UPST— AI Stock Forecast & Price Targets

Published 7/8/2026 · A free sample of K3vl4r’s AI-powered analysis.

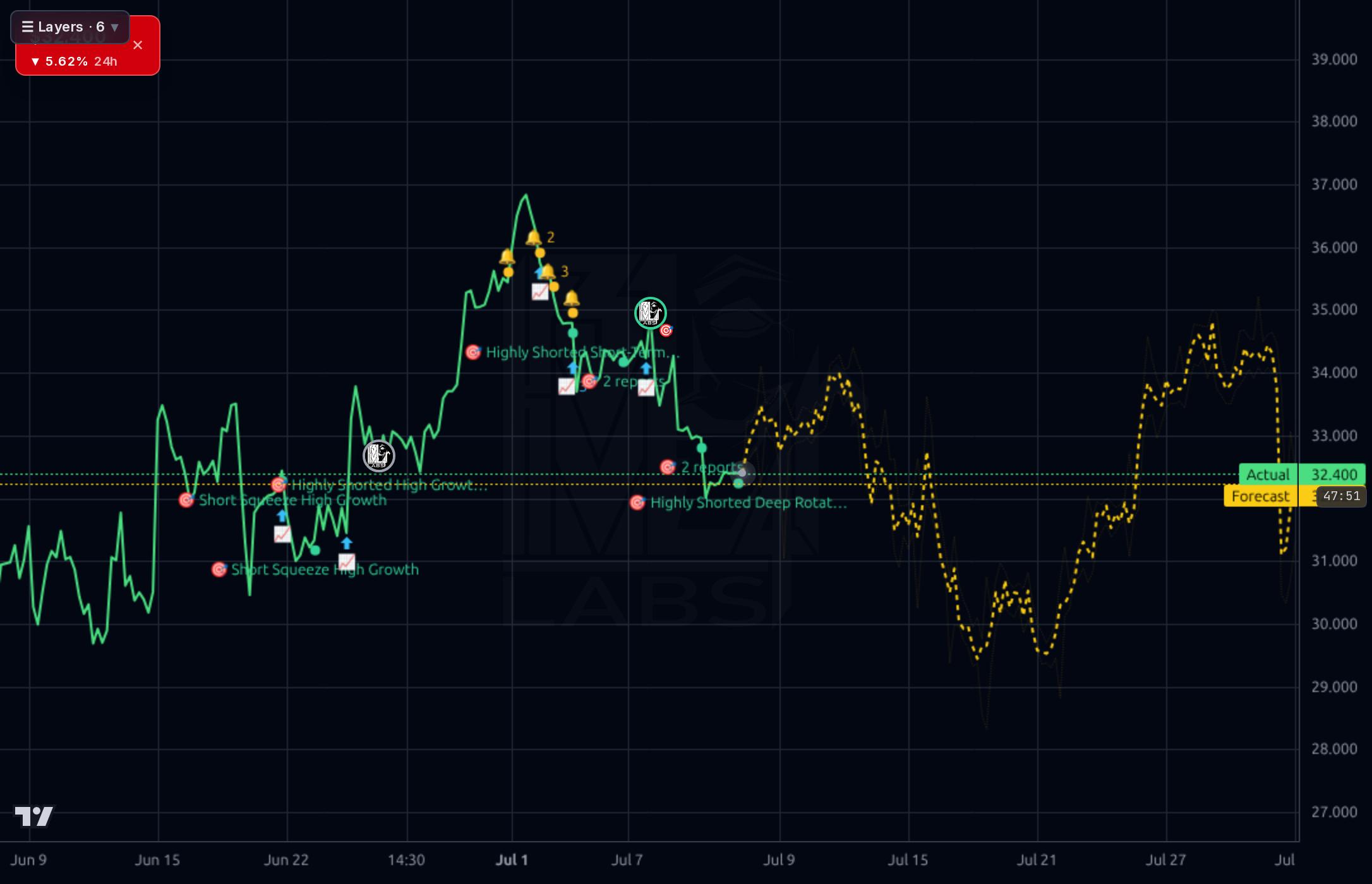

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live UPST price forecast →

UPST remains a high-beta play whose near-term trajectory is heavily dependent on institutional appetite for securitized loans and successful execution of its AI underwriting model. While recent analyst upgrades (Needham to $40, BTIG maintaining $43) provide bullish price anchors, the stock's valuation metrics (e.g., 9.97x Forward P/E) are stretched given volatile profitability and negative free cash flow. The immediate focus must be on the August 4th earnings report for confirmation of operational stability.

Wait for confirmation of sustained buying volume above recent resistance levels, ideally supported by a technical bounce off structural support near $31-$32. Size any entry cautiously, treating the August 4th earnings report as the primary catalyst/invalidation point; do not size into it.

The thesis hinges on successfully translating loan origination volume recovery into durable GAAP profitability and positive FCF post-earnings. If Q2 results show significant improvement in OCF and net income, a target range of $38-$42 (blending analyst targets with technical resistance) is plausible. A failure to meet these operational metrics invalidates the current bullish structure.

The long-term viability depends on successfully expanding Total Addressable Market via auto secured/HELOCs and maintaining AI underwriting superiority against competitors, while managing high debt levels through sustained capital market access.

The company operates in a high-growth but volatile sector (Credit Services). Revenue shows strong year-over-year momentum with Sales Y/Y TTM at 57.69%, and Q/Q sales growth of 44.45% suggests operational reacceleration. However, profitability is concerning: the trailing P/E of 83.73 is high, and Free Cash Flow remains negative (-$140M in Q2 2026). The balance sheet shows significant leverage (Debt/Eq of 2.70), which increases risk during a credit downturn.

The stock has shown strong recent momentum, breaking out above key technical levels as suggested by the 'Bullish Breakout' news headline and the chart pattern analysis. Support appears structurally important around the $31-$32 zone based on prior context. The model indicates high bullish probability (1.0) for the near term, but the 1-week forecast accuracy is low (33% vs 67% naive baseline), suggesting caution despite positive momentum signals.

The news flow is overwhelmingly positive from an analyst coverage standpoint, with Needham raising the price target to $40 and BTIG maintaining a Buy with a $43 target. Furthermore, reports highlight a 'Bullish Breakout' above downtrends and strong 30-day/90-day returns (15.43% / 29.79%). This positive sentiment is largely focused on the company's AI strength and renewed institutional funding capacity, which are key catalysts to watch.

- Securitization revival: The ability to reopen the ABS channel via agency ratings is critical for funding growth beyond internal balance sheet capacity.

- Product diversification: Expansion into auto secured loans and HELOCs broadens revenue streams beyond core unsecured personal lending.

- High Valuation Multiple: The current valuation implies significant future profitability that has not yet been sustained across full fiscal years.

- Credit Cycle Risk: Any deterioration in the credit environment, leading to higher delinquencies or wider ABS spreads, poses an immediate existential threat due to high leverage.

- Profitability Volatility: Historical data shows swings from profitable quarters to net losses, making earnings predictability low.

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord