INTR— AI Stock Forecast & Price Targets

Published 7/6/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live INTR price forecast →

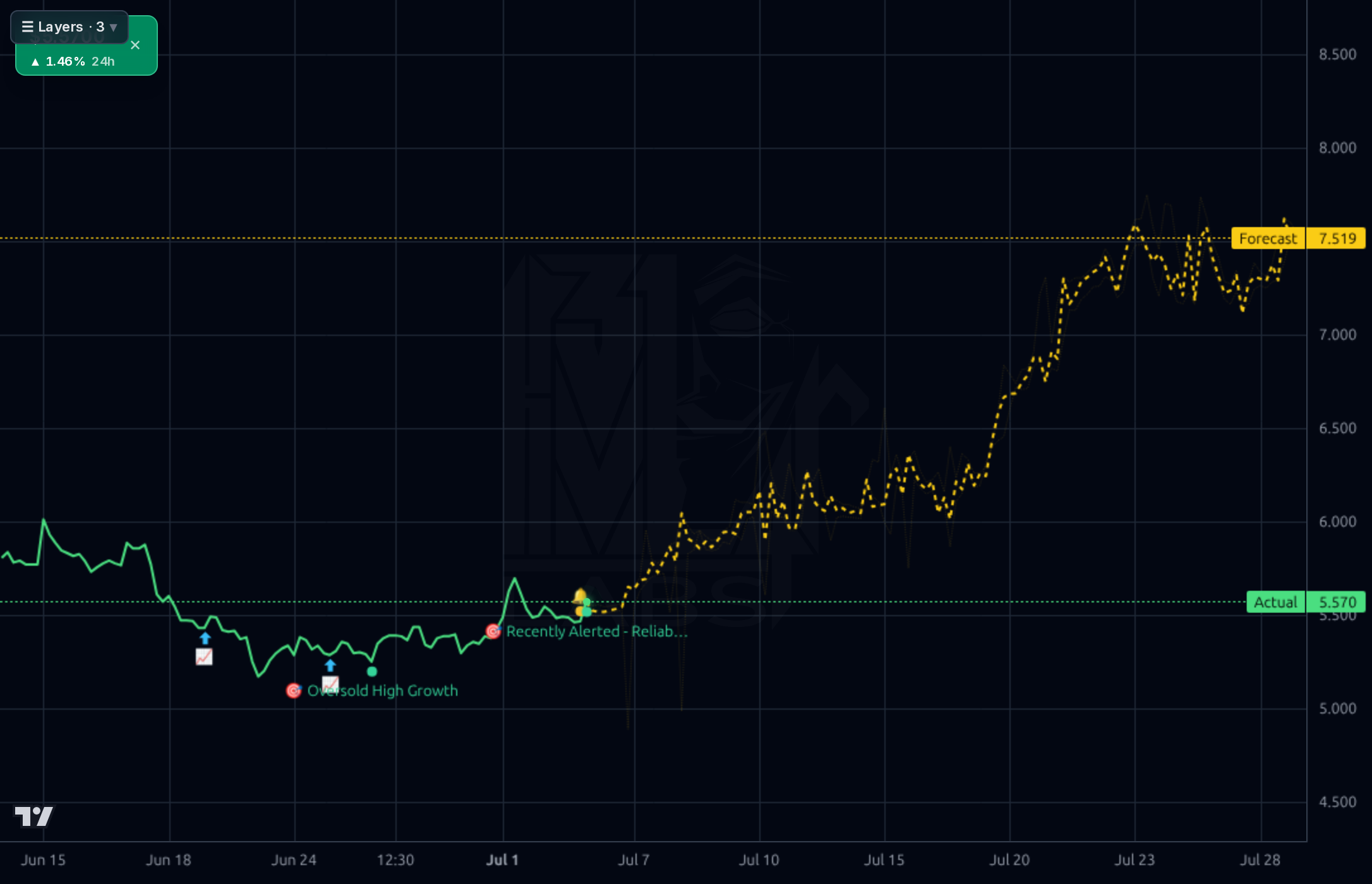

Inter & Co is a profitable Brazilian digital bank trading at 9x trailing / 5.2x forward earnings with 50% YoY revenue growth and 15% ROE, but the stock has been in a brutal downtrend (-35% YTD, -32% below 200-day SMA). The Kronos 1d model is constructively bullish near-term with a $7.40-7.52 forecast versus $5.57 spot, and analyst target of $9.90 implies ~80% upside, but the weekly forecast is unreliable and the Aug 7 earnings print is the binding catalyst. This is an ACCUMULATE candidate for value/growth investors willing to size around the print.

1-4 week view: Initiate a starter position (~1/3 target size) in the $5.30-5.60 zone with a hard stop below $5.10 (invalidates the 52w low base). Kronos 1d model has 66% directional accuracy and forecasts $7.40, giving a favorable ~3:1 R/R to first target $6.50 and stretch $7.20. CRITICAL: Aug 7 earnings is ~32 days out and is the key binary catalyst — do NOT hold full size through the print given the recent 51% EPS Q/Q sets a high bar. Plan is pre-earnings only; scale out 50%+ into any $6.50-7.20 spike before Aug 7, then reassess.

1-6 month view: Thesis is that Q2'26 earnings (Aug 7) confirms the profitable-growth narrative (Rule of 50, US expansion traction) and revalues the multiple back toward analyst consensus $9.90 (~80% upside). Expected return range: base case $7.50-8.50 by year-end (+35-55%), bull case $9.90 if EPS beats and Brazil rates cut cycle accelerates. Catalysts: Aug 7 earnings, Brazilian Selic rate decisions, US rollout milestones. Change my mind: an EPS miss/margin compression on Aug 7, or a break below $5.00 that voids the base.

1-3 year view: Terminal thesis is that Inter compounds book value at 15%+ ROE while scaling from 30M+ Brazilian clients into US Latino/remittance corridors, warranting a re-rating from 1.2x book to 2.0x+ book as digital-bank peers (Nu, etc.) trade materially higher. If forward EPS growth of 24% CAGR holds, EPS could reach $2.00+ by 2028, supporting a $16-20 stock at 8-10x. Biggest structural risk: Brazilian macro/FX (BRL depreciation directly hits USD ADR value), and competitive pressure from Nubank in the same digital-banking pool.

Fundamentals are the strongest leg of the thesis. Quarterly revenue has climbed steadily from BRL 2.00B (Q2'25) to BRL 2.44B (Q1'26), a ~22% sequential expansion over four quarters, while net income rose from BRL 315M to BRL 395M — net margins holding a tight 15.5-16.2% range. TTM sales growth is 50% and EPS Q/Q is +51%, with ROE at 14.9% and ROA at 1.6%, respectable for a digital bank. Valuation is undemanding: trailing P/E 8.8, forward P/E 5.2, P/B 1.24, PEG 0.23, P/FCF 3.85 — all screening as deep value against consensus 24% five-year EPS growth. Balance sheet shows total assets of BRL 99B against equity of BRL 10.2B (leverage ~10x, normal for a bank), and Q1'26 operating cash flow swung positive to BRL 1.45B after a negative Q4'25. The main knock: debt/equity of 3.1 and current ratio of 0.51 look tight in isolation but are typical of a regulated bank funded by deposits. Capital allocation is disciplined per management commentary ('Rule of 50'), with a modest 2.07% dividend and no evidence of dilutive activity in the share count (325.8M outstanding).

Price action is decisively bearish across all timeframes. On the 1d and 4h charts, INTR broke down from ~$10 in Feb to a 52-week low of $5.16 in late June, with SMA200 -32.6% and SMA50 -12.6% — a textbook downtrend. The 1wk chart shows the entire 2024-2025 rally from ~$2 to $9.40 has retraced back to the $5.50 area, sitting just above prior consolidation support at $4-5. However, RSI at 40 is not yet oversold on daily but the 1h chart shows a clean base forming late June with 'Oversold High Growth' and 'Recently Alerted - Reliable' signals firing near $5.20-5.30, followed by a bounce to $5.57. Kronos 1d forecasts a rally to ~$7.40 (33% upside) with the 4h band supporting $6.50-8.00 into August before rolling over — consistent with a mean-reversion bounce rather than a new uptrend. The weekly forecast is essentially flat at $5.76 and has been beaten by naive baseline, so discount it. Key levels: support $5.16 (52w low, must hold), resistance $6.00 (psychological/prior consolidation), then $7.00-7.50 (forecast target + declining 50-day area).

Signal: The July 2 Investing.com interview with CFO Santiago Stel articulates a coherent 'Rule of 50' framework (profitable growth over growth-at-all-costs) and flags US expansion as the next chapter — meaningful because it aligns with the strong Q1'26 print and validates the fundamental turn. The July 3 Insider Monkey/Emerging Value bullish thesis at $5.38 is a corroborating third-party view but is a curated aggregation, not primary research — treat as sentiment confirmation. Noise: Broader-market crypto/geopolitical headlines (Bitcoin, Iran) are not relevant to INTR beyond generic EM risk-off tone. Retail social sentiment is 100% bullish on a tiny sample (n=4 tagged) — consistent with a bombed-out stock finding contrarian believers, but too small to weight heavily.

- US expansion — CFO Stel explicitly named the US as 'the next chapter' in the July 2 Investing.com interview, targeting Latino/remittance customers

- Q1'26 revenue growth of 50% YoY with expanding net margin (15.7% → 16.2%) demonstrates operating leverage from the scaled banking-as-a-service platform

- Rule of 50 discipline (efficiency + growth ≥ 50) is the internal KPI framework driving capital allocation — validated by 15% ROE at only 4 years post-IPO

- Fee-income diversification: brokerage, insurance, pension and Inter Shop marketplace add non-interest revenue less sensitive to Selic rate cycle

- EPS next Y consensus growth of 27% and next 5Y of 24% CAGR (per Finviz) with PEG 0.23 suggests the growth is materially underpriced

- Aug 7 earnings binary — the stock has already priced in a strong print via the CFO interview; any miss on net margin or credit costs likely re-tests $5.00

- Brazil macro/FX risk — BRL depreciation directly hurts USD-denominated INTR ADRs; INTR is down 35.5% YTD despite improving fundamentals, suggesting FX/EM risk-off is dominant

- Weekly Kronos forecast has 0% directional accuracy vs 100% naive baseline — the model is unreliable on longer horizons for this name, so don't over-rely on multi-month AI projections

- Competitive: Nubank (NU) is the dominant Brazilian digital bank and any market-share loss narrative would compress INTR's multiple

- Leverage: Debt/Equity 3.1 and Current Ratio 0.51 leave little cushion if Brazilian credit cycle deteriorates or NPLs rise

- Short interest 5.21% and short ratio 2.14 indicate meaningful skeptic positioning — a squeeze is possible but so is continued distribution

- Q4'25 operating cash flow was negative BRL 145M — Q1'26 rebound to +BRL 1.45B is encouraging but the volatility warrants monitoring

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord