OLLI— AI Stock Forecast & Price Targets

Published 7/9/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live OLLI price forecast →

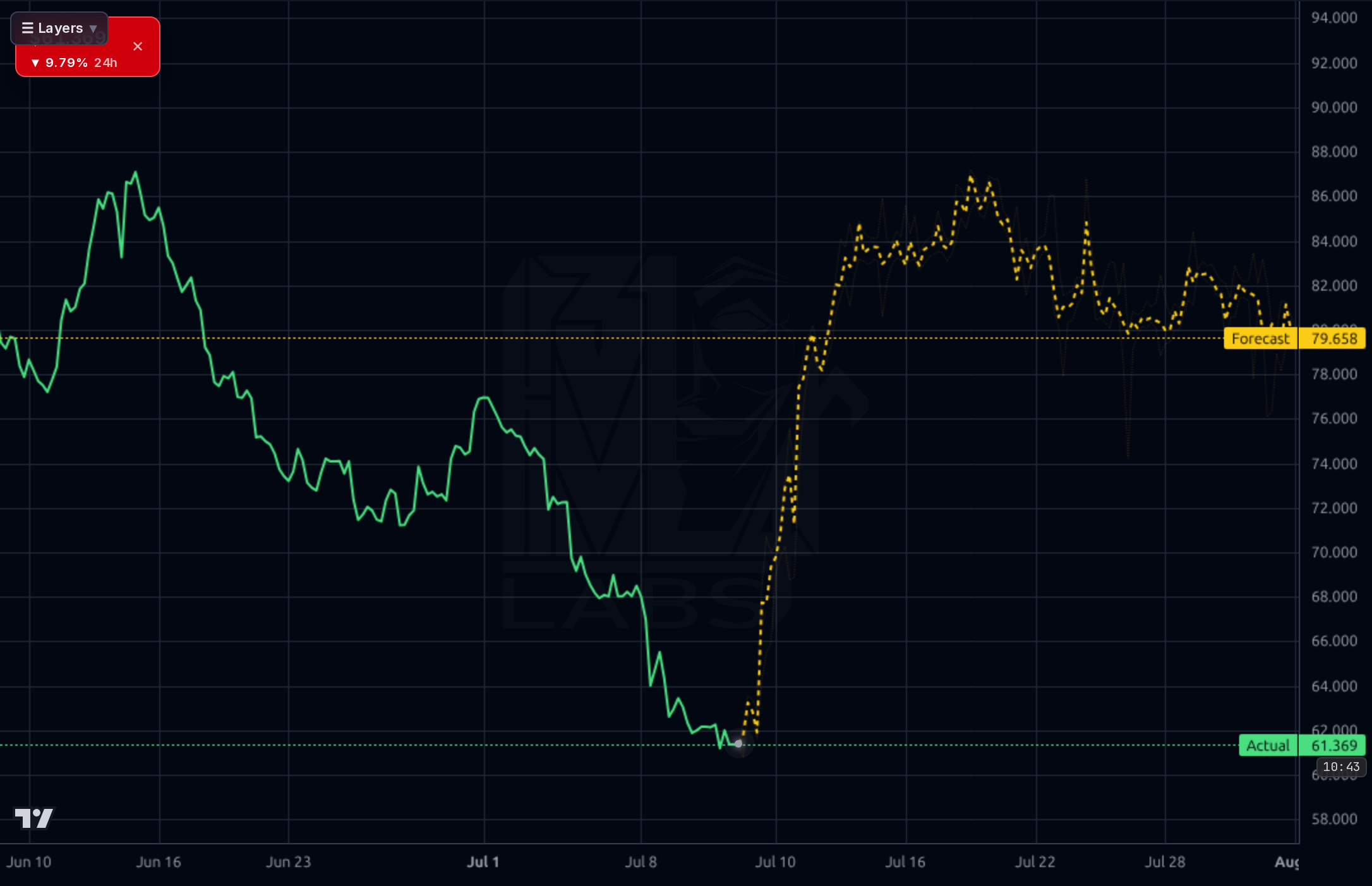

OLLI has cratered to $61.88 (-9% today, -51% YoY, -44% YTD) after a JPMorgan downgrade to Neutral with PT cut from $152 to $70, dragging the stock to a fresh 52-week low with RSI 28 and price 41% below the 200-day SMA. Fundamentals remain intact — 16.7% TTM sales growth, 39% gross margin, $250M cash, 13.8% ROE — but the sentiment shift, rising short float (8.5%→10.6%), and consensus PT reset make this a staged accumulation, not a catch-the-knife trade. Base case sees $85–90 within 9 months as oversold conditions unwind toward a still-reset analyst view; downside to $50–55 is real if August earnings disappoint.

1-4 weeks: do NOT chase a bounce. Price is in freefall on a fresh downgrade with RSI 28 and 3.27x volume — oversold can stay oversold. Wait for either (a) a daily close back above $70 to confirm the downgrade is priced, or (b) a re-test of $55–58 on lower volume for a first tranche. Any starter position should be ≤25% of intended full size, with hard invalidation on a weekly close below $55. Avoid front-loading; the analyst-target overshoot pattern (prior base $92 sits +33% above live) and 0/3 recent directional accuracy on this name argue for patience over conviction.

1-6 months: staged accumulation zone $55–68 targeting a mean-reversion move toward $80–90 into and out of the August 27 earnings print. The core mid-term thesis is that gross margin held at 41.9% last quarter, sales grew 14% Q/Q, and forward P/E at 12.2x already discounts a significant growth slowdown — so an in-line print with stable comps could catalyze a 20–30% snap-back. What would change my mind: negative comps, gross margin compression below 39%, or management flagging tariff/sourcing headwinds. Expected return range from a $60 average cost: +30% base / -10% bear over 6 months.

1-3 years: OLLI's structural story — sourcing tailwinds from retail bankruptcies, disciplined new-store unit economics, 14% projected 5Y EPS growth, and a debt-light balance sheet — remains intact and is a plausible compounder at these prices. Terminal thesis: if the company can grow revenue mid-teens and hold margins, mid-teens EPS growth on a re-rated 18–20x multiple gets to $110–130 over 24–36 months. Biggest structural risk is Walmart/Amazon encroachment eroding the closeout-sourcing moat, particularly if a normalization in retail bankruptcy activity dries up inventory availability. Secondary risk: management execution as the store base scales and unit economics of newer geographies dilute company averages.

The underlying business remains healthy despite the tape. TTM revenue is $2.73B with Y/Y sales growth of 16.7% and most recent quarter sales +14.3% Q/Q comparable. Gross margin held at 41.9% in the April quarter versus 39.1% Finviz-blended, operating margin 11.5%, and net margin 8.6% — all consistent with prior years and inconsistent with a business in structural decline. Balance sheet is strong: $197.7M cash, $710M total debt (largely lease-related), 2.32 current ratio, book value $31/sh. TTM FCF of $136M against a $3.74B market cap gives a ~3.6% FCF yield, and ROE of 13.8%/ROIC of 10% show capital discipline. Q4 (Jan) net income of $85.6M was the seasonal peak and Q1 (Apr) came in at $56.4M, so trailing earnings power ($4.04 EPS TTM, $5.08 forward) is not collapsing. What's arguably 'broken' is not the P&L — it's the market's willingness to pay the historic multiple, with forward P/E compressing to 12.2x and PEG 0.86 as growth expectations reset lower.

The chart is deeply broken across every timeframe. Weekly view shows a top near $141 in early 2025 followed by a persistent lower-highs/lower-lows sequence into today's $61.88 print — a ~56% peak-to-trough drawdown. Daily shows the stock breaking down through $75 in early July and gapping lower on the JPMorgan downgrade, closing 17.8% below the 20-day, 21.5% below the 50-day, and 40.8% below the 200-day SMA. RSI at 28.4 is oversold, relative volume 3.27x, and today's -9% candle on heavy volume screams capitulation rather than orderly distribution. Support: the actual 52-week low prints at $61.61 (essentially tagged today) and the June 2020 zone around $55 is the next visible shelf. Resistance is dense — $70 (prior-day close and new PT), $75 (breakdown pivot), then $85–90 (June consolidation base). The 1h/4h Kronos forecast bands suggest a mean-reversion bounce toward $79–103, but calibration is poor: realized 1d directional accuracy is 18% versus 83% naive baseline, and 1wk MAPE 10% with 17% directional accuracy — the model is beaten by naive and its bullish tilt should be heavily discounted.

The dominant catalyst is JPMorgan's downgrade from Overweight to Neutral with a PT slashed from $152 to $70 (Boss), which is the proximate cause of today's -9% move and the 52-week low print. Secondary coverage (Yahoo, Barchart) frames the setup as a contrarian opportunity given positive comps, loyalty growth, healthy margins and a 14.1x forward P/E, but also flags a looming 'death cross' — technically valid given the SMA distances. Broader tape context is negative: Iran ceasefire jitters, S&P down, and multiple 52-week lows (STLA, OLLI, SMR) suggest sentiment-driven selling, not company-specific news flow beyond the sell-side reset. Signal versus noise: the JPM downgrade is real signal because it recalibrates the sell-side high-water mark and likely pulls the mean consensus PT (currently $114.73) meaningfully lower over coming weeks. The 8-K on June 15 was just the annual meeting vote (Item 5.07) — administrative, not a catalyst. Retail sentiment on X/Stocktwits is bullish/contrarian, and the WhatsApp-group spam pattern is a mild negative tell for a potential retail-driven false bottom.

- New-store expansion — OLLI has continued double-digit revenue growth with 16.7% TTM sales, implying ongoing unit additions from the ~500+ store base

- Loyalty program growth ('Ollie's Army') cited in Barchart coverage as a durable moat driver supporting comp performance

- Sourcing tailwind from ongoing retail distress (2025-2026 bankruptcy cycle) feeding closeout inventory into stores at attractive GMs

- August 27 earnings print as a near-term catalyst to either validate resilient comps or force a further reset — either resolves the current uncertainty

- Forward EPS of $5.08 (vs $4.04 TTM) implies ~26% forward earnings growth already embedded in guidance/consensus

- JPMorgan downgrade to $70 PT likely triggers follow-on cuts from the ~1.44 Recom consensus, pulling the $114.73 mean target down and removing a key sentiment support

- Short float rose from 8.5% to 10.6% in ~45 days — bearish conviction is building, not peaking, and could accelerate on any weak August print

- Technical damage is severe: -40.8% below 200-day SMA, imminent death cross, and no visible support until $55 zone

- Competitive encroachment from Walmart and mass-market discounters remains the primary secular threat to the closeout model

- Historical model forecast accuracy on OLLI is 18% directional versus 83% naive — the visible Kronos bullish reversion signal should be discounted heavily

- August 27 earnings is 49 days out — a long runway of tape risk with a bearish sentiment overlay

- Analyst targets have systematically overshot realized moves on this name; the reset from $152 to $70 by JPM is a warning that other desks may follow

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord