PSIX— AI Stock Forecast & Price Targets

Published 7/6/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live PSIX price forecast →

PSIX is a deep-value industrial (TTM P/E 8.4, ROE 76%) that has round-tripped from $121 to ~$37 as the AI/data-center power narrative unwound, with Q1 FY26 showing revenue -5% YoY, gross margin compression from ~28% to ~23%, and EPS Q/Q -62%. The setup pairs genuine cheapness and a strong balance sheet with deteriorating momentum, a 20.5% short float, and a binary Aug 6 earnings print — a HOLD into the print with $35.77 as the line-in-the-sand invalidation.

HOLD into the Aug 6 earnings print — do not front-run confirmation. The stock is pinned near $35.77 support with 20.5% short float and 63% insider ownership (thin ~7.3M float), creating squeeze potential on any positive surprise but also gap risk on a miss. Trading range likely $35–41 pre-print. Tactical plan: only nibble on a decisive reclaim of $40 with volume; a clean break of $35.77 invalidates the value case near-term and opens $30. Do NOT size a swing into the binary print; if you must be long, keep size small and hedge with puts given IV will crush post-print either way.

1-6 months hinges entirely on Aug 6 guidance. If management confirms margin stabilization and reaffirms a return to the $190M+ quarterly revenue run-rate, the stock can re-rate toward $45–50 as forward P/E compresses back to a more normal 12–14x on $3.32 EPS. If guidance confirms further margin compression and softer end-market demand (data-center AI power in particular), the value trap deepens and $28–30 is the next stop. Base expectation is a wide-tailed distribution centered around $40. What changes my mind: two consecutive quarters of gross margin stabilization above 24%, or explicit multi-year contract wins in stationary genset/microgrid that de-risk the top line.

1-3 year terminal thesis is that PSIX is a diversified engine/power-systems platform levered to structural themes (backup/prime power for microgrids and data centers, transit/school bus electrification, aftermarket recurring revenue) with best-in-class returns on capital when it executes. At 8x earnings with 76% ROE, a normalized $4–5 EPS and a 12–15x multiple gets you $50–70. The biggest structural risk is that the recent margin compression is not cyclical but reflects a permanent mix shift or loss of pricing power against larger integrated competitors (Cummins, Generac, Caterpillar); secondary risk is governance/related-party overhang from majority insider ownership, which caps the institutional multiple this name can achieve regardless of fundamentals.

The valuation screen is genuinely cheap: trailing P/E 8.4, P/S 1.19, P/B 4.6, EV/EBITDA 9.5, with ROE 75.7%, ROIC 29.8%, and profit margin 14.3% — elite returns for a specialty industrial. But the direction of travel is the problem. Q1 FY26 revenue printed $128.6M vs. Q2/Q3/Q4 2025 in the $191–204M range, a sharp sequential step-down (-5% YoY per news), with gross margin compressing to 22.9% from 28.2% in Q2 2025 and operating margin dropping to 8.9% from 16.9%. EPS Q/Q -61.75% confirms the earnings roll-over. The balance sheet is the mitigating factor: cash $45M, total debt $168M, D/E ~0.90 (improving), current ratio 3.42, working capital ~$194M, and Q1 FCF turned positive at $17.2M after a negative Q4. Forward EPS $3.32 vs. trailing $4.42 implies the sell-side already models the earnings step-down. Capital allocation shows no dividend and no evident buyback despite management/insider ownership of 63% — a governance flag also raised in recent coverage.

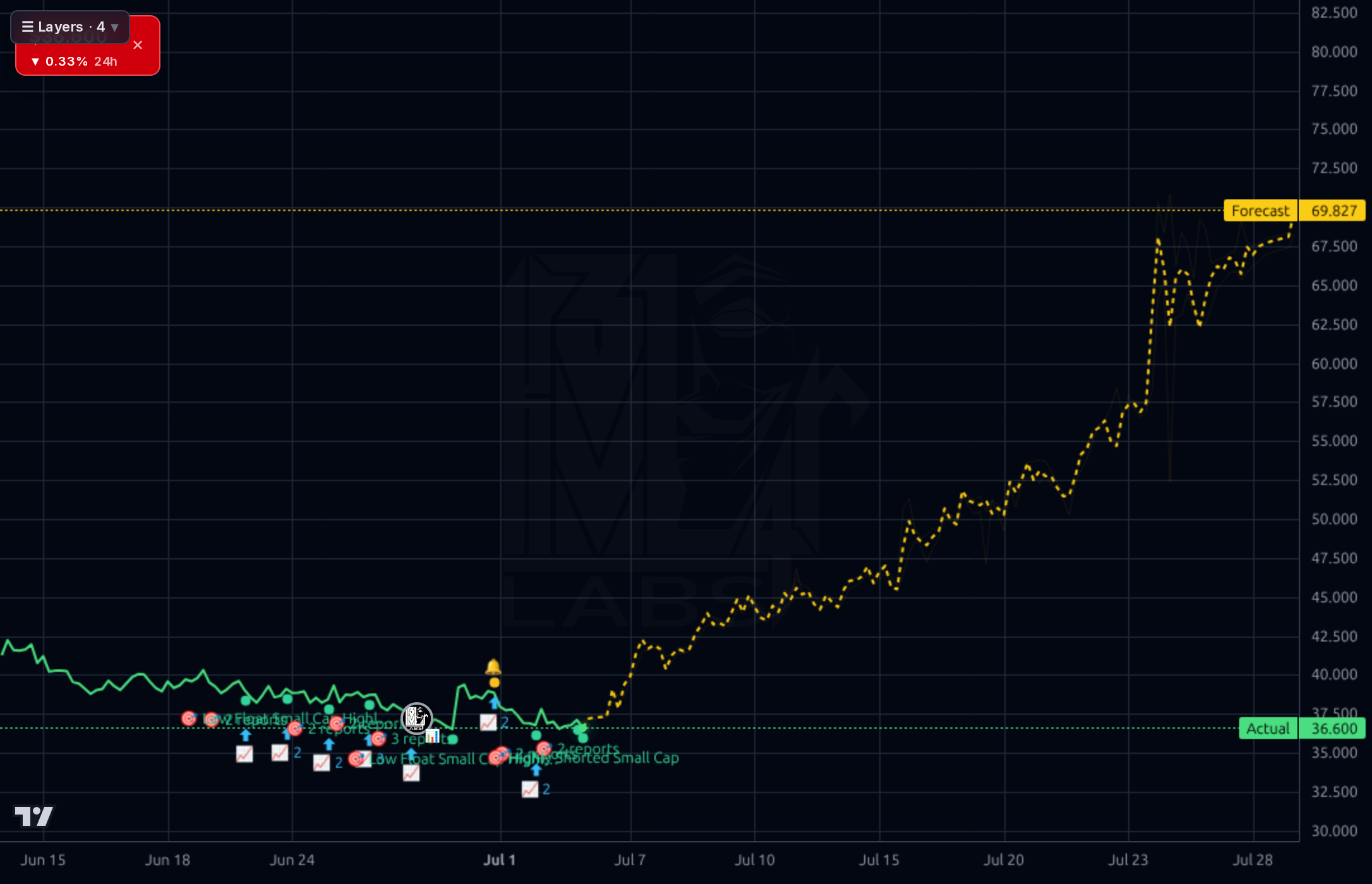

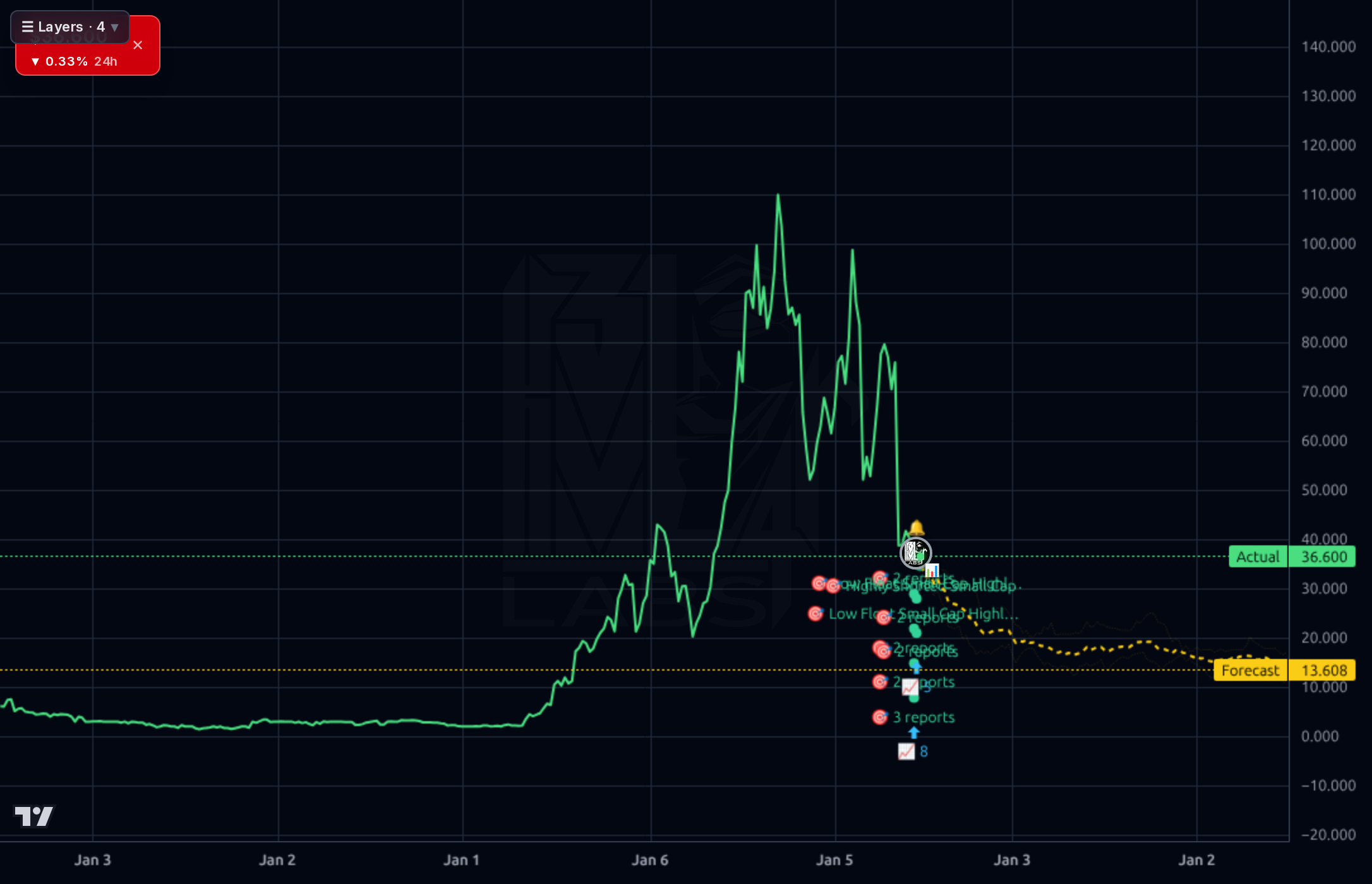

Across timeframes the picture is uniformly weak. The 1D/4H views show price sitting at $36.81, essentially on the 52-week low of $35.77, with SMA20 -4.5%, SMA50 -23.9%, and SMA200 -45.4% — a textbook stage-4 downtrend. Perf YTD -35%, Perf Quarter -44%, Perf Half-Year -37%. RSI 39.8 is weak but not yet oversold enough to force a bounce. The weekly chart makes the round-trip explicit: parabolic run to $110+ then a controlled unwind to the mid-$30s. The model's own forecast band is contradictory across timeframes — 1H shows +90% blow-off to $69.8, 4H shows $79, but 1D forecasts $51.8 and 1W forecasts a further decline to $13.6 with the widest band. Combined with realized 1-day directional accuracy of 47% (below the 82% naive baseline), the short-horizon bullish forecast should be heavily discounted; the longer-horizon bearish read carries more weight. Key levels: support $35.77 (must hold), then air pocket to $30 psychological; resistance $40 (SMA20 area), $42–45 (prior consolidation), then $50.

Signal: two recent SeekingAlpha pieces are the most important — a downgrade citing that Q1 FY26 revenue -5.1%, margins are contracting, and execution risk is rising, plus a piece flagging that AI/data-center exposure is 'muddied by conflicts of interest.' These validate the price action and the margin math visible in the quarterlies. Also notable: EDF is divesting US/Canada power solutions to KKR — not the same entity, but a reminder that private capital is aggregating power-adjacent assets, which could eventually mean strategic interest in PSIX or, more likely, competitive pressure. Counter-signal/noise: two ChartMill pieces highlighting the value screen (P/E 8.7–9x, strong profitability) and an Insider Monkey mention that PSIX was among Aschenbrenner's Situational Awareness AI picks — flattering but backward-looking given the stake is $26M in a name that has since halved. Broader market news (Bitcoin, Iran) is not directly relevant.

- Stationary genset demand into data-center resiliency and microgrid — still the highest-multiple end market despite the AI narrative unwind, and the segment referenced in company disclosures

- Aftermarket and OEM service parts programs — higher-margin recurring revenue stream that should support gross margin recovery if scaled

- School bus / transit bus electrification components — a stable, policy-driven OEM revenue floor independent of AI capex cycles

- Q1 FY26 free cash flow turning positive to $17.2M — enables debt paydown (total debt $168M) and potential capital returns if sustained

- Aug 6 print is the near-term catalyst — any guidance reaffirming H2 revenue reacceleration would reset the narrative

- Aug 6 earnings is binary: a miss or soft guide likely breaks $35.77 support and opens $28–30

- Gross margin has compressed from 28.2% (Q2 25) to 22.9% (Q1 26) — if this is structural rather than cyclical, the entire value thesis fails

- 20.5% short float and thin 7.3M float amplifies moves in both directions; Beta 1.99 magnifies broader market risk-off

- 63% insider ownership with governance/conflict-of-interest concerns flagged in recent coverage caps institutional adoption and the achievable multiple

- AI/data-center power narrative has already unwound once (from $121 to $37) — further disappointment on this vertical could accelerate selling

- Forward EPS $3.32 vs. trailing $4.42 confirms consensus already expects earnings deterioration; positive surprise bar is asymmetric only if the setup is priced for disaster

- Model's short-horizon forecast (bullish to $69–79) is unreliable — 1D directional accuracy 47% vs. 82% naive baseline

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord