TMDX— AI Stock Forecast & Price Targets

Published 7/6/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live TMDX price forecast →

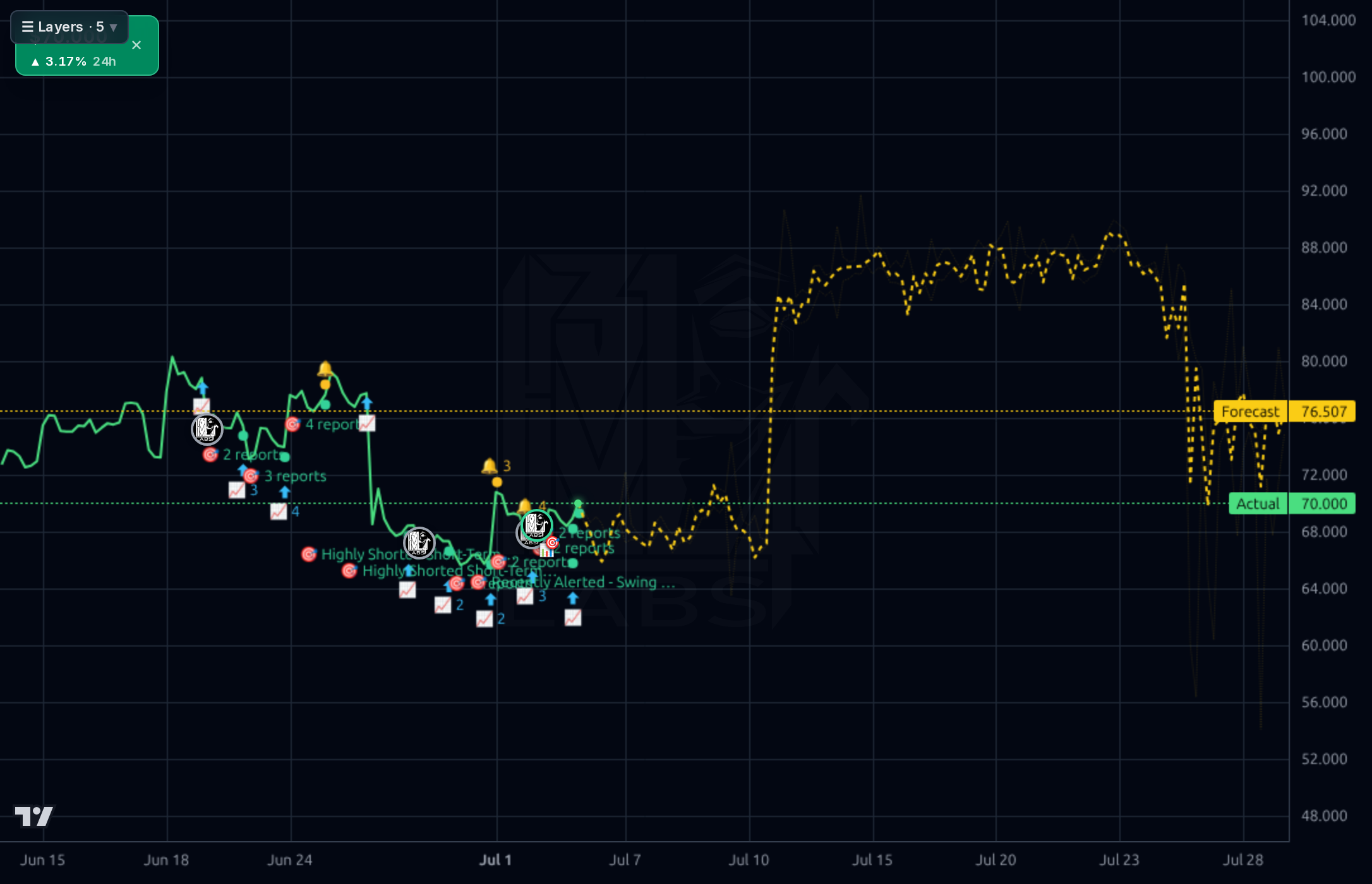

TMDX is a category-defining organ preservation platform trading at $68.86 after a brutal ~46% YTD drawdown, with strong underlying quality (45% ROE, 30% revenue growth, 59% gross margins) but a Q1 2026 margin collapse that halved operating margins and pushed FCF negative. The July 30 earnings print is the binary catalyst — the setup favors patience with a small starter position, since valuation (15.8x trailing, 20.3x fwd P/E) and 23% short interest create asymmetric potential if margins normalize, but downside remains real if Q1 was structural rather than transitory.

Hold or size a small starter (0.25-0.33 of intended position) into the July 30 earnings. Do NOT build a full position pre-print — earnings are a binary event with heavy IV crush risk and the stock has 23% short interest which can cut both ways violently. Key levels: $70 must reclaim to confirm a base, $60 is hard invalidation (breaking it signals structural earnings deterioration is being priced in). If price breaks $60 pre-earnings, step aside entirely. Realistic pre-earnings range: $63-75. The print itself is the catalyst — set alerts, don't trade the chop.

1-6 month base case: if July 30 shows operating margin recovering toward mid-teens and FCF turning positive, the short squeeze potential (23% SI, 5.7 short ratio) plus multiple re-rating could drive $85-95. If margins stay pinned at 7-10%, expect range-bound $60-75 as the market waits for another quarter of data. Bear case ($50-55) triggered by another sequential margin decline or debt-related surprise. Position for the upside outcome with defined risk — I'd size to survive the bear outcome. Change my mind: two consecutive quarters of sub-10% operating margins, or the $344M debt raise being tied to problem-solving (accounts receivable, inventory writedowns) rather than growth capex.

1-3 year thesis: TMDX is building the logistics backbone for organ transplantation with a real regulatory moat (only FDA-approved multi-organ normothermic perfusion platform), and DCD heart adoption plus international expansion are large TAM expansions. If operating margins normalize back to 20%+ and revenue compounds at 20-25%, the current $2.4B EV supports a 2-3x multi-year return. Biggest structural risk is reimbursement policy — CMS or private payer changes to OCS coverage economics would reset unit economics and could not be offset by volume alone. Secondary risk: competitive entry (Paragonix, XVIVO expanding scope) eroding the current oligopoly. This is a name to own through cycles if you believe in the platform, but sizing must respect the volatility.

Top-line remains strong: TTM revenue of $636M with 30.2% Y/Y growth and Q1 2026 revenue of $173.9M (+21% Q/Q vs a soft Q4). Gross margin held at 58.2% in Q1, but operating margin collapsed to 7.6% (vs 23.2% in Q2 2025 and 16.2% in Q3 2025) — a striking sequential deterioration. Net income of $7.3M in Q1 vs $34.9M in Q2 2025 confirms the profit compression is real, not a one-line-item anomaly. The balance sheet took a material hit: total debt jumped from $519M to $863M in a single quarter (+$344M), while cash rose only modestly to $462M, implying the raise funded capex/logistics build-out rather than sitting idle. Free cash flow flipped negative (-$12M) as capex spiked to $36.7M vs a $7-15M run rate the prior three quarters. Debt/Equity of 1.75 is elevated for a med-tech at this scale. That said, ROE of 45%, ROA of 15%, current ratio of 6.7, and 27% TTM net margin still mark this as a high-quality franchise — the question is whether Q1 marks a one-off investment cycle or a structural reset in unit economics.

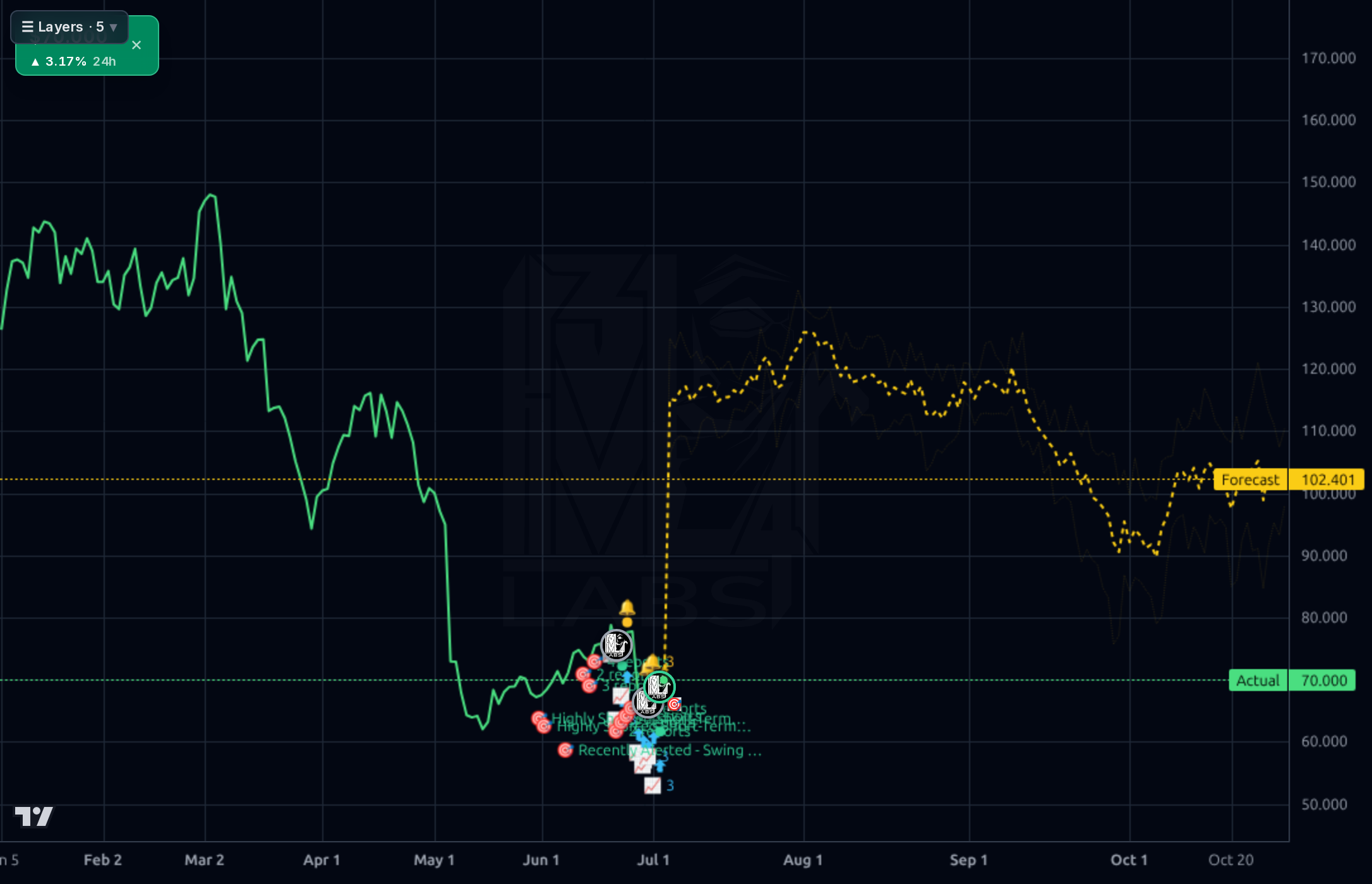

The multi-timeframe picture is decisively broken. The weekly chart shows a violent top formation from ~$175 down to the $60-70 zone — a >60% peak-to-trough decline. The daily chart shows price stabilizing in a $60-70 range since May but well below the declining 200-day (SMA200 -39.3%) and 50-day (SMA50 -10.5%). RSI of 42.6 is neutral-to-weak, not oversold. The 1h and 4h charts show a modest bounce off the $60 support, with price now at $68.86, just under key resistance at $70. The forecast model projects an aggressive rally to $86-90 on 1h/4h horizons, but the model's realized directional accuracy at longer horizons is essentially 0% vs a 100% naive baseline (MAPE 54-60% at 5-9d), so those upside projections should be heavily discounted. The daily forecast actually shows a range-bound $90-120 path — more credible but still likely optimistic given the calibration record. Key levels: $60 (52-week low, must hold), $70 (immediate psychological/technical pivot), $80 (SMA50 zone), $95 (gap-fill / prior support-turned-resistance).

News flow is mixed-to-constructive. TD Cowen reiterated Buy with a $120 target (implying ~74% upside), and Stifel raised its target from $75 to $80 while maintaining Hold — the sell-side is defending the story but not aggressively so. A Seeking Alpha piece explicitly frames the setup as the market over-reacting to Q1 margin pressure with the core growth thesis intact — a reasonable base-rate view for a name like this. A $722K insider sale after a 45% drop is a mild negative signal but is small in absolute dollars. ChartMill flagging TMDX as 'affordable growth' and Motley Fool's 10-year framing suggest the retail/quant crowd is starting to view this as a value-in-growth rebuild. Signal: consensus is that Q1 is a bump, not a break, but nobody is willing to underwrite that fully until the July 30 print. Noise: crypto/macro headlines are irrelevant to this specific setup.

- OCS Heart DCD adoption expansion — structurally increases the addressable donor pool for hearts, the highest-margin modality

- National OCS Program logistics build-out (aviation/ground) creating recurring service revenue — the $344M debt raise and $36.7M Q1 capex likely funding this

- International expansion opportunity flagged in company description, still early-stage in reported revenue

- Multi-organ platform leverage — same OCS backbone across heart, lung, liver reduces incremental R&D burden per modality

- Q2 2026 print (July 30) as the operational recovery catalyst — sell-side (TD Cowen $120 PT) is anticipating margin normalization

- Q1 2026 operating margin collapse to 7.6% from 23% in mid-2025 — if persistent, this is a structural thesis break, not a bump

- Debt jumped $344M in a single quarter to $863M with Debt/Equity of 1.75, and FCF turned negative — financial vulnerability if margins don't recover

- 23% short interest with 5.7 short ratio — can accelerate downside on a miss as much as fuel a squeeze on a beat

- Reimbursement policy risk on OCS utilization economics — a single CMS or major payer decision could reset the model

- Technicals remain deeply broken: -39% below SMA200, -46% YTD, no confirmed trend reversal — buying against the tape

- Forecast model's realized directional accuracy is worse than naive baseline at short horizons — heavily discount the aggressive upside projections in the forecast bands

- Insider selling ($722K) after a 45% decline is a mild negative confidence signal

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord