CELH— AI Stock Forecast & Price Targets

Published 6/29/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live CELH price forecast →

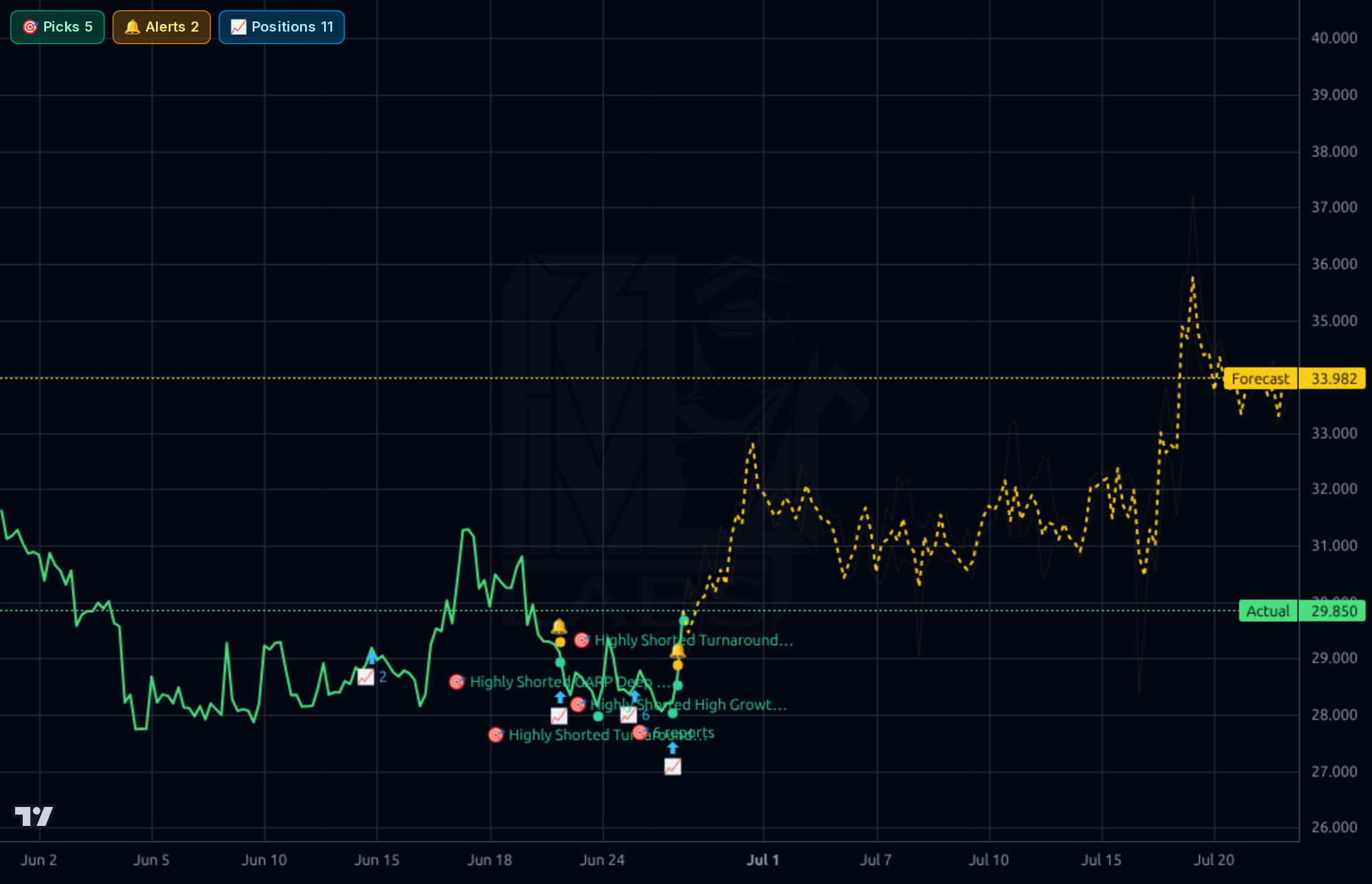

Celsius Holdings sits at $29.85, near 52-week lows (-55% from $66.74 high) after a brutal -34% YTD drawdown, but Q1 2026 results show a sharp reacceleration with revenue at $782M (+137% Y/Y, aided by Alani Nu) and net income rebounding to $110M. The setup is a classic high-short-interest (20.7% float), beaten-down growth name with forward P/E of ~14.9x and PEG 0.78 — attractive if execution holds, but the recent +3.4pp jump in short float and analyst PT cuts (Roth to $57, BofA to $45) confirm sentiment remains heavy.

1-4 week: Tactical long bias into the $27.50-29 zone with stops below $27.47 (52w low invalidation). Targets: $32 (50DMA reclaim), then $35-38 if short squeeze ignites given 20.7% short float and 4.24 days-to-cover. Size at 1/3 normal position given the broken weekly trend. Invalidation: daily close below $27 voids the base.

1-6 month: Accumulate into weakness ahead of May 7 (next earnings already passed — assume next print August). Thesis is that Alani Nu integration drives the implied earnings ramp to fwd EPS $2.02, justifying a re-rating from $30 toward analyst consensus $45-60. Base case return +25-40%. Catalysts: Q2 earnings, summer beverage seasonality, potential short squeeze. Change my mind if gross margin compresses further below 47%, or if Alani Nu synergies disappoint, or if Monster/Red Bull gain share materially.

1-3 year: CELH remains a credible long-term share-gainer in the functional energy category with Alani Nu adding a female-skewed brand and Rockstar partnership rounding out the portfolio. If management can defend ~50% gross margins and grow revenue 15-20% off the new $3B base, EPS can compound toward $4-5 by 2028, supporting $60-80 fair value. Biggest structural risk: energy drink category maturation in the US, private-label pressure, and the brand's reliance on Gen Z/fitness consumer trends which can rotate quickly. Secondary risk: PepsiCo distribution relationship terms.

Revenue trajectory is the strongest line of the bull case: Q1'26 revenue of $782.6M vs $739M in Q2'25 and $721M in Q4'25, with Sales Y/Y TTM of +123% and Sales Q/Q of +138%, largely reflecting the Alani Nu acquisition consolidating into the business. Gross margin has compressed to 48.3% in Q1'26 from 51.5% in Q2'25, a meaningful 300bp deterioration likely from acquisition mix and promotional intensity. Operating margin held at 18.3% and EBITDA rebounded to $158M after a noisy Q3'25 (-$61M EBITDA, likely one-time charges). Balance sheet is solid: $549M cash, $669M debt, working capital $813M, current ratio 1.77 — net debt is minimal relative to $679M TTM EBITDA. Cash flow is lumpy (Q4'25 burned $130M FCF, Q3'25 generated $321M, Q1'26 $66M), partly working-capital driven. ROE at 8-13% is mediocre for a CPG growth story, and trailing P/E of 71x looks stretched while forward P/E of 14.9x is reasonable IF the implied earnings ramp materializes. EPS Q/Q +126% is the standout quality datapoint.

Multi-timeframe picture is mixed-to-cautious. The weekly chart shows CELH has crashed from ~$95 highs in early 2024 to $29.85 — a structural ~70% drawdown that has flattened into a base. The daily chart confirms price is hugging the $27-30 zone after a multi-month downtrend, with $27.47 the 52-week low acting as the line in the sand. The 1h shows a constructive bounce: price broke from ~$28 base on June 23-24 to $29.85, reclaiming short-term momentum (RSI 50.2, SMA20 +1.79%) but still -3.45% below SMA50 and -32% below SMA200 — no confirmed trend change. Kronos forecast on 1h/4h is bullish ($33.98 1h target, $51.47 4h target longer-out), but the 1wk model has been BEATEN by naive baseline (17% vs 83%) — discount the longer forecasts heavily. The 1d forecast band sits around $38-40, plausible if the base holds. Key levels: support $27.47 (52w low), $28 (recent base); resistance $32 (50DMA), then $38-43 gap-fill zone.

Newsflow is mixed but tilts incrementally constructive after a long bearish stretch. Roth Capital and BofA both maintained Buy ratings but cut targets ($65→$57 and $55→$45 respectively), reflecting reset expectations rather than thesis breakage — and even the lower targets imply 50%+ upside from $29.85. Cramer's commentary explicitly highlighted that shorts have 'played havoc' with the stock, aligning with the L1 bearish signal that short float jumped from 17.3% to 20.7% (+3.4pp) in 45 days — heavy crowding sets up squeeze potential on any positive catalyst. Zacks coverage notes increased retail interest. The broader market news (crypto/MiCA) is irrelevant context. Net signal: institutional analysts remain constructive on direction while resetting magnitude, and short interest is at extreme levels — a classic setup for asymmetric upside if Q2 earnings surprise positively.

- Alani Nu integration driving the +138% Q/Q revenue surge — execution on cross-selling and shared distribution is the single biggest near-term lever

- International expansion into Europe and APAC per company description — currently still nascent revenue contribution

- CELSIUS Hydration line and powder/stick formats opening adjacent occasion categories beyond ready-to-drink

- Rockstar brand under management broadens shelf presence and bargaining power with retailers

- Forward EPS estimate of $2.02 implies ~5x growth from TTM $0.42 — if hit, fwd P/E of 14.9x re-rates materially

- Gross margin compression from 51.5% (Q2'25) to 48.3% (Q1'26) — 300bp slip signals promotional pressure or unfavorable mix from Alani Nu

- Short float at 20.7% (+3.4pp in 45 days) reflects strong institutional skepticism; squeeze cuts both ways if earnings miss

- Trailing P/E of 71x and price still -55% from highs — multiple compression risk if growth narrative breaks

- Forecast model directional accuracy of only 17% at 1wk horizon (worse than naive 83%) — model is unreliable in this regime

- Lumpy cash flow (Q4'25 -$130M FCF) raises working capital management questions

- Category competitive intensity: Monster, Red Bull, and emerging private-label functional drinks pressuring shelf economics

- Both Roth and BofA cut price targets in late June — analyst momentum is downward despite Buy ratings

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord