PEGA— AI Stock Forecast & Price Targets

Published 7/6/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live PEGA price forecast →

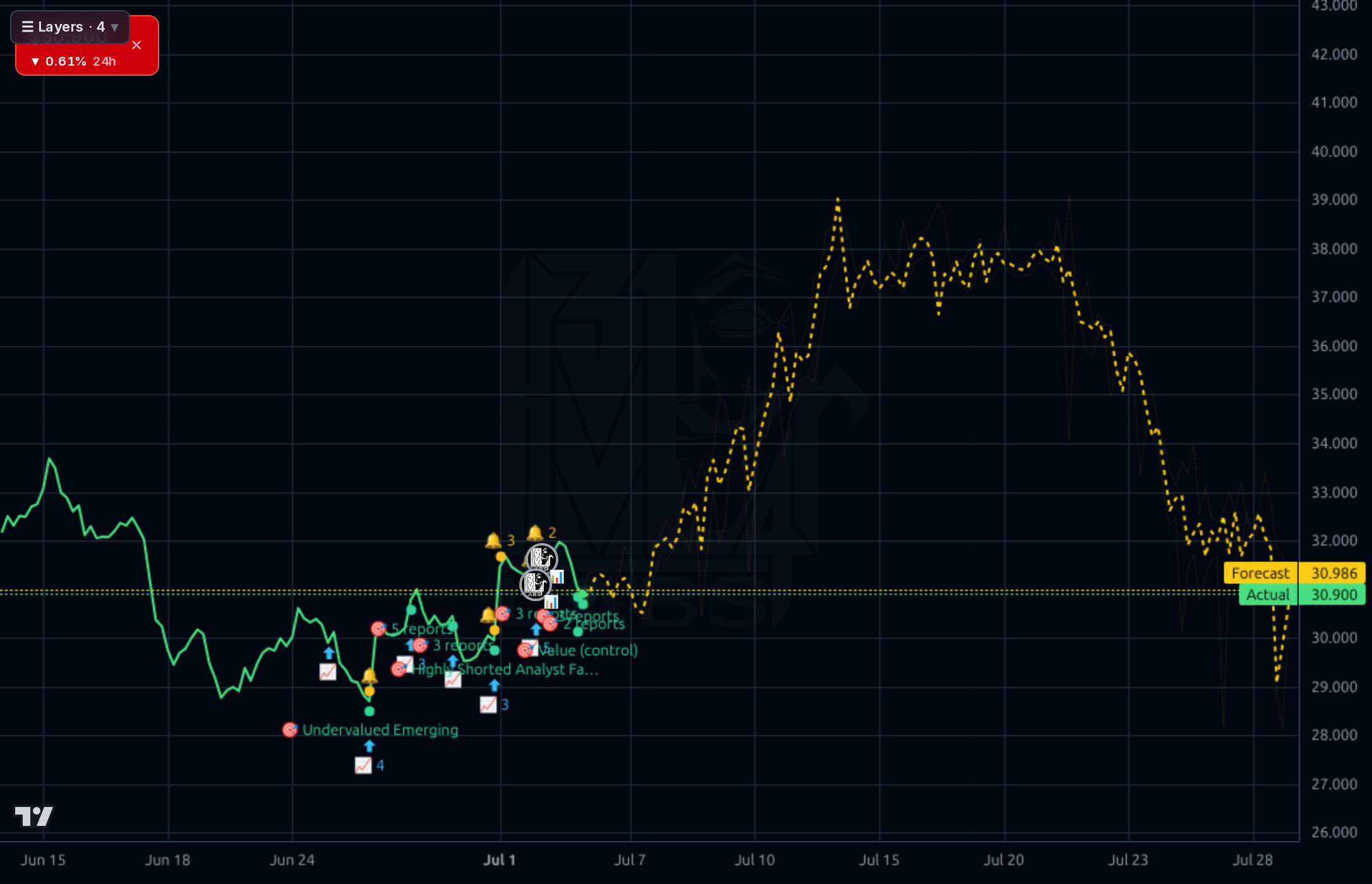

PEGA at $30 offers a genuinely cheap valuation (fwd P/E ~10x, PEG 0.56) backed by $533M TTM FCF, 52% ROE, and a net-cash balance sheet, but sits in a brutal downtrend (-48% YTD, -35% below 200-SMA) with Q/Q revenue -9.6% and EPS -59.5% deceleration heading into a binary July 21 earnings print. The setup is a value-with-catalyst accumulation zone near the $28.66 52W low, but position sizing must respect that past bull targets have systematically failed to print and the model's directional accuracy is worse than a naive baseline.

Neutral-to-constructive but do NOT size into earnings. With the July 21 print ~15 days out, this is a binary IV-crush event. If already long, hold a starter tranche near $29-30 with stop below $28.50 (loss of 52W low invalidates the setup). If flat, wait for the print or take a small pre-earnings speculative position (<25% of intended size). Key levels: support $28.66, resistance $32/$34. Earnings is the invalidation — a guide cut that breaks $28.66 opens $24-25; a beat/raise can gap the stock to $34-36 quickly given 15% short float.

ACCUMULATE on weakness with a 6-12 month view. Base case: earnings clears the deceleration bar, Solution Designer/MCP adoption metrics show early traction, and the stock re-rates to $34-38 (11-12x forward EPS of $3.04). Bull case: capital return acceleration (buyback given net cash) + AI ACV inflection drives $44 (14x fwd EPS). Bear case: revenue deceleration continues, guide cut, $24 (7-8x fwd EPS). Expected return range: -20% to +45%, skewed positive from current $30. Change my mind if Q2 Pega Cloud ACV growth decelerates below high-single-digits or if operating margin stays sub-10%.

Terminal thesis rests on whether PEGA becomes a durable AI workflow orchestration layer for regulated enterprises (finance, healthcare, government) where its Situational Layer Cake and governance features are genuinely differentiated versus Salesforce Agentforce and ServiceNow. If yes, this is a $60-80 stock in 2-3 years on mid-teens EPS growth and multiple expansion to 15-18x. Biggest structural risk: hyperscaler AI commoditization of workflow orchestration collapses PEGA's moat, turning it into a legacy BPM vendor with terminal decline. Founder-led (Trefler still owns ~46%) provides strategic patience but also key-person risk.

PEGA's fundamentals show a classic quality-vs-deceleration split. On the quality side: TTM revenue $1.70B with 75% gross margins, $533M free cash flow (P/FCF ~10x), ROE 51.7%, ROIC 44.7%, net cash position (~$474M cash vs $72M debt), and a low PEG of 0.56. Q1 2026 delivered $430M revenue with $206M operating cash flow — cash conversion is elite. However, the deceleration is real: Q/Q revenue -9.6%, EPS -59.5%, and TTM sales growth just +3.5%. Q1 operating margin compressed to 8.6% from 24.9% in Q4 2025 (seasonally lumpy but still concerning). Capital allocation is conservative — small dividend (0.39% yield, 4.9% payout) with 45.9% insider ownership suggesting founder-led discipline but limited buyback aggression given the depressed price. Forward P/E of 10x and analyst target of $58.50 imply the Street still believes in EPS recovery, but the burden of proof now sits on the July 21 print.

Across all timeframes the picture is bearish-to-basing. The 1D and 1WK charts show PEGA collapsed from ~$68 highs to $30, sitting -34.7% below its 200-SMA, -8.4% below the 50-SMA, and -2.1% below the 20-SMA. Perf YTD -48%, Perf 6M -49%, Perf Quarter -27%. RSI(14) at 43.8 is neutral, not oversold — no capitulation signal. Price is testing the $28.66-$30 support shelf that has held on prior tests; the 1H chart shows a modest bounce from $29 with resistance at $32. The Kronos forecast band is aggressively bullish (1D forecast $30.99, 4H shows sharp rebound to $53, 1WK $38), but realized directional accuracy at 42% is BELOW the 58% naive baseline — the model is unreliable in this regime and its upside should be heavily discounted. Key levels: support $28.66 (52W low, must hold), resistance $32/$34/$36 (prior failed reclaim zones). Short float 15.3% adds squeeze optionality if earnings surprise up.

Signal: multiple recent pieces frame PEGA as an AI orchestration play — Solution Designer Initiative (June 24) and Pega Blueprint methodology are concrete product launches aimed at bridging business intent with technical execution. D.A. Davidson reiterated Buy with $55 target (June 10), and Simply Wall St/Yahoo pieces (July 5) explicitly argue the stock is cheap given earnings power. Guggenheim's July 2 upgrade of Salesforce/ServiceNow to Buy provided a sector-wide bid that lifted PEGA (Perf Week +8.1%). Noise: WhatsApp group spam on social, generic robotics list-inclusion. The two 8-K filings (June 8 guidance/Reg FD and June 18 material event/shareholder vote) are routine but worth flagging. Net: narrative is turning constructive on AI monetization, but no fundamental datapoint yet validates the story — that comes July 21.

- Solution Designer Initiative (launched June 24) — new practitioner enablement program to bridge business intent and technical execution using Pega Blueprint methodology

- Pega GenAI Blueprint for rapid application prototyping — direct monetization of AI development workflow within existing platform

- MCP (Model Context Protocol) integration positioning PEGA as governance-preserving orchestration layer for enterprise AI agents

- Pega Cloud transition continuing to shift revenue mix toward higher-quality recurring ACV

- July 21 earnings expected to include AI adoption metrics and forward guidance — potential re-rate catalyst if Pega Cloud ACV reaccelerates

- Q/Q revenue -9.6% and EPS -59.5% indicate real demand deceleration that must reverse on July 21 print or the value case breaks

- Hyperscaler competition (Salesforce Agentforce, ServiceNow) risks commoditizing AI workflow orchestration — PEGA's differentiation unproven at scale

- Structural downtrend intact: -35% below 200-SMA, -48% YTD; no reclaim of $34-36 resistance shelf has held despite multiple attempts

- Kronos forecast model directional accuracy (42%) is below naive baseline (58%) — model's bullish signal is unreliable in current regime

- Q1 operating margin compressed to 8.6% from 24.9% in Q4 — margin volatility raises quality-of-earnings concerns

- Founder/insider concentration (46% insider ownership) creates governance and key-person risk

- Binary earnings event 15 days out with high implied volatility — gap risk in either direction

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord