KVYO— AI Stock Forecast & Price Targets

Published 7/1/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live KVYO price forecast →

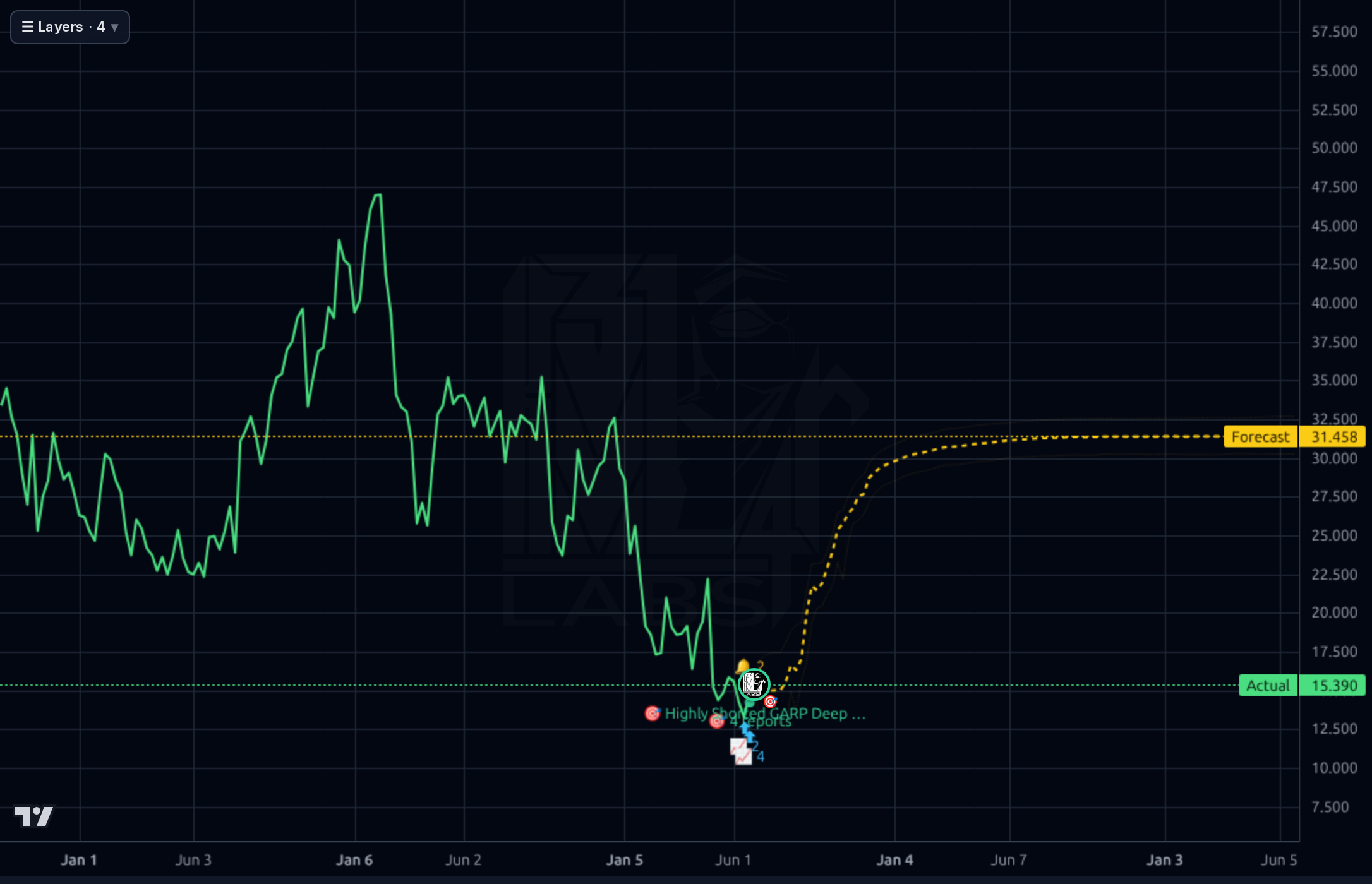

KVYO is a high-growth SaaS name (Q1 revenue +28% YoY, 75% gross margins) that has been decimated in 2026, down 53% YTD and 55% off 52-week highs, now trading at $15.10 with a forward P/E of ~14.6 — historically cheap for this asset. Fundamentals are inflecting positive (four straight quarters of narrowing losses to Q1 net income of $9M, FCF of $241M TTM), sentiment is washed out (18% short float, 44% institutional ownership), and the chart shows an early base-building attempt off the $12.53 low. The August 4 earnings print is the binary catalyst that dictates whether this becomes a genuine reversal or another leg down.

1-4 week view: Tactical long bias while $14.00 holds, targeting $16.50 first then $18.00. Size at half normal risk given the stock sits 34 days from earnings (August 4) — this is the dominant catalyst and I would NOT hold a full position through the print. Hard stop below $13.75 (invalidates the breakout and puts the $12.53 low in play). Earnings stance: trim or fully exit any swing trade 2-3 sessions before 8/4; the setup is 'ride the bounce, respect the binary.'

1-6 month view: Constructive. Thesis is that a Q2 beat + AI Agent monetization commentary re-rates the stock from ~14x forward earnings toward 20x, implying $20-22. Catalysts: 8/4 earnings, AI Agent enterprise wins, Shopify dependency narrative easing, further short-covering (18% still elevated). What changes my mind: revenue growth decelerating below 22% YoY, operating margin backsliding, or Shopify concentration disclosures worsening. Expected return range: -15% to +45% skewed positively given valuation reset already occurred.

1-3 year view: Klaviyo remains the leading B2C CRM/marketing platform in the SMB e-commerce stack with a durable 30%+ growth profile and structurally 75%+ gross margins. The AI-agent transition is the swing factor — if Klaviyo becomes the data/orchestration layer for merchant AI (as the Marketing/Customer Agent launches suggest), it earns a premium multiple and can compound to $35-45. Biggest structural risk is customer concentration/dependency on Shopify's ecosystem and the possibility that Shopify or a hyperscaler builds competing native AI marketing agents, commoditizing Klaviyo's workflow layer. Secondary risk: SMB e-commerce cyclicality in a weaker macro.

The fundamental picture is quietly improving beneath a brutal tape. Quarterly revenue has stepped from $293M (Q2'25) → $311M → $350M → $358M (Q1'26), a clean sequential ramp with Sales Y/Y TTM of 30.3% and Q1 YoY around 28%. More importantly, the P&L has flipped: operating income moved from -$31M in Q2'25 to +$1.7M in Q1'26, and net income from -$24M to +$9M — a real inflection, not accounting noise. Gross margin is stable at 74-76%, consistent with best-in-class B2C SaaS. The balance sheet is fortress-grade: $985M cash vs. $117M debt, current ratio 4.23, working capital $875M, and TTM FCF of $241M against a $4.5B market cap gives an EV/FCF near 15x — reasonable for a 30% grower. Forward P/E of 14.6 and PEG of 0.62 signal the market is pricing in significant deceleration or disruption; the burden of proof is now on Q2 numbers. The one blemish is Q1 operating cash flow of only $34M (vs. $93M in Q4'25), which needs monitoring for seasonality vs. deterioration.

Across timeframes the picture is 'basing after a crash, not yet trending.' The 1D chart shows a violent drawdown from ~$47 highs (visible on the weekly) to a $12.53 low, followed by a sharp reflex rally to $15.39 — the stock is +11.9% on the week and +20.5% off the low, but still -33.7% below the 200-SMA and -6.7% below the 50-SMA, so this is a bounce inside a downtrend, not a confirmed reversal. RSI at 52 is neutral, giving room in either direction. The 1h chart shows a clear breakout above the $14.90-15.00 shelf with the forecast band pointing to $18.05 (~+20%) — plausible near-term. The 4h and 1D forecasts extend to $24-28, but past forecasts on this name have systematically overshot, and the model's 1D directional accuracy (63%) is below the naive baseline (67%), so I discount those upside targets meaningfully. Key levels: support $14.00 (breakout retest) then $12.53 (52w low, hard invalidation); resistance $16.50 (June swing), then the $18-19 gap zone, with $20.50 as the 52w low-print reference from further back.

Signal: (1) Klaviyo launched paired AI agents (Marketing Agent + Customer Agent) on 6/30 with an NYSE segment — this directly addresses the bear case that AI disintermediates SaaS by positioning Klaviyo as the AI layer itself, not the victim. (2) Goldman Sachs flagged KVYO as a software name with 60%+ upside potential (6/28), and Zacks noted an 87% consensus target upside (6/5) with positive earnings estimate revisions. (3) The 6/26 fundamental signal shows short float dropping from 24.8% to 18.2% — a material 6.6pp de-risking as bears cover into the bounce. Noise: Piper Sandler's $30→$26 target cut on 5/7 is stale but reflects the broader 'SaaS de-rating' overhang. The Seeking Alpha piece on Shopify dependency is a legitimate structural concern but not new information. Stocktwits chatter about Composer public availability and Customer Agent traction is directionally supportive of a good Q2 print but should not be trusted as fact.

- August 4 earnings is a binary — a miss on revenue or forward guide against the elevated 27.9% Sales Q/Q reset likely retests $12.53

- Shopify ecosystem dependency remains the dominant structural overhang flagged by sell-side (Seeking Alpha 6/30)

- AI-agent disruption cuts both ways — if hyperscalers or Shopify build native competing agents, Klaviyo's workflow moat erodes

- Short float still 18.2% and Perf YTD -53.5% signals the stock remains a contested name; bounce could fade on any bad tape

- Q1 operating cash flow ($34M) collapsed from Q4 ($93M) — need clarity that this is seasonality, not deterioration

- Forward EPS estimates ($1.03) require sustained margin expansion; any operating margin backslide re-opens valuation compression

- The 1D forecast model has directional accuracy below the naive baseline in this regime, so upside forecasts should be discounted

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord