UPST— AI Stock Forecast & Price Targets

Published 7/6/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live UPST price forecast →

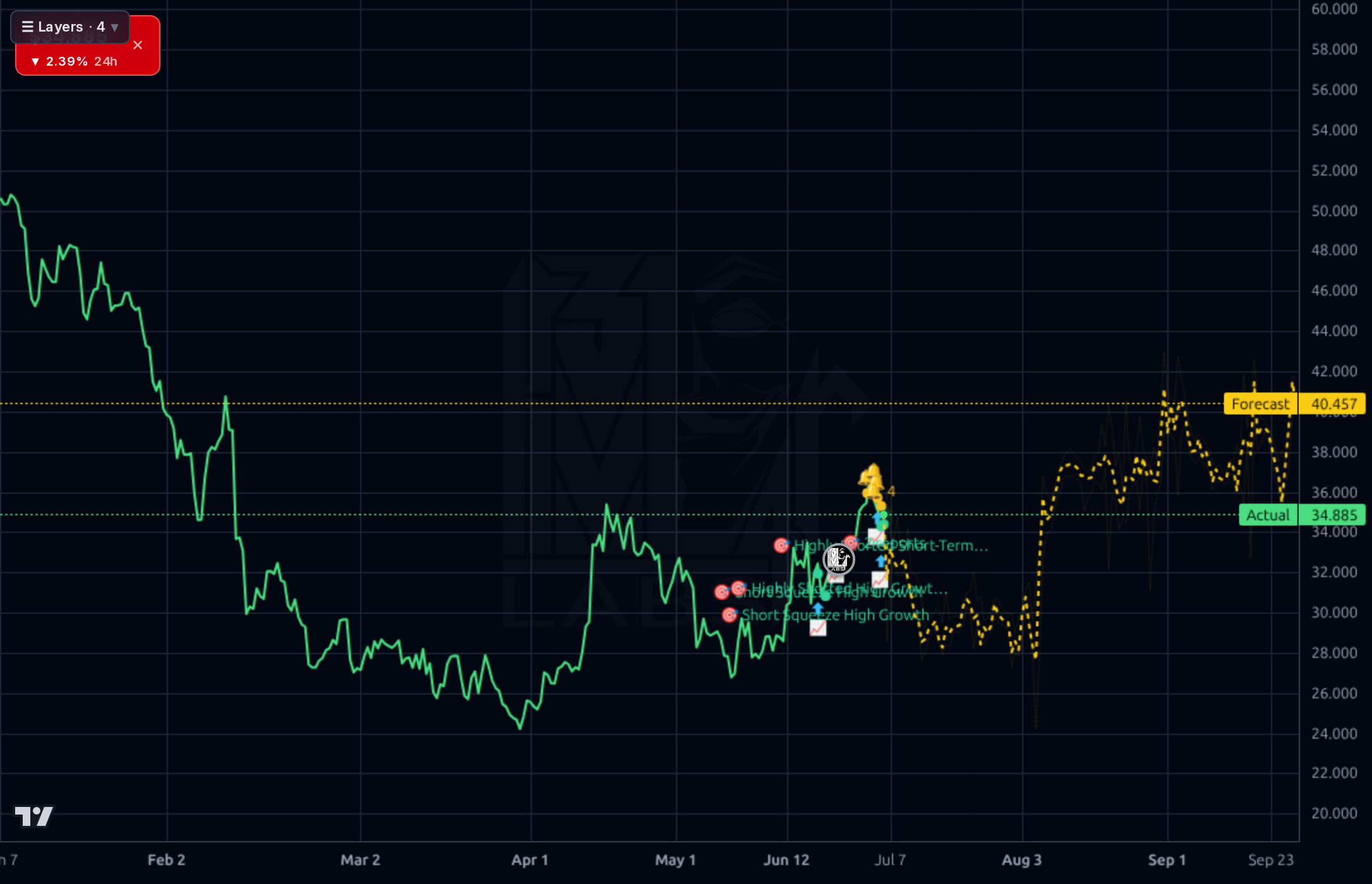

Upstart remains a high-beta bet on the credit cycle and institutional loan take-out capacity, with revenue reaccelerating (+44% Q/Q sales, +58% TTM Y/Y) but Q1 2026 swinging back to a $6.6M net loss and operating cash flow of -$133M. The shares have rallied ~37% this quarter into a valuation (90x trailing P/E, 19x forward, 3.8x EV/Sales) that already prices in a smooth recovery, and with 32.75% short float, a binary Aug 4 earnings print, and 1h/4h forecast bands drifting to $31-32, the risk/reward is balanced enough to warrant patience rather than fresh conviction.

HOLD into the Aug 4 earnings print (~29 days). Do not add here at $34.88 — the near-term forecast band actually drifts to $31-32, momentum is warm (RSI 59, +7.5% above SMA20, +37% QTD), and IV will compress into the print regardless of direction. For existing longs, consider trimming 20-30% into any push toward $37-38 resistance given the binary event risk. Invalidation of the recovery thesis: a decisive break below $31 on volume, which would signal the short squeeze has exhausted. Do not size a directional swing trade through earnings; if you must play the print, use defined-risk options with sizing appropriate for a name that has historically gapped 15-25% on results.

1-6 month view is HOLD/ACCUMULATE ON WEAKNESS. The bull case requires two consecutive profitable quarters and OCF turning positive again post-Q1's -$133M swing; if delivered, forward P/E of 19x on rising estimates (next-year EPS growth revised to +81.7%) is defensible and shares could work to $40-45. The bear case is that Q1's loss was the leading edge of a cycle re-rollover — funding partners tighten, originations plateau, and multiple compresses to 12-15x forward on lowered estimates, taking shares to $27-28. Expected return range: -20% to +25%. What changes my mind bullishly: Q2 print showing OCF turning positive AND a new named forward-flow partner. Bearishly: any hint of delinquency deterioration in the Q2 credit metrics, or an ABS deal getting pulled/priced wide.

1-3 year terminal thesis rests on whether Upstart's AI underwriting genuinely delivers structural loss-rate advantages across a full credit cycle — something that has not been proven through the 2022-2023 rate shock. If yes, the business can scale into an asset-light originations platform with 20%+ operating margins and $2-3B revenue, justifying a much higher price. If no, it becomes a subscale specialty lender with cyclical earnings and permanent multiple discount. Biggest structural risk: the model itself is a black box to loan buyers, and any credit event that surprises institutional partners could permanently impair take-out demand and force balance-sheet warehousing — which the company is not capitalized to sustain at scale given $1.98B debt and negative TTM FCF.

Top-line trajectory is the clear positive: Q1 2026 revenue of $308M is up sequentially from $276M (Q4) and $257M (Q2 2025), and TTM sales growth is +57.7% Y/Y with gross margins near 83%. However, profitability is not sticking — after three profitable quarters ($5.6M, $31.8M, $18.6M), Q1 2026 flipped to a -$6.6M net loss with operating margin of just 0.9% and EPS Q/Q -163.85%. Cash generation is worse: OCF was -$133M in Q1 versus +$109M in Q4, and TTM free cash flow is -$312M, meaning the business is still consuming capital to fund the origination rebound. The balance sheet reflects this: total debt of $1.98B against $475M cash and equity of $733M drives a D/E of 2.7x, though the current ratio (11.6) and quick ratio (4.0) show near-term liquidity is intact. ROE of 7% and ROA of 1.8% are thin for the multiple assigned. Fundamentally this is a business whose economics depend entirely on the reopening of forward-flow and ABS channels — recent Neuberger renewal ($600M capacity) and KBRA ratings on the 2026-3 trust are exactly the right signals, but they have not yet converted to durable GAAP profit or positive FCF.

Across timeframes the stock is in a rebound off cycle lows. On the 1d chart price has climbed off the $24 April low through $28-30 to the current $34.88, closing decisively above the 50-day (SMA50 +10.9%) but still -10.3% below the 200-day, so the primary trend is not yet confirmed as bullish. Weekly perspective shows this is still a deeply broken chart — 52-week high $87.30 (-60%), 5Y perf -71% — with $34-36 representing the middle of a multi-quarter range. RSI 59.3 is warm but not stretched, and Perf Quarter of +37% signals momentum. The AI forecast is mixed: the 1h and 4h bands drift DOWN toward $31.99 and $28-32 over the coming days/weeks (near-term bullish prob only 0.40 on 1wk despite headline 1.00 bullish prob), while the daily forecast points to $39.91 and the weekly to an unrealistic $84 — I discount the long-dated forecast heavily given the model's degrading MAPE at longer horizons (15% at H8, 27% at H9). Support sits at $31-32 (prior consolidation and forecast anchor), then $28. Resistance is $37 (recent local high visible on the 1h chart) then $40. The 32.75% short float creates upside gap risk, but also means any earnings miss unwinds fast.

The signal in recent news is capital-markets access, not operating results: the renewed Neuberger Specialty Finance forward-flow agreement (up to $600M) and preliminary KBRA ratings on Upstart Securitization Trust 2026-3 both confirm that institutional take-out capacity is being rebuilt — historically the most reliable positive catalyst for this name. Sell-side coverage is mixed, with Jefferies raising its target to $30 (still below spot) while maintaining Hold, and Zacks/SeekingAlpha framing the story as a 'promising recovery' with 'lumpy' Q2 risk. EPS estimate revisions have moved higher (next-year EPS growth revised from 45.4% → 60.8% → 81.7%), which supports the forward multiple compression thesis if delivered. The noise to filter: daily price-move headlines and broader crypto/geopolitical items are context only. Net-net, news supports the recovery narrative but does nothing to derisk the Aug 4 print.

- Renewed Neuberger Specialty Finance forward-flow agreement providing up to $600M of committed personal loan take-out capacity

- Reopened ABS channel via KBRA preliminary ratings on Upstart Securitization Trust 2026-3, restoring securitization as a funding lever

- Next-year EPS estimate revised up materially (+20.9pp to 81.7% growth) reflecting analyst confidence in operating leverage

- Product expansion beyond unsecured personal loans into auto secured personal loans and HELOCs broadening TAM

- Revenue reacceleration to $308M in Q1 2026, +44.5% Y/Y, indicating originations volume recovery from rate-shock trough

- Aug 4 earnings is a binary catalyst — Q1 already flipped back to net loss and OCF of -$133M, so a second consecutive miss would break the recovery narrative

- Valuation of 90x trailing P/E, 19x forward, 3.8x EV/Sales prices in operating leverage that has not been demonstrated across a full year

- Balance sheet leverage of 2.7x D/E ($1.98B debt vs $733M equity) leaves minimal cushion if loan sales slow

- TTM free cash flow of -$312M means the business is capital-markets dependent; any funding freeze is existential

- 32.75% short float and beta of 2.27 mean both upside and downside moves overshoot fundamentals — dangerous for undisciplined sizing

- Credit cycle risk: delinquency deterioration or a widening ABS spread environment would immediately compress take-out demand from institutional buyers

- Model's own weekly/monthly forecasts have degrading MAPE (15-27% at longer horizons) and should not anchor position sizing

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord