CTSH— AI Stock Forecast & Price Targets

Published 7/1/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live CTSH price forecast →

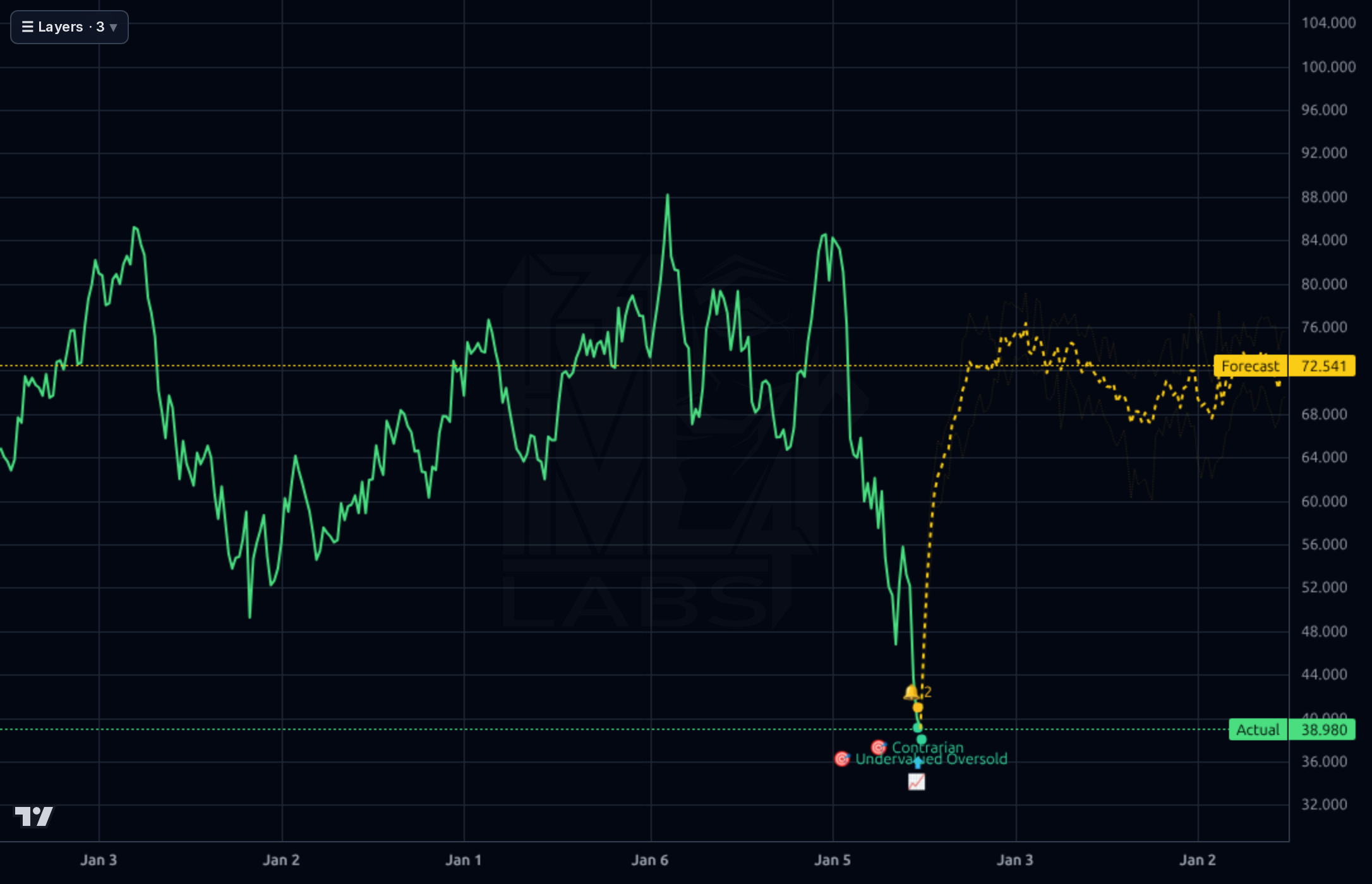

CTSH trades at a distressed 8.4x TTM P/E and 6.3x forward P/E after a ~55% drawdown from the 52-week high of $87 to ~$38.74, despite still generating ~$1.9B FCF, 15.6% operating margins, and mid-single-digit revenue growth. The setup is a classic deep-value/oversold contrarian opportunity into a July 29 earnings binary — attractive risk/reward on valuation and 3.3% dividend, but the Kronos model's directional accuracy is worse than a naive baseline here (3% vs 97% on 1d), so we treat the yellow forecast as unreliable and lean on fundamentals + mean-reversion technicals.

1–4 week view: Tactical long into oversold conditions (RSI 23, at 52W low, high short interest) with a small starter position only, because the July 29 earnings print is a binary catalyst inside the window. Entry zone $37.50–39.00, stop below $36.50 (loss of 52W low invalidates the base). First target $42–44 (gap fill / breakdown retest), stretch $47 (TD Cowen PT) if guidance holds. Explicit earnings stance: do NOT add size into the print — take partials before July 29 or hedge with puts; a bad Q2/soft guide could easily send it to $32–34. Treat Kronos 1H/4H forecasts as directionally supportive but numerically unreliable given 3% directional accuracy.

1–6 month view: Accumulate on weakness. Thesis: valuation (8.4x P/E, 6.3x fwd, 4.6x EV/EBITDA, 0.86x P/S) prices in an earnings recession that fundamentals don't yet show; a stabilized macro tape + any positive AI-services booking commentary should drive multiple re-rating toward 10–11x fwd EPS (~$62–68, in line with $67.70 consensus PT). Catalysts: July 29 print, ongoing Neuro AI / ServiceNow / Rubrik traction, potential buyback acceleration at these levels, dividend support at 3.4%. Expected return range +25% to +55% over 6 months. What would change my mind: two consecutive quarters of organic revenue deceleration below +3%, operating margin dropping below 14%, or major client (top-10) loss disclosures.

1–3 year view: CTSH is a cash cow IT services franchise attempting to pivot from labor-arbitrage to AI-orchestration (Neuro AI platform, multi-agent accelerators). If management executes, sustainable mid-to-high single-digit revenue growth + margin stability + steady buybacks/dividends supports a fair-value range of $70–90 (roughly reclaiming the 52W high). Structural risk: generative AI is a double-edged sword for IT services — it can either expand billable AI transformation projects or compress traditional application maintenance/BPO revenue as clients automate. Watch billable headcount vs. revenue-per-employee trend as the key long-term KPI.

Cognizant is a large, cash-generative IT services franchise: TTM revenue ~$21.4B growing +6.5% Y/Y (Sales Q/Q +5.8%), operating margin 15.6%, net margin 10.4%, ROE 14.9%, ROIC 13.9%. The most recent quarter (Q1 2026) showed revenue of $5.41B (+3% Y/Y), gross margin 32.8%, operating income $843M, and net income $662M — steady, not decelerating. Balance sheet is fortress-like for the sector: $1.5B cash vs only $1.09B total debt, Debt/Eq 0.07, current ratio 2.23, $15.1B stockholders' equity. Cash flow quality is strong — TTM FCF ~$1.9B on ~$2.76B operating cash, capex just ~$70M/qtr; P/FCF only 7.4x. Capital allocation supports a 3.3–3.4% dividend (27% payout, 5Y div growth 7%), leaving ample room for buybacks. The 'broken' element is optics: EPS Y/Y TTM -3.1%, and one anomaly quarter (Q3 2025 net income only $274M vs $645–662M in surrounding quarters) suggests a one-time charge weighing on TTM EPS. At 0.86x P/S, 4.6x EV/EBITDA and PEG 0.67, this is priced like a structurally impaired business, which the underlying financials do not corroborate.

Across all three timeframes the trend is unambiguously down: on the 1D chart price collapsed from ~$87 in Feb to a fresh 52W low ~$37.08, printing a near-vertical capitulation leg in June (SMA20 -18.6%, SMA50 -23.7%, SMA200 -41.8%; Perf Month -30.5%, Perf Quarter -36.6%, Perf YTD -53.3%). RSI(14) at 23.2 is deeply oversold and the 1H chart shows the first sign of stabilization/basing near $38–40 with 'Contrarian' and 'Undervalued Oversold' tags firing. The Kronos forecast band is aggressively bullish on all timeframes (1H target ~56, 4H ~77, 1D ~64, 1W ~72) — but the model's realized 1D directional accuracy is 3% vs a 97% naive baseline (MAPE 52%), so these targets should be heavily discounted; they mainly confirm the mean-reversion setup, not the magnitude. Key levels: support $37.08 (52W low) and psychological $37; first resistance at the $42–44 breakdown shelf, then $47 (TD Cowen PT) / $50 gap zone, then the $56 area (June breakdown). Short float 12.7% with 6.3 days-to-cover creates fuel for a squeeze on any positive catalyst.

Signal: the fundamental story is not deteriorating — CTSH is aggressively pushing its Neuro AI multi-agent platform, integrating ServiceNow AI Agents (June 18), expanding an AI governance alliance with Rubrik, and partnering with Pearson on AI workforce skills. Barchart and Yahoo both frame CTSH as an under-owned AI-services play trading at a discount, and a Yahoo piece highlights resilience in top-client bookings. Noise / overhang: Morgan Stanley and TD Cowen both cut price targets in late June (TD Cowen to $47, Hold), reflecting macro caution on IT services demand and a soft near-term outlook — this is the proximate cause of the June capitulation, not a company-specific blow-up. Consensus target remains $67.70 (Recom 2.06 = Buy-ish), well above spot. Broader market news (crypto/MiCA) is irrelevant to CTSH.

- Neuro AI Multi-Agent Accelerator becoming an orchestration layer across ServiceNow AI Agents (announced June 18) — potential to monetize as a horizontal enterprise AI control plane

- Expanded AI governance alliance with Rubrik targeting regulated enterprise AI deployments

- Pearson partnership on AI workforce skilling — pipeline for large-scale transformation engagements

- Strategic partnership with Uniphore Technologies on small language models + AI agents

- Continued dividend growth (5Y CAGR 7.1%, payout only 27%) and buyback capacity from $1.9B annual FCF at a 7.4x P/FCF valuation

- Bookings resilience in top-tier client cohort (per recent Yahoo coverage) provides revenue visibility

- Binary July 29 earnings print — a soft Q2 or weak H2 guide could break the $37 52W low toward $32–34

- Two sell-side downgrades in the last week (Morgan Stanley, TD Cowen to $47 Hold) signal continued Street de-risking

- IT services demand cyclicality — macro slowdown compresses discretionary tech consulting spend

- Secular risk that generative AI compresses traditional application maintenance / BPO revenue faster than Neuro AI monetization ramps

- Kronos model directional accuracy of 3% vs 97% naive baseline (1D) — the bullish forecast is statistically unreliable in this regime

- 12.7% short float with 6.3 days-to-cover cuts both ways — can amplify downside on any negative catalyst

- Insider trade: Congressional disclosure shows a sell in March; insider ownership just 0.49%

- EPS Y/Y TTM -3.1% and an anomalous Q3 2025 (net income only $274M) suggest lingering charges or margin volatility

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord