FOUR— AI Stock Forecast & Price Targets

Published 7/1/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live FOUR price forecast →

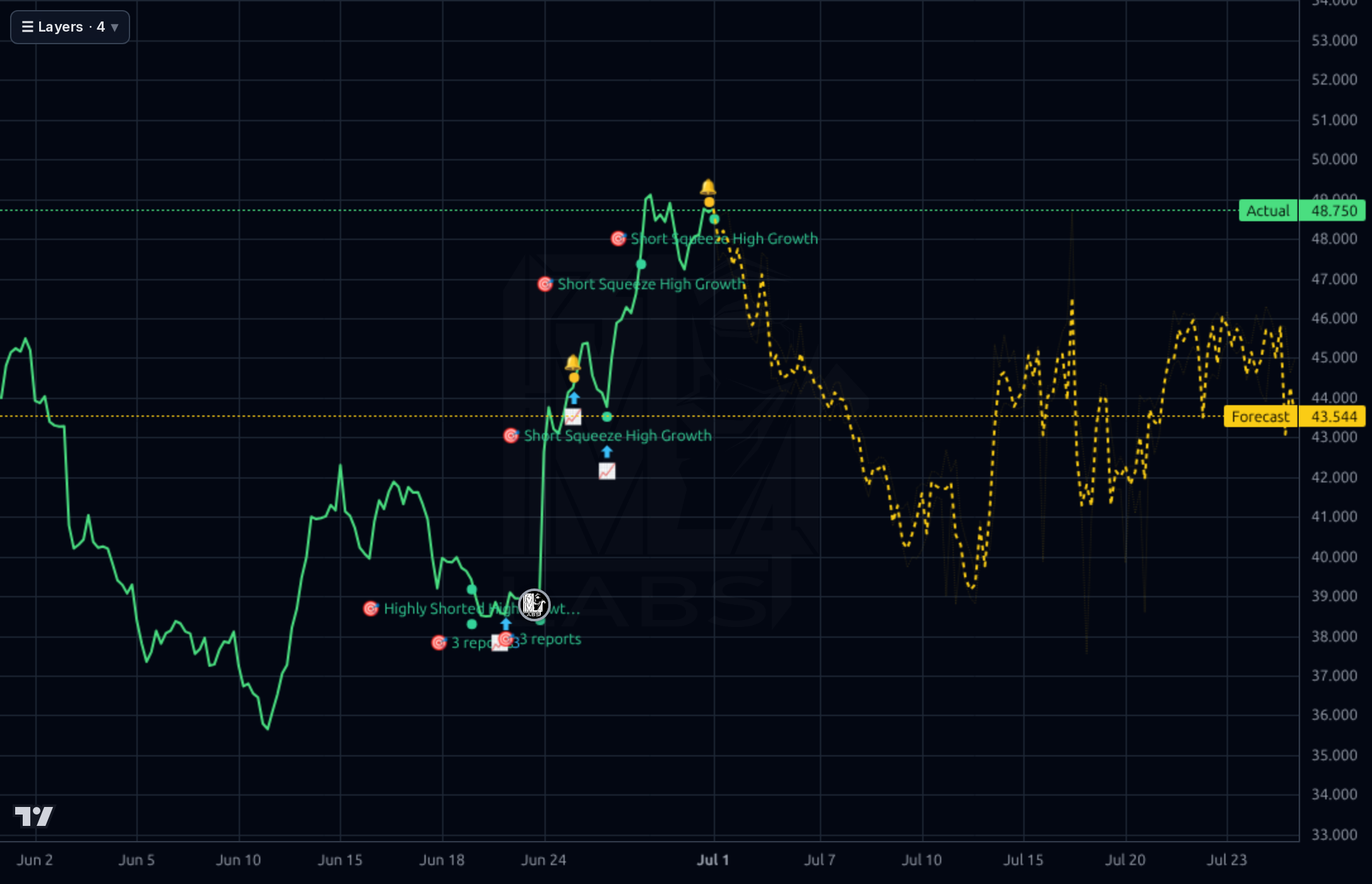

Shift4 has rallied ~25% off the mid-$30s low to $48.23 on short-squeeze dynamics (29.9% short float), a proactive debt refinancing, and renewed sell-side attention, but the stock is now bumping into resistance at prior breakdown levels with RSI at 65.5 and SMA20 stretched +18%. The setup remains fundamentally interesting — 28% revenue growth, 7.2x forward P/E, PEG 0.48, $488M FCF — but leverage (Debt/Eq 2.77, $4.58B debt) and a binary Aug 4 earnings print argue for trimming into strength rather than chasing.

Into a 34-day runway to the Aug 4 earnings print, I would TRIM/take partial profits on the squeeze at $48-49 rather than add. Key resistance is $49-52 (prior breakdown shelf and forecast upper band); key support is $43-44 (Kronos forecast anchor and yellow dashed line) and then $38-40 (breakout base). Invalidation of the bounce is a daily close back below $43.50. Do NOT carry a full swing position into earnings — IV crush and a binary EPS reaction (consensus Q2 EPS $1.24; miss risk elevated given Q1'26 margin compression) make it a coin flip. If you must be long into the print, size it as a lottery ticket, not core.

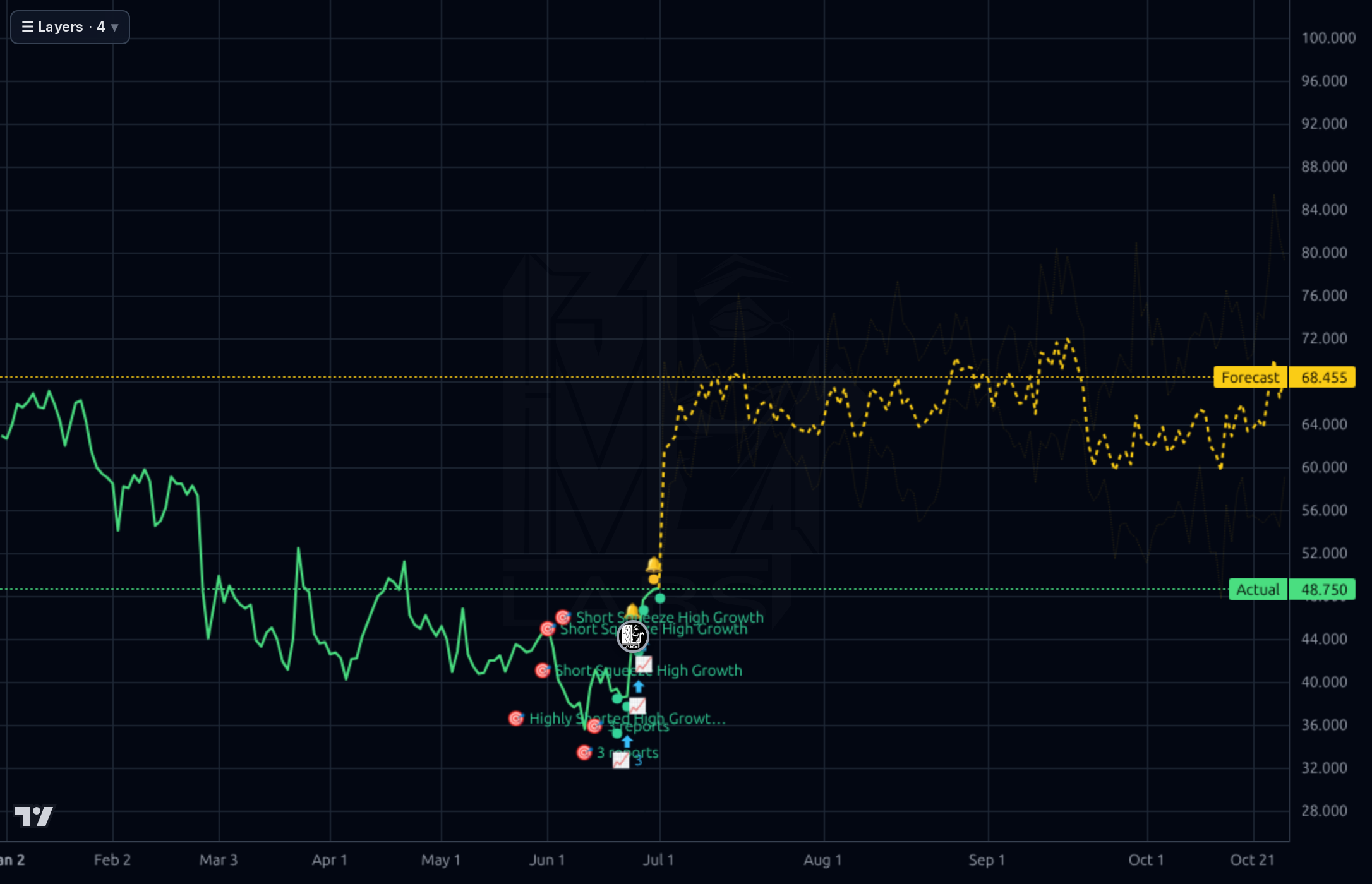

Over 1-6 months the setup is a range trade $40-58 with earnings as the fulcrum. Base case: earnings show volume growth intact but margins still pressured, stock oscillates in a $42-55 band, offering ~10-15% swing returns. Bull case (World Cup volumes surprise, margin bottom confirmed, guidance raised): re-rating toward $58-65 on multiple expansion from 7x to 9-10x forward. Bear case (margin compression accelerates, debt costs pressure EPS): retest $36-38. What would change my mind: a Q2 print showing gross margin back above 36% and operating margin above 8% would flip me to a full ACCUMULATE with a $60+ base target.

The 1-3 year terminal thesis rests on whether Shift4 can defend its integrated software+payments moat in hospitality, sports/stadiums, and international expansion against Stripe, Adyen, Toast, and Block. If revenue compounds 20%+ and margins normalize to mid-teens operating, this is a $75-100 stock at a 12-14x forward multiple. The structural risk is that payments is commoditizing and vertical SaaS players (Toast in restaurants specifically) are eating share, in which case the $4.58B debt stack becomes existential in a downturn. Insider ownership of 29.6% (founder Isaacman still the biggest holder per news) aligns incentives, and the SkyTab/international/crypto donation optionality is real but unquantified.

Top line remains strong: TTM revenue $4.45B with Sales Y/Y TTM +28.3% and Q1'26 revenue of $1.121B up meaningfully year-over-year, but sequential deceleration is visible — Q1'26 revenue slipped from Q4'25's $1.189B and gross margin compressed to 34.97% from 37.82% in Q4'25. Operating margin collapsed to 4.46% in Q1'26 from 10.2% in Q4'25 and net income fell to $15M from $40.2M, driving the -106.8% EPS Q/Q and -72.4% EPS Y/Y TTM prints — a real profitability problem, not just optics. The balance sheet is the biggest concern: $4.58B total debt against $1.65B equity (D/E 2.77), and cash burned from $3.03B in Q2'25 to $473M by Q1'26 as the company deployed capital (likely M&A/buybacks). FCF is still robust at $488M TTM and P/FCF of 7.3x is genuinely cheap, but Q1'26 FCF of just $63M vs $148M in Q4'25 shows the same compression. Forward P/E of 7.2x and PEG of 0.48 discount a lot of bad news; the question is whether margin compression is transitory (integration/mix) or structural (competition from Stripe/Adyen/PayPal). Insider ownership of 29.6% and institutional ownership of 91.2% are supportive of an eventual re-rating if execution stabilizes.

Across the 1h and 4h charts, the June rally from $35.64 to $49 is textbook short-squeeze price action — near-vertical, low-volume-hesitation, and now stalling right at the forecast band's upper edge around $48-49. The 1d chart shows price has reclaimed the May-June basing zone but is still -55% off the 52-week high of $108.50 and -16.5% below the 200-day SMA, so this is a counter-trend bounce inside a broader downtrend, not a confirmed reversal. RSI at 65.5 is approaching overbought and SMA20 is +18.3% below price — extended. The weekly view frames $48-52 as the key pivot: the prior support shelf from late 2024 that broke down; reclaiming it opens $58-65, failure sends the stock back to the $38-40 base. Kronos forecasts diverge meaningfully — the 1h/4h models see near-term mean reversion toward $43.5, while the 1d/1wk models project drift to $68-72 over months; given directional accuracy trails the naive baseline on both near-term horizons, I discount the AI signal and lean on the technical read: resistance overhead, momentum stretched.

The material catalyst was the June 24 announcement of proactive debt management — critical given the $4.58B debt load — which drove the 11.8% pop and set the squeeze in motion. Loop Capital initiated coverage June 25-26 at Hold with a $40 target (below current price), a mixed signal: sell-side attention is returning but the price target is a de facto downgrade from spot. Zacks flagged the June 29 8.8% surge but cautioned that earnings estimate revisions don't support continuation. The bull narrative also includes World Cup-related payment volume tailwinds and a Seeking Alpha reiteration citing Q1 volume/international growth. Signal: debt refi de-risks the balance sheet and squeeze dynamics are real. Noise: retail chatter on Stocktwits/X and Moonshot listing campaigns — ignore. The $40 Loop target and Zacks caution are the sober counterweights to the crowd's 100% bullish sentiment reading, which itself is a contrarian yellow flag.

- World Cup 2026 payment processing volumes flagged by retail commentary and consistent with Shift4's stadium/venue vertical — potential Q2/Q3 revenue catalyst

- International expansion contributing to the 28% TTM revenue growth per Seeking Alpha coverage citing Q1 international strength

- Proactive debt refinancing announced June 24 reducing interest burden on the $4.58B debt stack — direct EPS accretion if executed

- SkyTab POS and integrated software suite (Lighthouse, Shift4Shop) driving cross-sell into existing merchant base per company description

- The Giving Block crypto donation marketplace as embedded optionality in a rising crypto adoption cycle

- Q1'26 gross margin compressed to 34.97% from 37.82% and operating margin fell to 4.46% from 10.2% — if this continues, the 7.2x forward P/E is a value trap

- Total debt of $4.58B against $1.65B equity (D/E 2.77) with cash down from $3.03B to $473M in three quarters — leverage is elevated in a rising-rate scenario

- Short float rose from 26.6% to 29.9% (+3.3pp in 45d) — sophisticated shorts are pressing the bet even after the squeeze

- Aug 4 earnings is a binary event 34 days out; consensus $1.24 EPS with EPS Y/Y TTM already -72.4% creates asymmetric miss risk

- Stock is -55% off the 52-week high and -50.9% YoY — the broader trend is still down; this bounce is counter-trend until proven otherwise

- Competitive pressure from Stripe, Adyen, Toast, and Block in Shift4's core verticals — the AI-disruption narrative that crushed the stock has not been refuted

- Loop Capital's $40 target initiated at Hold is below current $48.23 — sell-side is not endorsing this rally

- Retail sentiment is 100% bullish on tagged messages — classic contrarian warning at a resistance level

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord