MORN— AI Stock Forecast & Price Targets

Published 7/6/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live MORN price forecast →

Morningstar has been violently re-rated (-47% from 52W high, -24% YTD) yet fundamentals remain intact: 30.7% ROE, 62% gross margins, $453M FCF, and accelerating operating margins (24.2% in Q1'26). The stock is showing early technical stabilization off the $141 low with a reclaim toward $165, but the July 29 earnings print is a binary catalyst and balance sheet leverage (D/E 1.87) plus a recent analyst downgrade warrant measured accumulation rather than aggressive buying.

1-4 week view: Hold or lightly accumulate on weakness toward $150–155; do NOT add aggressively into the July 29 print. That earnings release is a binary event with high IV crush risk. Key invalidation: a break below $150 on volume shifts risk/reward negatively toward the $141 low. Upside cap pre-earnings is $173 (major resistance). If already long, keep position size modest and let the print resolve direction.

1-6 month view: This is where the accumulation case is strongest. Assuming earnings do not reveal fundamental deterioration, the combination of a re-rated multiple (12.3x fwd), intact margin expansion, and PitchBook/Indexes/Copilot growth vectors sets up a mean-reversion trade toward $185–200 (roughly the daily forecast band). Expected return range: +15% to +25% base case. Thesis breaks if Q2 shows revenue deceleration below 6%, margin compression, or debt clarification reveals aggressive/dilutive M&A rather than accretive capital return.

1-3 year view: Morningstar remains a durable data/analytics compounder with a moat rooted in trusted independent research, deep private market data (PitchBook), credit ratings (DBRS), and index products. Multi-year drivers: PitchBook expansion into private credit/M&A, Sustainalytics ESG monetization, workflow embedding via Copilot, and Indexes as a rising ETF benchmarking business. Biggest structural risk: AI-driven disintermediation of core research/ratings products — if generative AI credibly reproduces Morningstar's analyst-driven output at scale, the moat erodes. Bull-case fair value if execution holds: $220–260 range.

The core franchise remains high-quality: TTM revenue of $2.51B growing 8.4% Y/Y, gross margin of 62%, operating margin expanding to 24.2% in Q1'26 (from 20.7% in Q3'25), and ROE of 30.7%. Q1'26 delivered $644.8M revenue and $107.1M net income, with sequential margin expansion suggesting operating leverage is materializing. FCF of $453M TTM and EV/EBITDA of 10.1x are attractive for a subscription-heavy data/analytics business. The clear blemish is the balance sheet: total debt jumped from $1.03B (Q2'25) to $1.91B (Q1'26), while stockholders' equity fell from $1.61B to $1.02B — D/E now 1.87 and current ratio just 1.03. That $880M of incremental debt combined with equity contraction (likely buybacks near multi-year highs and/or M&A) is the single biggest unanswered question and needs clarification on the July 29 call. Valuation has reset meaningfully: fwd P/E 12.3x, PEG 0.71, P/S 2.52 — cheap for the quality if growth holds.

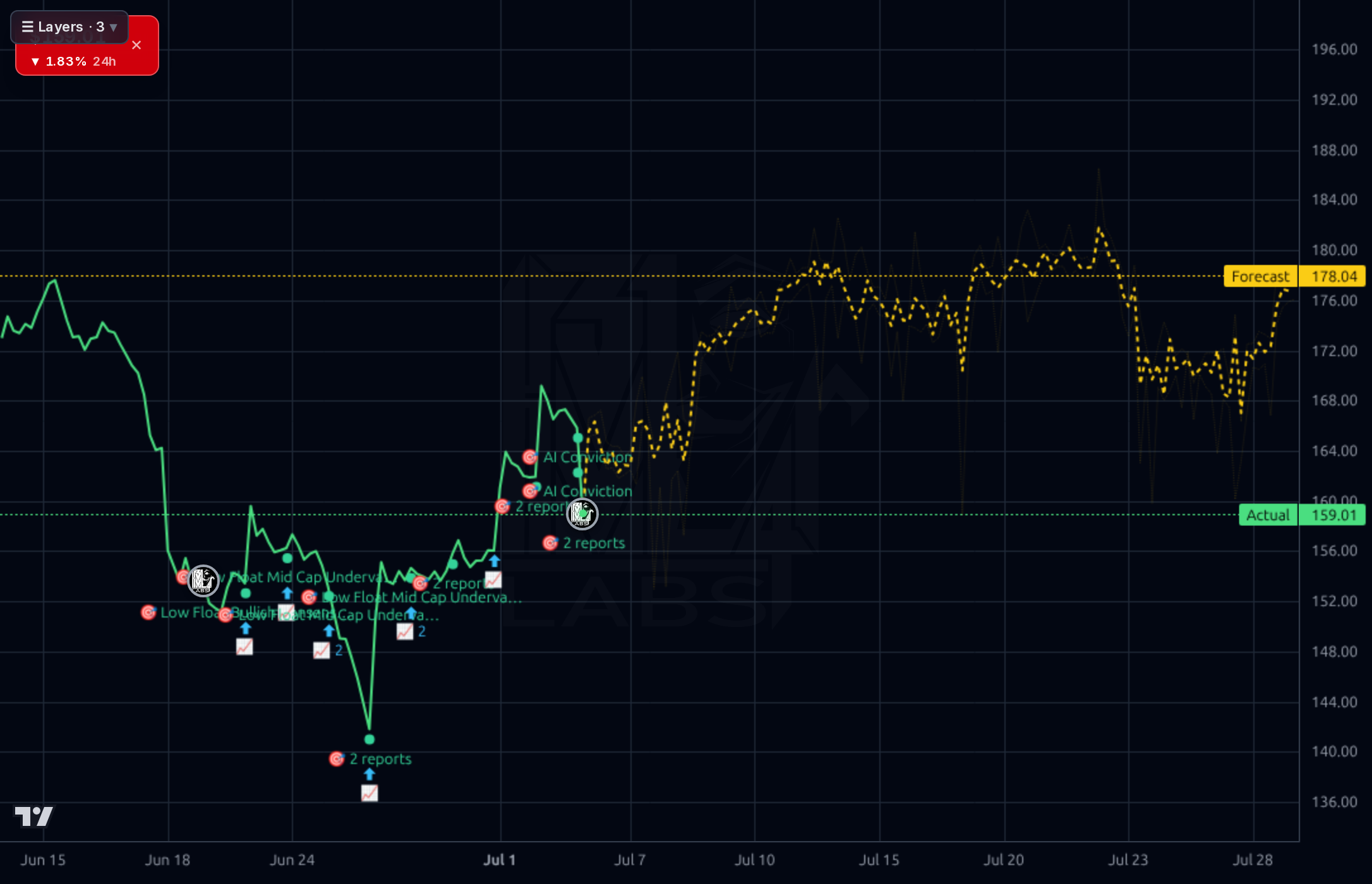

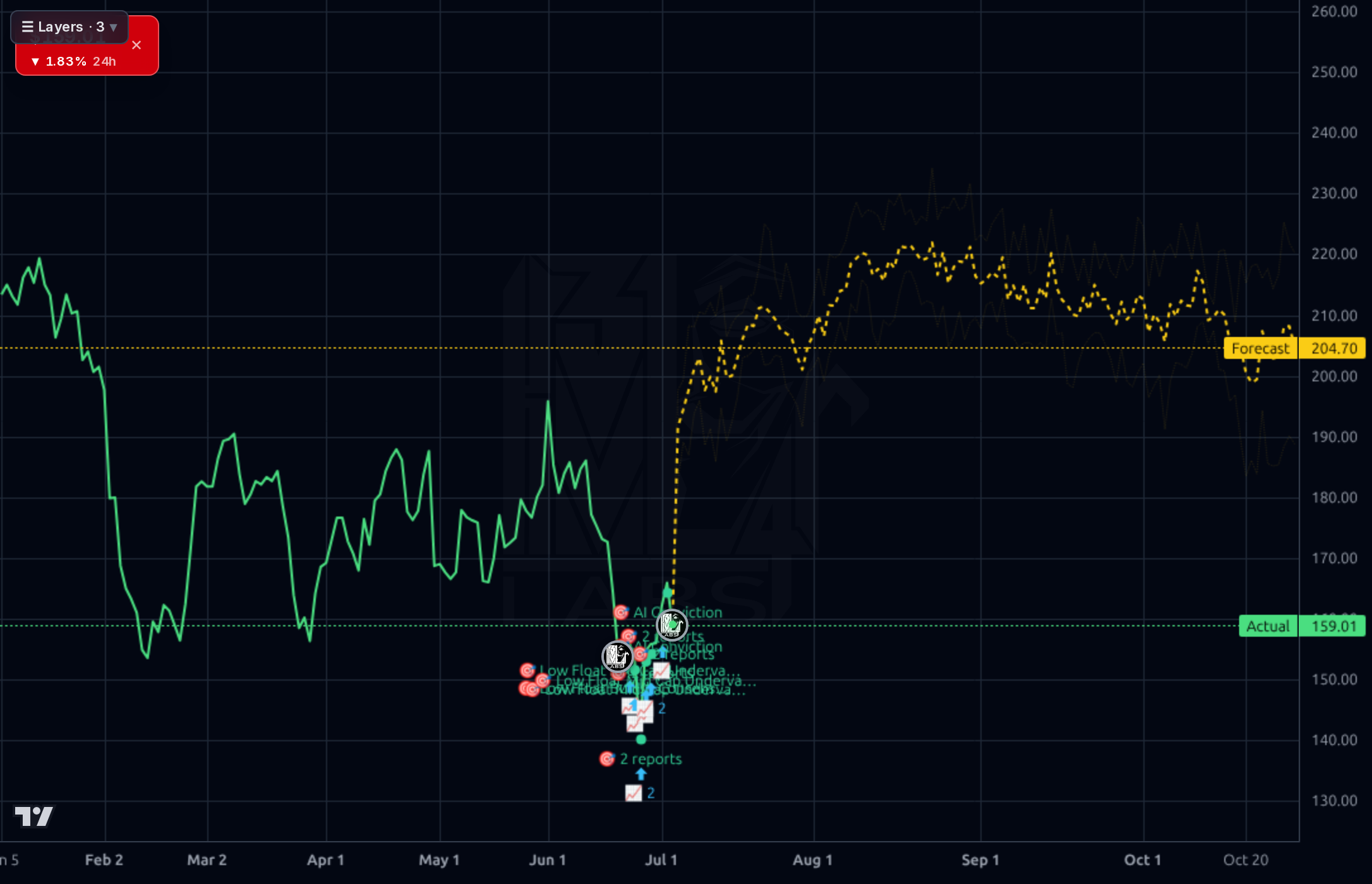

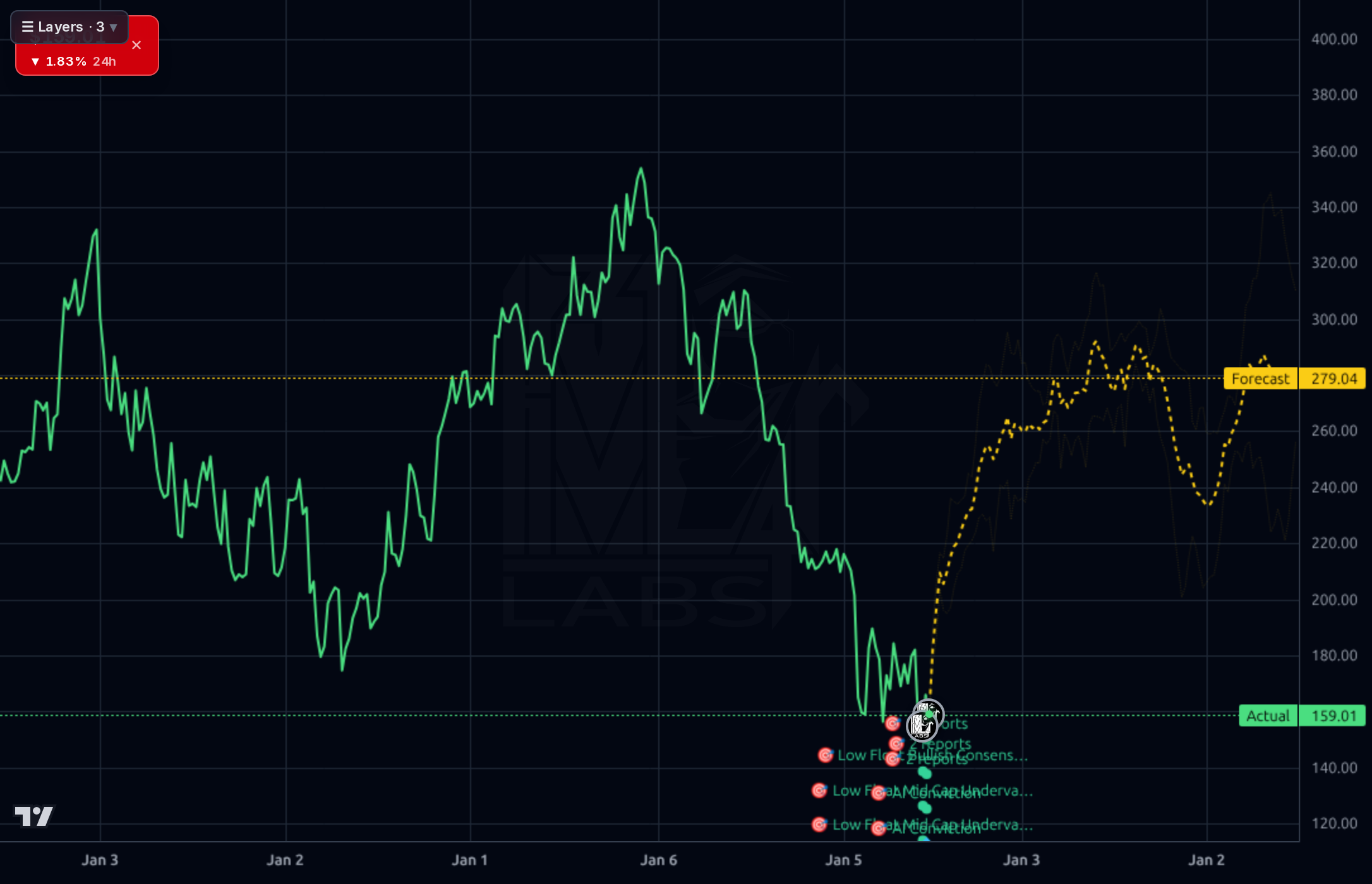

Across timeframes, MORN staged a violent selloff from ~$313 (Jan) to a $141 low in late June, then rebounded sharply to $159–165. The 1h/4h charts show a clear V-recovery with the forecast band ($178 on 1h, $185 on 4h) pointing modestly higher over the coming weeks. On the daily, the forecast band ($204) suggests mean-reversion potential toward $200+ over 3–6 months. Price sits below SMA20 (-0.55%), SMA50 (-3.83%), and well below SMA200 (-14.7%), so the longer-term downtrend is intact — this is a bounce, not yet a confirmed trend reversal. RSI 49.7 is neutral. Key resistance sits at $173 (prior consolidation zone) and $185 (forecast anchor); reclaiming $173 on a weekly close would be the first real technical confirmation. Support is $150 then the $141 52W low. The 1d model forecast has been directionally unreliable (30% vs 61% naive baseline) — discount short-term forecast; weekly signals more trustworthy.

Signal: Morningstar announced Microsoft 365 Copilot integration (research/analytics embedded in Outlook and Excel) and launched daily CLO valuation indexes with Houlihan Lokey — both extend the moat into workflow stickiness and private credit benchmarking, an underserved and growing niche. The June 29 pre-announcement confirms Q2 earnings on July 29, the pivotal near-term catalyst. Morningstar data is also being cited across financial press (loan fund AUM, alternative investment coverage, retirement planning), reinforcing brand centrality — a subtle but important indicator that the core franchise is not being disintermediated. Noise: broader market/crypto headlines are irrelevant to the thesis. The one adverse signal is a recent analyst rating drift (Recom 1.00 → 1.67), suggesting sell-side conviction is softening ahead of the print — worth respecting but not decisive given the consensus PT of $234 still implies +41% upside.

- Microsoft 365 Copilot integration embedding Morningstar research directly into Outlook/Excel — extends workflow lock-in for institutional clients

- New daily CLO valuation indexes with Houlihan Lokey — captures rising private credit benchmarking demand

- PitchBook continued expansion into VC/PE/credit/M&A coverage — highest-growth internal vector

- Operating margin expansion trajectory (20.7% Q3'25 → 24.2% Q1'26) suggests scalable operating leverage as revenue compounds

- Sustainalytics ESG data business as regulatory reporting requirements globalize

- July 29 earnings is binary — any material miss or soft guidance could retest $141 52W low

- Balance sheet leverage: debt nearly doubled to $1.91B and equity fell ~37%; D/E 1.87 with current ratio 1.0 leaves little cushion

- Recent analyst downgrade (Recom 1.00 → 1.67) suggests sell-side conviction is eroding

- 9.72% short float indicates non-trivial bearish positioning ahead of print

- AI-driven disintermediation threat to core research/ratings franchise over 3-5 years

- Longer-term downtrend intact — price below SMA200 by 14.7%; current bounce not yet confirmed as reversal

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord