MSFT— AI Stock Forecast & Price Targets

Published 7/8/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live MSFT price forecast →

Microsoft remains fundamentally strong due to its dominant cloud and AI positioning (Azure/Copilot), but near-term valuation is pressured by high AI capex intensity leading to FCF compression. The stock appears to be in a mean-reversion setup, making accumulation during pullbacks prudent while awaiting confirmation of sustained revenue conversion from AI investments.

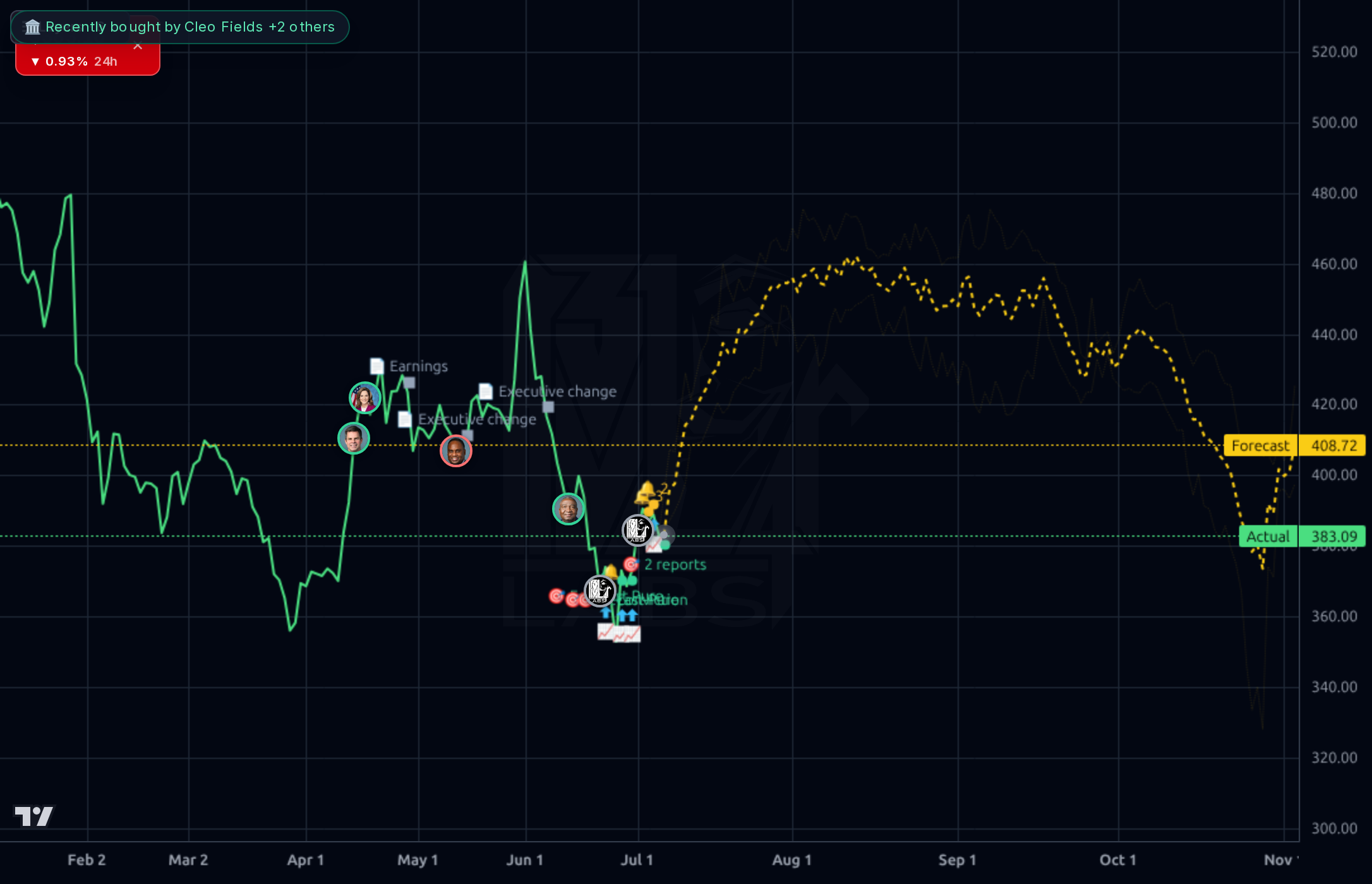

Accumulate on dips toward the $349.2 (52W Low) or near-term support levels identified by technical analysis, treating any immediate move as noise given the upcoming earnings event. Do not size a swing trade into the earnings date itself.

Maintain an ACCUMULATE bias over the next 1-6 months. The thesis hinges on Azure/Copilot monetization accelerating to ease FCF compression. A break above $420 with strong volume would signal renewed confidence in the AI revenue conversion cycle.

The long-term structural thesis remains intact: MSFT is a compounder built on enterprise dominance. The primary risk is if the high capex intensity continues without commensurate margin expansion, forcing a multiple contraction despite operational strength.

The fundamentals are best-in-class: high profitability (39.34% Profit Margin) and strong returns (ROE of 34.01%). Revenue growth remains robust (Sales Y/Y TTM: 17.87%), supported by consistent quarterly increases in revenue, though the cash flow picture shows a significant strain, with Free Cash Flow compressing from $25.6B (Q3 '25) to $15.8B (Q1 '26) due to high capex ($19.4B to $30.9B). The balance sheet remains fortress-like (D/E: 0.30), supporting this aggressive AI investment cycle.

The stock is showing signs of consolidation near key support, as suggested by the recent price action relative to the forecast bands on both charts. While the long-term trend appears broken (SMA200 at -12.47%), the short-term momentum suggests a potential bounce or mean reversion towards historical averages. The model's 1-week directional accuracy is better than its 1-day reading, suggesting caution on immediate breakouts but acknowledging underlying strength.

The news flow highlights AI as the primary secular driver, with mentions of Xero integrating Microsoft 365 and Commvault expanding its Azure partnership. However, the market narrative seems to be grappling with MSFT's recent dip relative to GOOGL's massive gains (+108% over a year), suggesting investor focus is on how quickly AI capex translates into visible revenue acceleration rather than just capability.

- Azure/Intelligent Cloud growth fueled by enterprise AI workloads and partner ecosystem attach.

- Copilot seat penetration driving direct margin tailwinds within productivity suites (Excel/Outlook).

- Verticalized AI revenue streams through strategic partnerships like Mayo Clinic for healthcare AI models.

- FCF compression due to high, sustained AI capex spending outpacing immediate FCF generation.

- Valuation risk if the market discounts the current multiple based on perceived slowdown in near-term AI monetization.

- Macro/geopolitical uncertainty (oil prices, trade tensions) exposing MSFT's beta of 1.13.

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord