TMDX— AI Stock Forecast & Price Targets

Published 7/8/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live TMDX price forecast →

TMDX possesses superior underlying operational quality (45% ROE) and market-leading technology in organ preservation, but near-term investment is severely hampered by negative technical momentum, significant Q1 margin compression, and high debt levels. The stock remains a speculative play whose valuation hinges entirely on the binary outcome of the upcoming earnings report to confirm operational recovery.

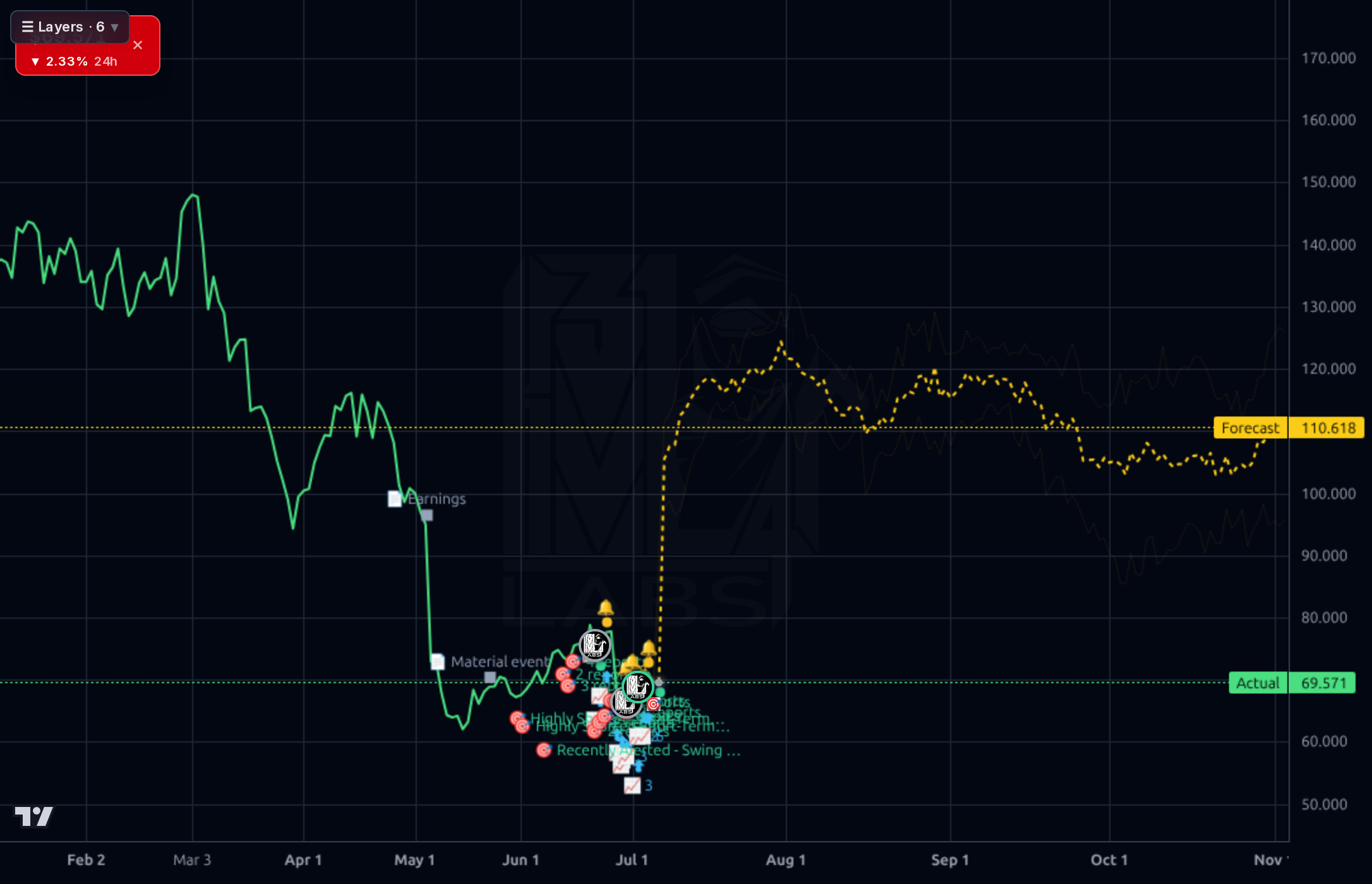

Wait for the July 30th earnings report. Do not size any swing trade into this event; treat the print as the primary catalyst and invalidation point. Key short-term support to watch is the $60-$70 zone, but a break below that signals deeper weakness.

The thesis hinges on Q2 operating margin recovery above historical averages (e.g., 13%+). If margins normalize and FCF turns strongly positive, the base case target of $85-$95 becomes more credible. A catalyst for upward movement is clear confirmation of OCS Heart DCD adoption scaling.

The long-term thesis remains strong due to its category-defining platform in organ preservation. The biggest structural risk is regulatory shifts in reimbursement/CMS policy, which could undermine the entire utilization model regardless of technological success.

The company exhibits strong underlying profitability metrics with a 45.22% Return on Equity and robust historical revenue growth (30.24% Y/Y TTM). However, the recent quarterly data shows concerning trends: Q1's operating margin compression to 7.6% and negative Free Cash Flow (-$12.1M) contrast sharply with prior quarters. The balance sheet carries a high debt load ($863M total debt vs $494M equity at end of Q1), which increases financial vulnerability despite strong current ratios (6.74). Capital allocation remains questionable given the debt structure and need for margin recovery.

Technically, the stock is in a deep downtrend, trading significantly below its 52-week high ($71.11 vs $156). The chart shows multiple instances of sharp declines punctuated by consolidation attempts near key support zones (historically around $60-$70). While the model's short-term forecast bands are unreliable given low directional accuracy, the current price action suggests a battle between technical selling pressure and underlying fundamental value. A confirmed break above recent resistance levels would be necessary to signal a trend reversal.

The news flow is overwhelmingly positive from analysts, with multiple firms reiterating 'Buy' ratings and maintaining high price targets ($120 target cited). This analyst sentiment highlights the core technology's strength. However, this bullish narrative must be weighed against the recent operational concerns (Q1 margin compression) and the insider sale noted on 6/24. The market is currently pricing in future recovery based on expert opinion rather than confirmed near-term execution.

- Expansion of OCS Heart DCD adoption to expand donor pool and drive high-margin heart preservation revenue.

- Scaling the national OCS Program logistics solution to build predictable, recurring service revenue streams.

- Persistence of Q1 operating margin compression suggests a structural issue beyond temporary capex spending.

- High debt load ($863M) combined with negative FCF creates significant financial vulnerability.

- Regulatory changes in reimbursement/CMS policy pose an existential threat to the core utilization model.

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord