PSIX— AI Stock Forecast & Price Targets

Published 6/29/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live PSIX price forecast →

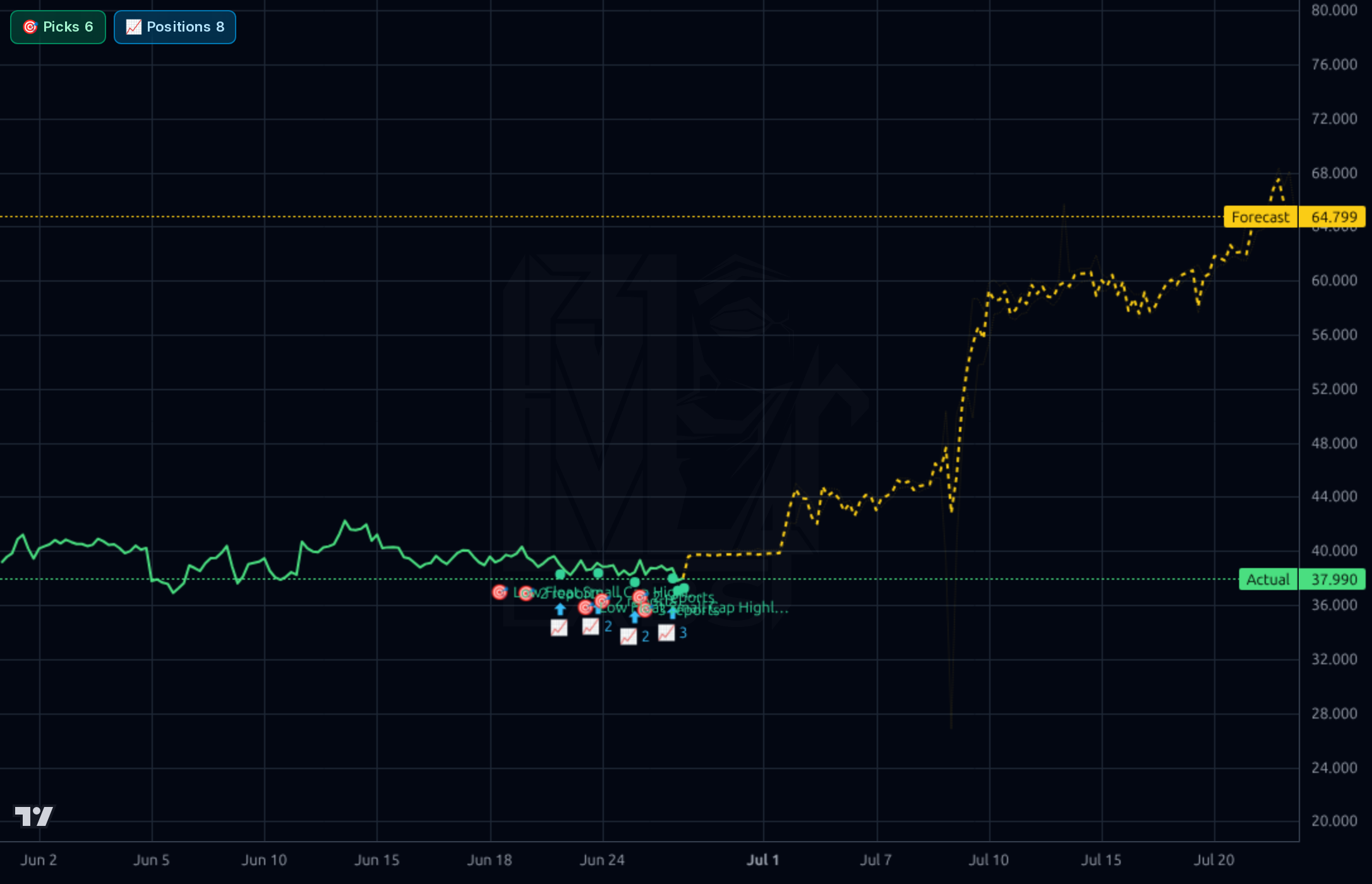

PSIX is a previously-hyped AI/data-center power play that has round-tripped from $110+ to $38 on margin compression, a guidance cut, and growing skepticism about the durability of its data-center exposure. Fundamentals remain genuinely strong (TTM P/E 8.6, ROE 76%, ROIC ~30%, net cash flow positive), but Q1 FY26 showed revenue -5% YoY and EPS -62% QoQ, validating the bear case on cyclical normalization. With the stock near 52-week lows, 20.5% short interest, and analyst target of $70, this is a contrarian setup with high asymmetry but real fundamental deterioration — accumulate cautiously, not aggressively.

1-4 weeks: Tactical long bias near $36–$38 with stop below $35.50 (loss of 52-week low). 20.5% short float + 2.35 days-to-cover + RSI 38 + multiple Kronos short-horizon forecasts pointing higher set up a potential squeeze. Position size small (1-2% portfolio) given the broken chart. First target $44–$46 (gap fill/May breakdown), stretch $55. Invalidation: a daily close below $35.50 on volume — that opens the door to the $22 zone the 1d model is targeting.

1-6 months: This is a 'show me' story. The thesis pivot — will the AI/data-center genset business actually re-accelerate, or was Q1 FY26 the first of several down quarters — gets decided on the next 1-2 earnings prints (May 11 AMC is the next catalyst). Expected return range: -30% to +60%. Bull case requires a guidance raise and gross margin recovery back above 25%; bear case is another revenue miss confirming the cyclical roll-over. What would change my mind to outright BUY: gross margin stabilization at 24%+ and any data-center order commentary. What would push to SELL: another -5% revenue print or further margin contraction below 22%.

1-3 years: If PSIX genuinely captures a meaningful slice of behind-the-meter / data-center backup power demand, current $876M market cap on $715M revenue is cheap — the bull case is multi-bagger from here. Structural drivers: aging US grid, data-center power scarcity, microgrid/standby growth, EPA-certified large engines as a moat. Biggest structural risk: PSIX is fundamentally an engine OEM with ~24% gross margins and cyclical industrial demand — not a software/AI-margin business. If the data-center narrative deflates, this re-rates to a 6-8x EBITDA industrial cyclical (~$25–$30), not a growth multiple. Concentrated insider ownership (63%) and governance flags raise the long-tail risk of value destruction.

The headline ratios look exceptional — trailing P/E 8.57, forward P/E ~9.9–11.4, P/S 1.22, ROE 75.7%, ROIC 29.8%, profit margin 14.3%, and TTM sales growth +38.6%. Balance sheet is healthy: $45M cash, $167M debt, current ratio 3.42, working capital ~$194M, and stockholders' equity has grown from $135M (Jun 2025) to $186M (Mar 2026). However, the quarterly trajectory is the problem: revenue fell from $204M (Q3'25) and $191M (Q4'25) to $128.6M in Q1'26, gross margin compressed from 28.2% (Q2'25) to 22.9% (Q1'26), operating income collapsed from $32.5M to $11.4M, and net income from $51M to $7.3M. This is the textbook fingerprint of a cyclical/order-flow peak. EPS Q/Q -61.8% and Sales Q/Q -5.1% confirm. FCF turned positive again in Q1'26 ($17.2M), which is encouraging, but TTM FCF is barely breakeven (-$0.2M) and P/FCF is 35x — the optical P/E is flattered by a peak earnings quarter that's already rolling off. Insider ownership at 63% is a double-edged sword (alignment, but governance concerns flagged in news).

All three timeframes show a broken parabola. The weekly chart shows the classic blow-off: a run from sub-$5 to $110, followed by a violent collapse to $38 — price is now -68.8% from the 52-week high of $121.78 and just 6% above the 52-week low of $35.77. Daily shows the breakdown in May, sideways base at $36–$40 through June, with SMA20 -3.8%, SMA50 -27%, SMA200 -45% — every moving average is overhead resistance. RSI 38.6 is weak but not yet oversold. The Kronos forecasts diverge sharply by horizon: 1h and 4h models predict a sharp move up to $55–$65 (bull case re-rate), but the 1d model predicts continued decline toward $22 — and crucially, the 1d directional accuracy (57%) is BELOW the naive baseline (93%), so that bearish forecast should be heavily discounted, while the shorter horizons (where the model has been hot but with limited samples) suggest a near-term squeeze. Key levels: support $35.77 (52w low) is the line in the sand; resistance $44–$46 (May breakdown), then $55 (analyst target zone, prior consolidation).

Signal: The June 24 Insider Monkey piece confirms PSIX is a top holding (#8) in Leopold Aschenbrenner's Situational Awareness AI-themed fund with a $26.3M stake — this is the real institutional anchor for the AI/data-center thesis. ChartMill (Jun 20, Jun 24) flags deep value (P/E 8.7, strong fundamentals). The June 29 EDF Power Solutions divestiture to KKR is unrelated to PSIX (different company, similar name) but could create confusion/headline volatility. Noise/negative: Jim Cramer told a caller to cut losses after the Q1 miss and lowered guidance (June 4). Seeking Alpha downgrade June 17 explicitly cites the Q1 revenue -5.1% and margin contraction — this is the bear's smoking gun. Seeking Alpha June 16 piece raises governance concerns and questions the data-center exposure narrative as 'muddied by conflicts of interest.' The crowd sentiment on X is notably skeptical even from bulls ("pessimistic on actual real participation in BTM opportunity"), which is contrarian-friendly for accumulators but confirms the AI narrative is under genuine threat.

- Data-center / behind-the-meter standby power: stationary gensets for data centers explicitly named in company description; if AI buildout continues, large-engine genset demand is a multi-year tailwind

- Microgrid and renewable resiliency power systems — secular grid-reliability theme

- EPA-certified spark-ignition large engines for prime/standby — regulatory moat in a tightening emissions regime

- School bus / transit / vocational truck powertrain — alt-fuel ICE transition as a longer-cycle replacement market

- Margin recovery optionality: if revenue mix shifts back toward higher-margin power systems (Q2'25 ran 28% gross margin), operating leverage could surprise to the upside

- Q1 FY26 revenue -5.1% YoY and EPS Q/Q -61.8% — earnings momentum has clearly broken

- Gross margin compression from 28.2% (Q2'25) to 22.9% (Q1'26) suggests pricing power / mix deteriorating

- Seeking Alpha flagged governance and conflict-of-interest concerns around the AI/data-center narrative — credibility risk

- 20.5% short float and 63% insider ownership = very thin true float (~7-8M shares), violent two-way moves on any news

- Stock down 44% YoY, -45% from 200-day SMA — momentum/technical traders are sellers on every rally

- Cyclical industrial exposure: if North American capex slows, gensets and industrial engines roll over fast

- Jim Cramer 'cut your losses' commentary and lowered guidance create overhang for retail flows

- Kronos 1d model directional accuracy (57%) is below naive baseline (93%) — the model is unreliable in this regime

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord