YMM— AI Stock Forecast & Price Targets

Published 7/6/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live YMM price forecast →

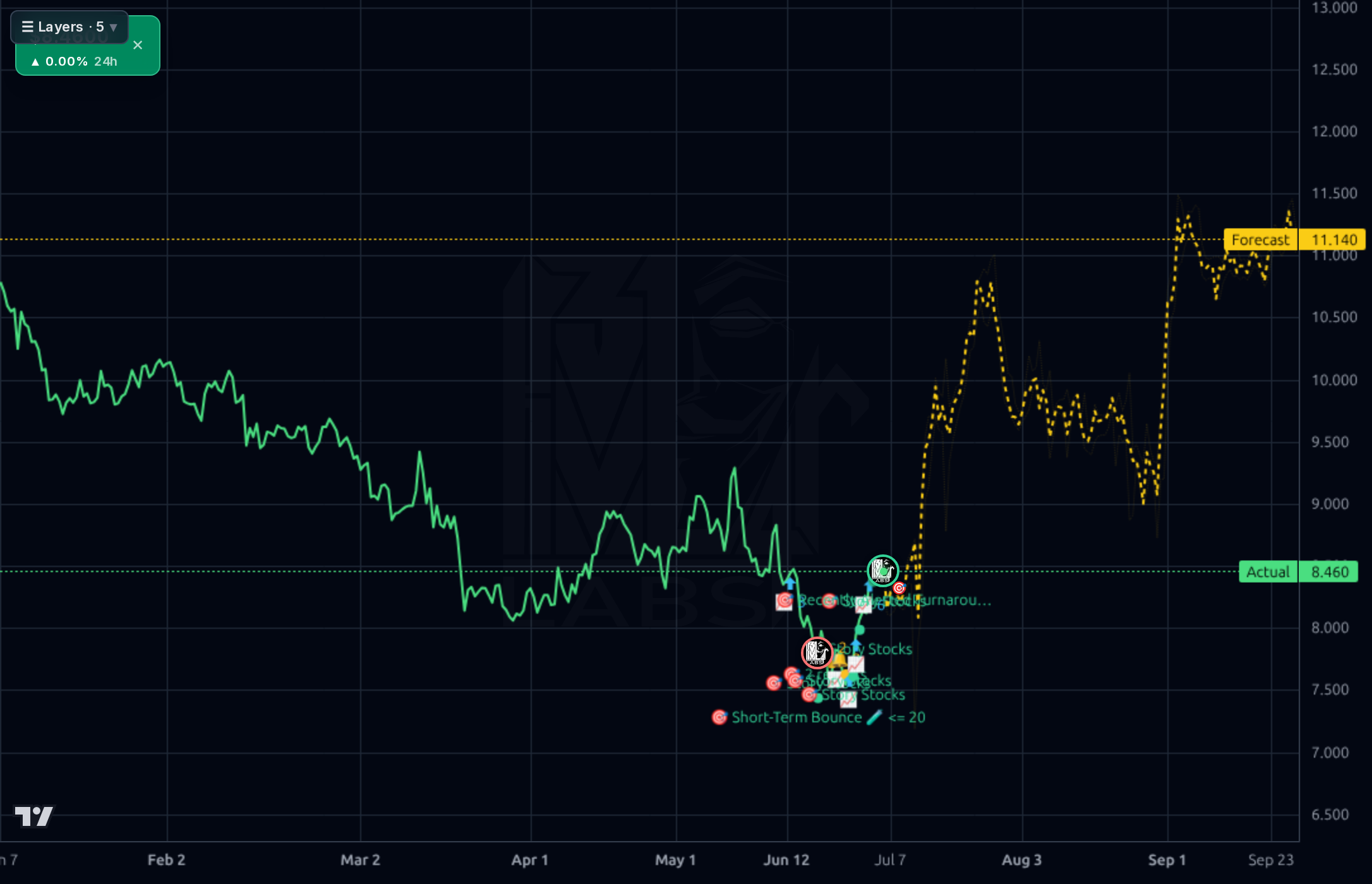

Full Truck Alliance is a cash-rich, high-margin Chinese digital freight platform trading at a compressed forward P/E of ~9.9x and PEG of 0.70 despite JPMorgan's recent upgrade to Overweight with a $10 target. The stock has stabilized near 52-week lows around $8.43 after a -30% year and -21% YTD drawdown, with fundamentals (32.7% net margin, 6.93 current ratio, ~$18.5B cash) materially outrunning price action. We remain constructive but temper prior optimistic base targets given the model's persistent overshoot and the August 20 earnings binary.

1-4 week view: With price consolidating in $8.00-8.60 and the Aug 20 earnings ~45 days out, treat this as a pre-earnings positioning window, not a swing trade into the print. A tactical add zone is $8.00-8.20 with invalidation on a daily close below $7.45 (52-week low). Above $8.60 the path opens to $9.20 (JPM target proximity) then the 200-day near $10.20. Do not add size into earnings; the July 7 ex-dividend is a minor step. Keep starter/half positions.

1-6 month view: The base case is that Q2/Q3 continue the pattern of 30%+ net margins and mid-single-digit to low-double-digit revenue growth, allowing the multiple to re-rate modestly from forward P/E ~10 toward 12-13x, targeting $9.50-10.50. Key catalysts: Aug 20 earnings, any capital return announcement given the CN¥18.5B cash hoard, and PBOC/China stimulus flow-through to freight volumes. What changes the mind: a revenue deceleration below +3% YoY, regulatory action on digital freight platforms, or a broken $7.45 low.

1-3 year view: The terminal thesis is that YMM becomes the dominant digital layer in Chinese road freight, expanding take rates via value-added services (credit, insurance, ETC, energy) that lift group margins above 35% and drive 15-20% EPS CAGR. A bull outcome (12-13x on ~$1.20 EPS) gets to the low-teens, roughly aligned with the $12-13 zone. The biggest structural risk is Chinese regulatory intervention — either explicit platform rules or capital-controls friction on ADR-listed Chinese names — which can compress the multiple regardless of operating results.

The fundamentals are the strongest part of the story. TTM revenue is CN¥12.64B with net income CN¥4.13B, implying a 32.7% net margin and 35.3% operating margin — Q1 2026 came in at CN¥2.85B revenue (+5.5% YoY per the May press release) with net income of CN¥991M (34.8% margin), continuing a multi-quarter cadence of ~30%+ bottom-line margins. The balance sheet is fortress-like: CN¥18.5B total cash versus only CN¥25.7M total debt, a current ratio of 6.93, and stockholders' equity of CN¥39.9B against total assets of CN¥44.8B. Operating cash flow of CN¥1.56B in Q1 2026 alone (vs CN¥326M in Q1 2025) is a notable step-change in cash generation. ROE of 10.5% is modest given the huge cash pile, which is the main capital-allocation critique — the dividend yield of ~2.0% and Jul 7 ex-date help, but a buyback or larger distribution is warranted. Forward P/E of 9.9 and PEG of 0.70 look inexpensive against consensus EPS growth of ~20% next year.

Across the 1h, 4h, and daily charts price is basing between roughly $7.45 (52-week low) and $8.60 after a sharp Q2 slide from the ~$11 area. The daily chart shows a lower-high structure since March with the 200-day SMA -17.3% overhead, but RSI at 53 and price +3.3% above the 20-day and only -1.0% below the 50-day suggest the downtrend is losing energy and a base is forming. The Kronos forecast is bullish across all four timeframes (1d forecast 9.18, 4h 11.14, 1d 10.10, 1wk 11.00), but realized directional accuracy is only ~54% on the 1d (vs 52% naive) and roughly matches the naive baseline on 1wk — the model has historically been optimistic on this name (MAPE ~21% on 1d, prior base targets have consistently sat ~16% above realized price). Immediate support $8.00 then $7.45; resistance at $8.60, then the June breakdown zone $9.20-9.50, then the 200-day near $10.20. Volume-weighted, the +11.8% weekly performance is encouraging but not yet a confirmed trend change.

The signal-heavy items are the June 29 JPMorgan upgrade to Overweight with the price target raised from $8.60 to $10 (Karen Li flagging the 28% YTD selloff as having 'priced in' bear cases), the May 28 Zacks upgrade to Buy, and the May 21 Q1 2026 print showing +5.5% YoY revenue to CN¥2.85B and net income of CN¥994M — all pointing to durable earnings power. Simply Wall St's May 23 valuation note and Insider Monkey's inclusion of YMM in 'fastest growing Asian stocks' add background validation but are largely secondary. The broader market news (bitcoin drawdown, Iran headlines) is not directly relevant. The next binary catalyst is the August 20 Q2 print, which will confirm or break the sequential margin/growth cadence.

- Q1 2026 operating cash flow of CN¥1.56B (nearly 5x the CN¥326M in Q1 2025) — a step-change in cash generation that supports capital return or reinvestment

- Expansion of value-added services (credit solutions, insurance brokerage, ETC, Intelligent Driving, energy services) beyond core freight matching — the margin uplift lever

- JPMorgan upgrade to Overweight with target raised to $10 (from $8.60) on June 29 signaling sell-side re-engagement after the 28% YTD selloff

- Consensus EPS next year growth of +20.4% with forward P/E ~9.9x offers a re-rating path if execution holds

- Potential capital return: CN¥18.5B cash versus CN¥25.7M debt leaves ample room for buybacks or an enhanced dividend beyond the current ~2% yield

- August 20 earnings is a binary event that can gap the stock; a revenue miss or margin compression versus the 30%+ cadence would break the thesis

- Chinese regulatory risk on digital platforms and ADR structures remains an idiosyncratic overhang not reflected in the fundamental multiple

- Price still -17% below the 200-day SMA and -40% from 52-week high — technical downtrend is not confirmed broken

- The forecast model has been persistently optimistic on this name (prior base targets averaging ~16% above realized price; 1d MAPE 21%) — discount upside from AI targets

- Cyclical exposure to Chinese domestic freight volumes; a further consumer/industrial slowdown pressures both revenue and take-rate expansion

- Institutional ownership at 73% with -4.6% recent institutional transactions signals distribution pressure that can cap rallies

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord