VNT— AI Stock Forecast & Price Targets

Published 7/6/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live VNT price forecast →

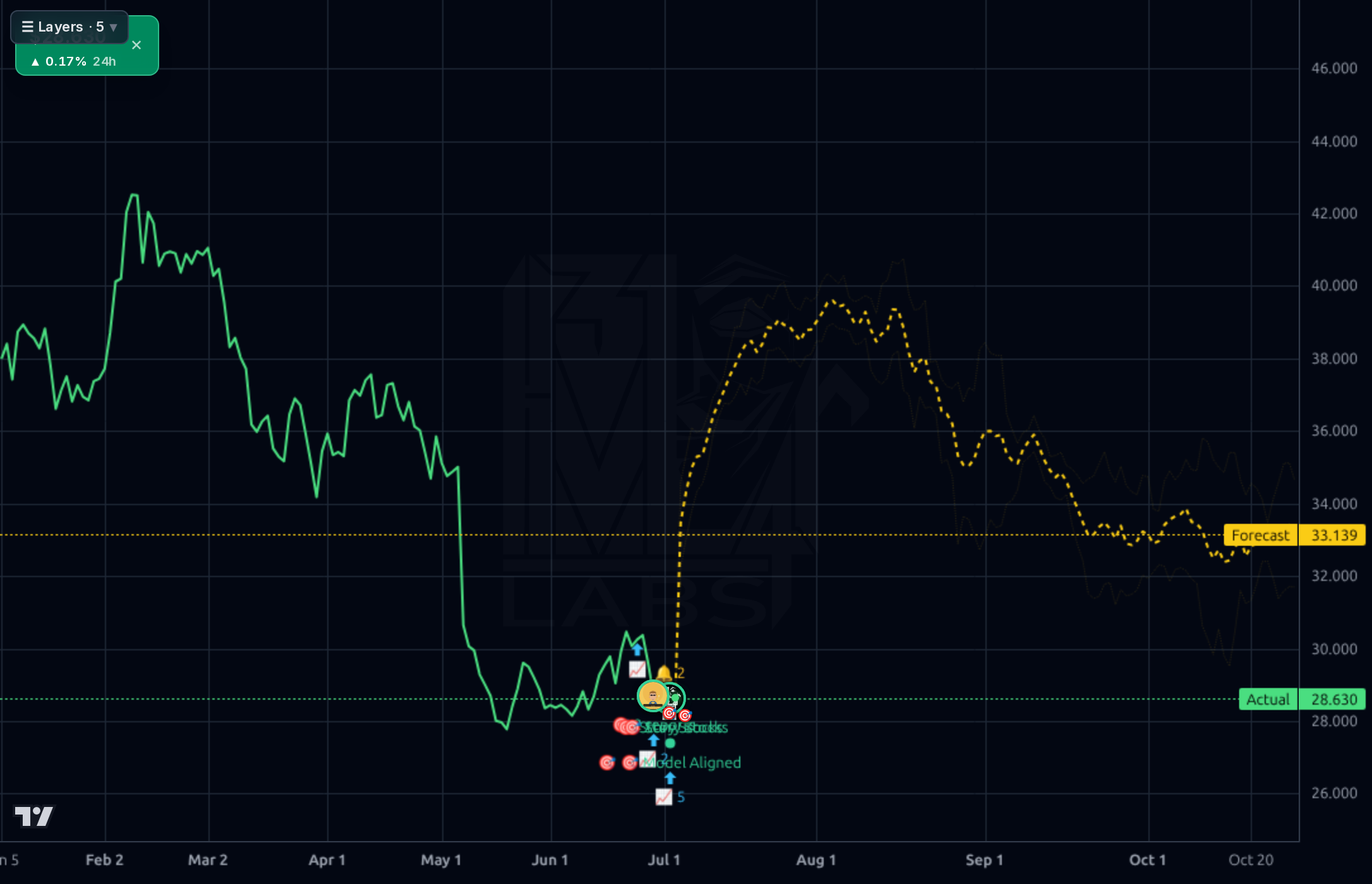

Vontier trades at a distressed 7.7x forward P/E and 0.87 PEG with strong underlying metrics (47% gross margin, 35% ROE, $291M TTM FCF), but the stock is pinned near 52-week lows ahead of a binary July 30 earnings print that must confirm Q1's FCF collapse ($24.8M vs $174.8M in Q4) was transient. Technicals remain broken (-21.6% below 200-SMA, -23% YTD, RSI 41) and the forecast model's directional accuracy is actively worse than naive baseline, so despite cheap valuation this remains a show-me name — accumulate cautiously, sized small into the print.

Into the July 30 earnings print (~24 days out), stay small or flat. This is a binary event with FCF normalization as the key question; do not size a swing trade into it. If entering, keep position size to 1/3 of a normal allocation with a hard stop below the $27.25 52-week low (invalidation of the value floor). Expect IV crush post-print; do not chase options. Any pre-earnings rally into $30-31 resistance is a place to trim, not add. Explicit earnings stance: neutral-to-cautiously-constructive, but not sized for the outcome.

1-6 month base case is a range trade between $27 and $33 unless earnings decisively resolves the FCF question. If Q2 prints operating cash flow >$120M and management guides constructively, expect a re-rate toward $33-35 (bridging analyst target $39.44 as an aspiration). If FCF disappoints again or working capital drag persists, $25-26 becomes the next support and the thesis breaks. Expected return range: -12% to +18%. Catalysts: earnings print, Driivz contract announcements, any Matco stabilization commentary. What would change my mind: two consecutive quarters of sub-$75M FCF or D/E creeping higher.

1-3 year terminal thesis rests on Driivz reaching sufficient scale to offset legacy fueling secular decline, combined with Repair Solutions stabilization. If successful, the business should sustain low-single-digit revenue growth with ~18% operating margins and $350M+ FCF, supporting a 12-14x P/FCF multiple = $38-45 range. Biggest structural risk is that the EV charging software market commoditizes before Driivz achieves scale, leaving Vontier stuck with a declining fueling business and $1.9B of debt. Secondary risk is that a debt refinancing at higher rates compresses FCF further.

Vontier's TTM profile is genuinely attractive on paper: $3.09B revenue, 47.2% gross margin, 18.0% operating margin, 13.4% net margin, 35% ROE, 14.3% ROIC, and $291M free cash flow supporting a 10.8x P/FCF. But the quarterly cadence reveals the problem — Q1 2026 revenue of $750.6M was down sequentially from $808.5M in Q4 2025, operating income fell to $134.8M from $152.7M, and most importantly Q1 operating cash flow collapsed to $46.5M with FCF of only $24.8M vs $174.8M the prior quarter. Cash on the balance sheet dropped from $492M to $234M in a single quarter while total debt only fell modestly to $1.94B, keeping D/E at 1.53 and leaving the company with a $1.7B net debt burden against $695M TTM EBITDA (2.5x net leverage — manageable but not comfortable). Sales growth is anemic at 1.3% Q/Q and 4.1% Y/Y TTM, and 3/5-year sales growth of -1.15%/2.60% confirms this is a slow-growth compounder, not a growth story. Capital allocation via buybacks is being deployed into a falling tape. The core question is whether Q1's working capital consumption was one-time; if the July 30 print shows normalized FCF near $100M+, the value case is intact.

The technical picture across timeframes is unambiguously negative. On the weekly chart, VNT peaked near $45 and has broken down through multi-year support, now trading at $28.63 with the 200-SMA sitting 21.6% overhead — a classic distribution pattern. The daily chart shows the stock rolling over from the mid-$30s into a lower-highs/lower-lows structure with the 52-week low at $27.25 acting as the only proximate support (roughly 4% below spot). RSI at 41 is weak but not oversold, meaning there's no reflexive bounce set-up yet. Short float has climbed to 7.66% (short ratio 6.03) indicating meaningful bearish positioning. The Kronos forecast band on the 1h/4h charts shows a bullish reversion trajectory toward the mid-$30s, but this must be heavily discounted: the model's realized 1d directional accuracy is 41% vs a 62% naive baseline, and 1wk accuracy is 0% vs 100% naive — the model is actively unreliable in this regime. Longer-dated 1wk and 1d chart forecasts point to $35+ but past calls at similar levels have not printed. Key levels: $27.25 (52-week low, must hold), $30 (psychological/near-term resistance), $32-33 (50-SMA zone), $35.50 (Kronos long-term forecast/resistance).

Signal: the Iberdrola/bp pulse partnership for Driivz to manage 2,500 fast/ultra-fast chargers across Spain and Portugal is a genuine validation of the EV-charging software platform and the kind of anchor deal needed to prove Driivz can scale into a real offset to legacy fueling decline. Cameron Richardson joining as Group President of Repair Solutions leading Matco Tools is a concrete operational lever — Matco has been a persistent underperformer and new leadership could unlock the segment. Third consecutive year on TIME's World's Most Sustainable Companies list is nice-to-have for ESG mandates but immaterial to price action. Noise/negative: the StockStory piece flagging '3 Reasons VNT is Risky' echoes the market's current show-me stance and reinforces the technical narrative rather than adding new information. Consumer/roadside retail survey coverage is marketing-adjacent. Broader crypto/geopolitical headlines are unrelated. Net: recent news is modestly constructive on fundamentals (Driivz traction, Matco leadership) but does nothing to alter the near-term technical setup — the July 30 print is the only catalyst that matters.

- Driivz Iberdrola/bp pulse partnership managing 2,500 fast/ultra-fast chargers across Spain and Portugal — anchor customer that validates enterprise EV charging software platform

- Cameron Richardson appointment as Group President of Repair Solutions leading Matco Tools — operational reset in the underperforming segment

- Q2 2026 earnings (July 30) as the primary near-term catalyst to demonstrate FCF normalization from Q1's $24.8M trough back toward the $100M+ quarterly run-rate

- Forward EPS of $3.70 vs trailing $2.83 implies ~31% earnings growth embedded in consensus, providing multiple expansion optionality if delivered

- Buyback capacity from $291M TTM FCF at current $4.03B market cap represents ~7% annual repurchase yield potential if capital allocation shifts aggressively

- Q1 2026 FCF collapse to $24.8M (vs $174.8M Q4) — if this persists in Q2 print, the entire cash-generative thesis breaks

- Total debt of $1.94B with D/E of 1.53 and net leverage ~2.5x EBITDA leaves limited buffer for a rate shock or continued working capital drag

- Technical structure is severely damaged: -21.6% below 200-SMA, -23% YTD, short float 7.66%, no reflexive oversold signal yet

- Forecast model directional accuracy (41% 1d, 0% 1wk) is worse than naive baseline — the visible bullish forecast band should NOT drive positioning

- Legacy fueling business faces secular decline while Driivz has not yet reached sufficient scale to offset — the transition risk window is 2-3 years

- Anemic 1.3% Q/Q sales growth and -1.15% 3-year sales CAGR make it hard to argue this is anything more than a low-growth compounder deserving a value multiple

- Analyst target of $39.44 (+38% upside) may prove aspirational — prior calls with similar bull targets have not printed

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord