KRMN— AI Stock Forecast & Price Targets

Published 7/6/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live KRMN price forecast →

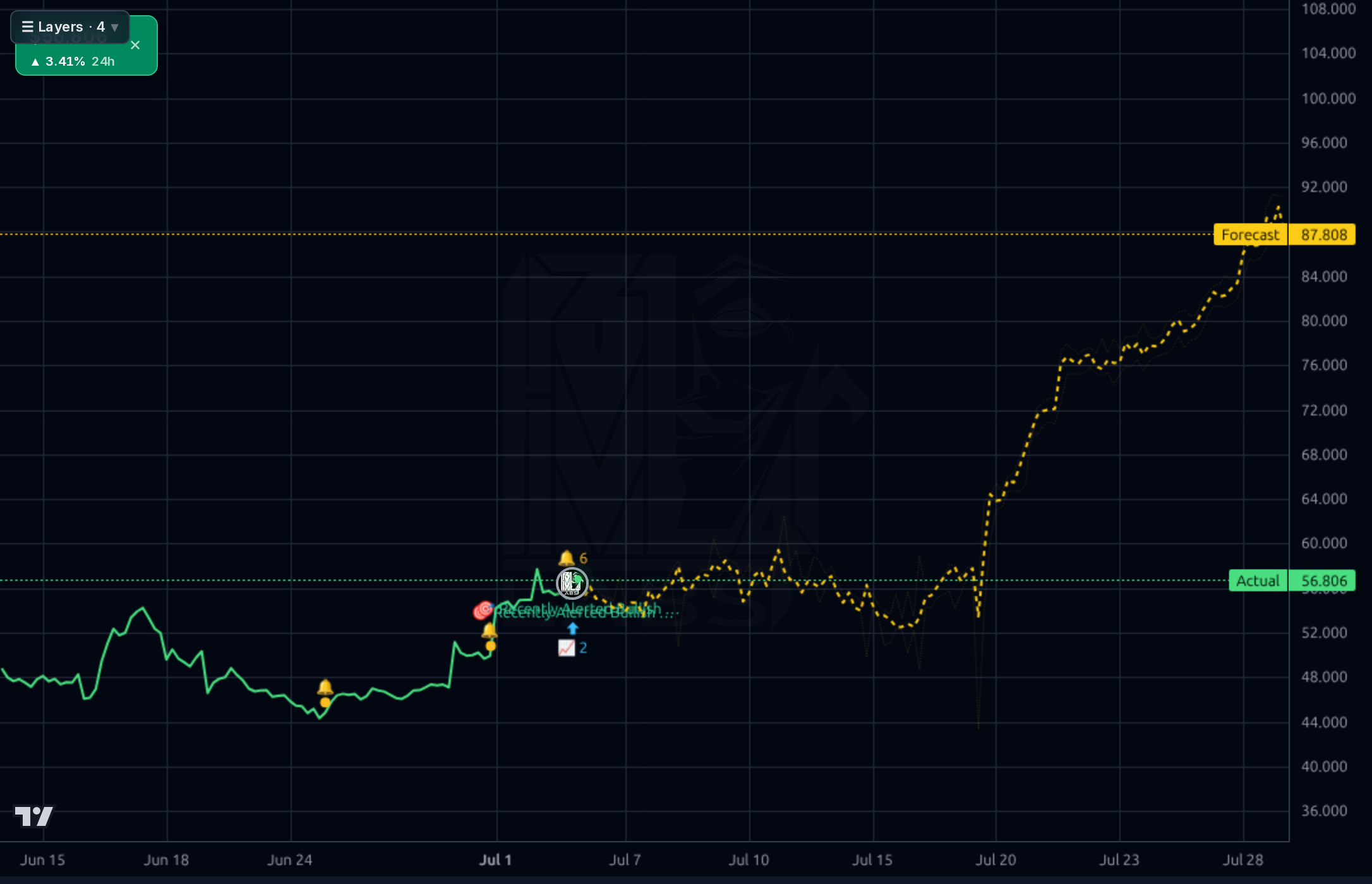

Karman is a hyper-growth defense/space supplier (TTM sales +44%, Q/Q +51%, pipeline ~$3B) trading at demanding multiples (61x fwd P/E, 14x sales) after a ~52% drawdown from $118 and an $854M secondary at $61. Near-term technicals have improved with a strong reclaim off $44-46 lows and the model bullish on 1-4 day horizons, but the Aug 6 earnings print and lingering sponsor overhang cap conviction. Accumulate selectively below $58, respecting $61 as the key resistance and $44-46 as thesis invalidation.

1-4 week view: constructive but constrained by the Aug 6 earnings print (~31 days away). Prefer to accumulate on pullbacks into $54-56 with a partial starter (25-33% of intended size); do NOT size a swing into the print. Stop below $52 on a closing basis; invalidation for the reclaim thesis is $50. Trim/partial-cover on any push into $60-62 (secondary resistance) ahead of earnings, since the risk/reward into a binary event with -9.4% prior EPS surprise is unattractive at that level. Earnings stance: neutral-to-positive fundamentally, but do not carry a full position through it.

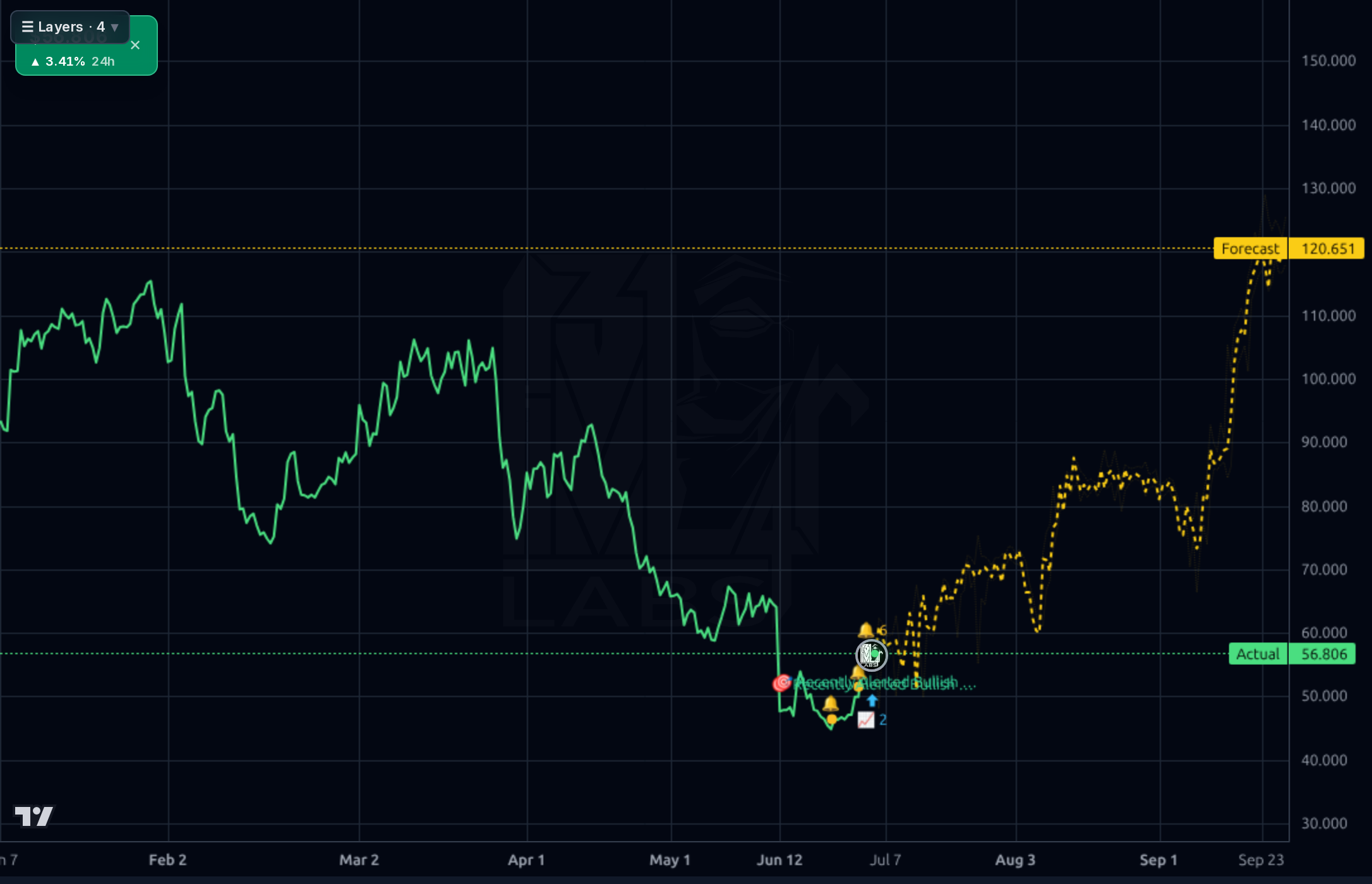

1-6 month view: base case is range-bound $55-72 as the market waits on backlog conversion and any further TCFIII sell-down. Bull case ($90+) requires a clean beat/raise on Aug 6, gross margins holding 40%+, meaningful pipeline-to-backlog conversion in the disclosures, and OCF turning positive. Bear case ($44) triggers on any revenue miss, margin compression, further debt-funded capex without cash conversion, or a fresh secondary filing. Expected return range at $56.80 entry: -22% to +58%, skewed positive on optionality but with real gap risk. What changes my mind: a follow-on filing before earnings (bearish), or backlog disclosure confirming >$1B of the pipeline has converted (bullish).

1-3 year view: Karman is a legitimate pure-play on hypersonics, strategic missile defense, and small-launch — end markets with multi-year secular tailwinds and consensus 5-yr EPS growth of ~51%. If management converts even a third of the $3B pipeline and holds 40% gross margins, revenue could double toward $1B+ and the multiple compresses naturally. The structural risk is capital structure: 2.14x debt/equity with negative FCF means any program-timing air pocket or rate cycle turn forces equity issuance at unfavorable prices, and sponsor TCFIII still has stock to distribute. Terminal thesis is positive but path-dependent — this is not a set-and-forget position; it needs to be re-underwritten each quarter against cash conversion and leverage.

Growth is genuinely exceptional: quarterly revenue climbed from $115M (Jun-25) to $151M (Mar-26), a +51% Y/Y ramp, with gross margin holding a stable 40-42% band and operating margin expanding into the 14-18% range. TTM sales are $522M with EBITDA of $136M, and management reports pipeline tripling from ~$1B to ~$3B between Mar-25 and May-26 — meaningful coverage against current revenue. However, the quality of the story is weaker than the top line suggests: TTM free cash flow is -$40M, Q1-26 OCF was just $209K, and total debt has ballooned from $486M (Jun-25) to $867M (Mar-26), driving debt/equity to 2.14x. ROE of 7.9% and ROIC of 2.4% are well below the company's cost of debt, meaning the balance sheet is being levered to fund working capital and capacity ahead of revenue conversion. Net margin of 5.7% and a trailing P/E of 249 leave essentially no cushion for execution slippage; the last EPS surprise was -9.4%. Valuation (14.3x sales, 54.6x EV/EBITDA, PEG 1.2) is priced for flawless delivery.

Across the 1h and 4h charts, price has staged a decisive reclaim from the June 2026 low near $44-46 to $56.80, printing a +21.8% week and clearing the 20-day SMA (+14.2%) while still sitting -3.5% below the 50-day and -26.7% below the 200-day — classic early trend-repair, not confirmed reversal. The 4h chart shows the forecast band tracking upward through $60-90 into September, but this name's realized directional accuracy collapses below the naive baseline beyond ~5 days (H6-H8 at 17-43%), so only the 1-4 day bullish read is credible; the multi-month $88-120 prints on the daily/weekly charts should be discounted heavily. Critical levels: $61 (secondary pricing) is durable overhead supply and the true trend-change test; $54-55 is near-term support; $44-46 is structural invalidation. RSI 55.9 leaves room, and the +21.8% weekly move plus 9.4% short float sets up squeeze potential, but the stock remains -52% off highs with the 200-day sloped down.

Signal: Citi maintained Buy but cut the target from $97 to $76 (Jul 1), a tempered but still-constructive analyst posture that aligns with the $103.50 street target average and 1.45 Recom score. The May 28-29 disclosures matter most — TCFIII priced an upsized secondary of 14M shares at $61 for ~$854M, and management simultaneously flagged the pipeline growth from ~$1B to ~$3B. Multiple mid-cap growth screens (Insider Monkey, Simply Wall St., Zacks) picked up the name in June, and a +7.1% single-session move on above-average volume shows retail rotation is active. The June 11 8-K (Items 4.01 auditor change, 9.01 exhibits) is a housekeeping item but worth noting as an auditor change in a young public company. Noise: broader crypto/bitcoin and Iran headlines are irrelevant to the thesis. The dominant framing across coverage is bullish on defense-tech secular demand, but that consensus is already reflected in the multiple. Net takeaway: pipeline growth is real and analysts remain constructive, but the sponsor overhang at $61 is the single biggest technical anchor.

- Pipeline expansion from ~$1B (Mar-25) to ~$3B (May-26) — ~6x current TTM revenue if converted to backlog

- Quarterly revenue ramp $115M → $151M (+31% in 3 quarters) with gross margin holding 40-42%

- Hypersonics and strategic missile-defense content (payload protection, interstage, propulsion) on priority Pentagon programs

- Consensus EPS growth ~60% next year, ~51% over 5 years drives PEG down to ~1.2 despite headline 61x fwd P/E

- Three-market diversification (defense, space, launch) reduces single-program dependence

- Analyst coverage constructive with 1.45 Recom score and $103.50 average target vs $56.37 spot

- Extreme valuation: 61x fwd P/E, 14.3x sales, 54.6x EV/EBITDA — any Aug 6 miss triggers violent de-rate

- Negative FCF (TTM -$40M) with debt up from $486M to $867M in three quarters; ROIC 2.4% below cost of debt

- Sponsor overhang: TCFIII already sold $854M at $61 in May; further secondaries likely cap rallies at that level

- Prior EPS surprise -9.4% — thin 5.7% net margin leaves no cushion for execution slippage

- 9.4% short float signals informed skeptics; also fuel for two-way volatility

- Auditor change (Jun 11 8-K Item 4.01) is a governance flag to monitor in a young public company

- Defense appropriations/program-timing concentration risk given hypersonics reliance

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord