ADBE— AI Stock Forecast & Price Targets

Published 7/1/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live ADBE price forecast →

Adobe is a high-quality compounder (89% gross margin, 63% ROE, $9.2B FCF) trading at just 7.4x forward EPS after a brutal ~48% drawdown from its 52-week high on AI-disruption fears. The setup is a deep-value contrarian opportunity with insider/institutional support and a $25B buyback, but the tape is broken (price below SMA20/50/200, RSI 39) and the AI forecast model has underperformed a naive baseline recently, so we accumulate patiently rather than chase.

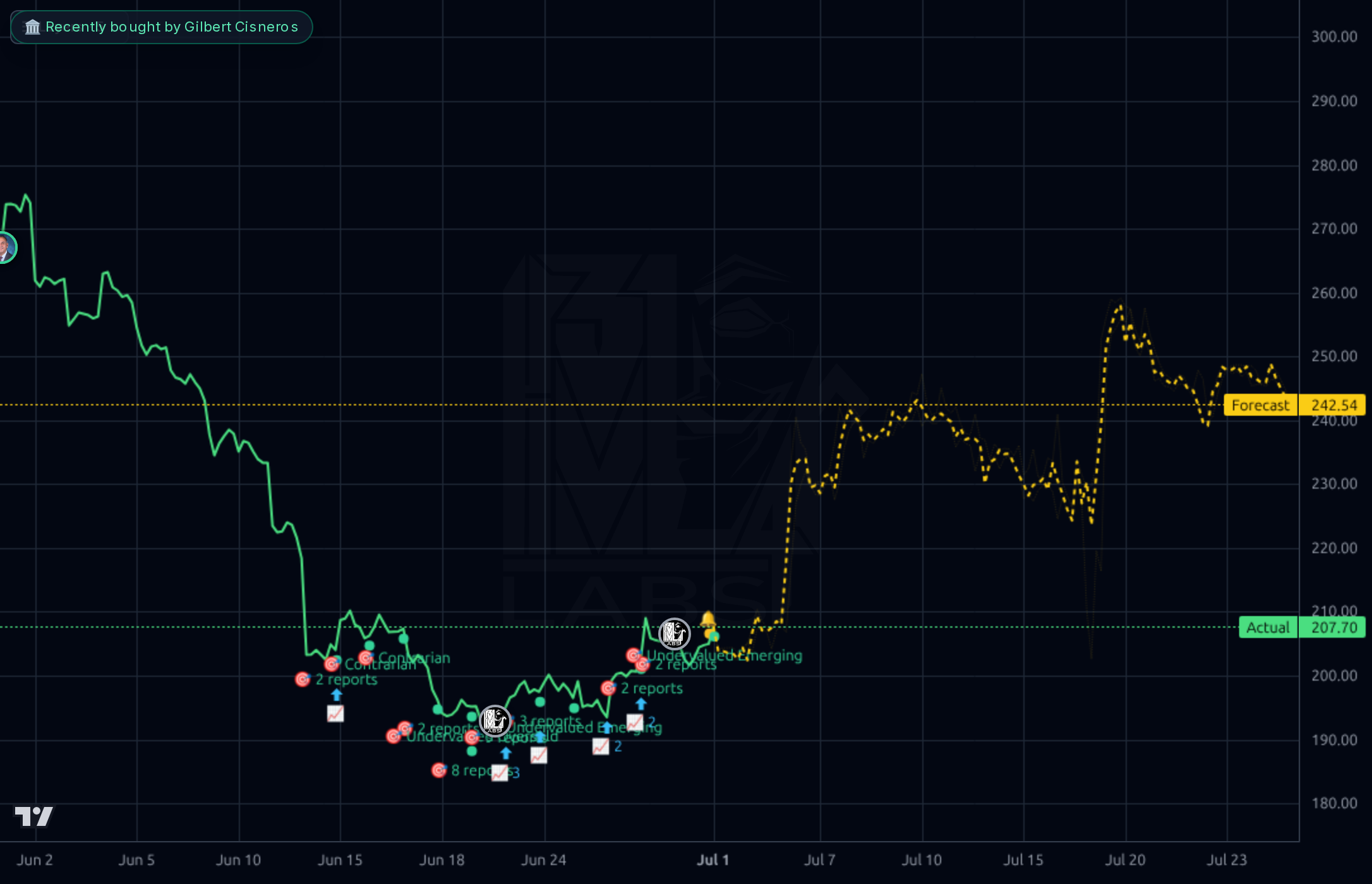

1-4 weeks: accumulate in tranches into weakness, don't chase. Preferred entries $195–$205; add on any retest of $190 (52w low). Invalidation is a weekly close below $185 on volume — that opens $170. Above, need a daily close over $215 to confirm the base, and $230 to trigger a real trend-change trade. Position size small-to-medium given the tape damage; earnings are 71 days out, so no immediate binary catalyst. Do not size to the AI forecast — its daily directional accuracy is below the naive baseline.

1-6 months: base case is a grind back toward $235–$250 as Firefly Foundry / AI ARR datapoints show up in the Sept 10 print and the buyback ($25B authorization) provides a floor. Expected return range +15% to +25% from spot. Catalysts: Sept 10 earnings (AI ARR disclosure, DME/DX segment growth, margin resilience), further Foundry customer wins, any activist/board news. Thesis breaks if: revenue growth decelerates below 8%, operating margin compresses under 33%, or AI ARR growth slows materially — any of those and this becomes a value trap, not deep value.

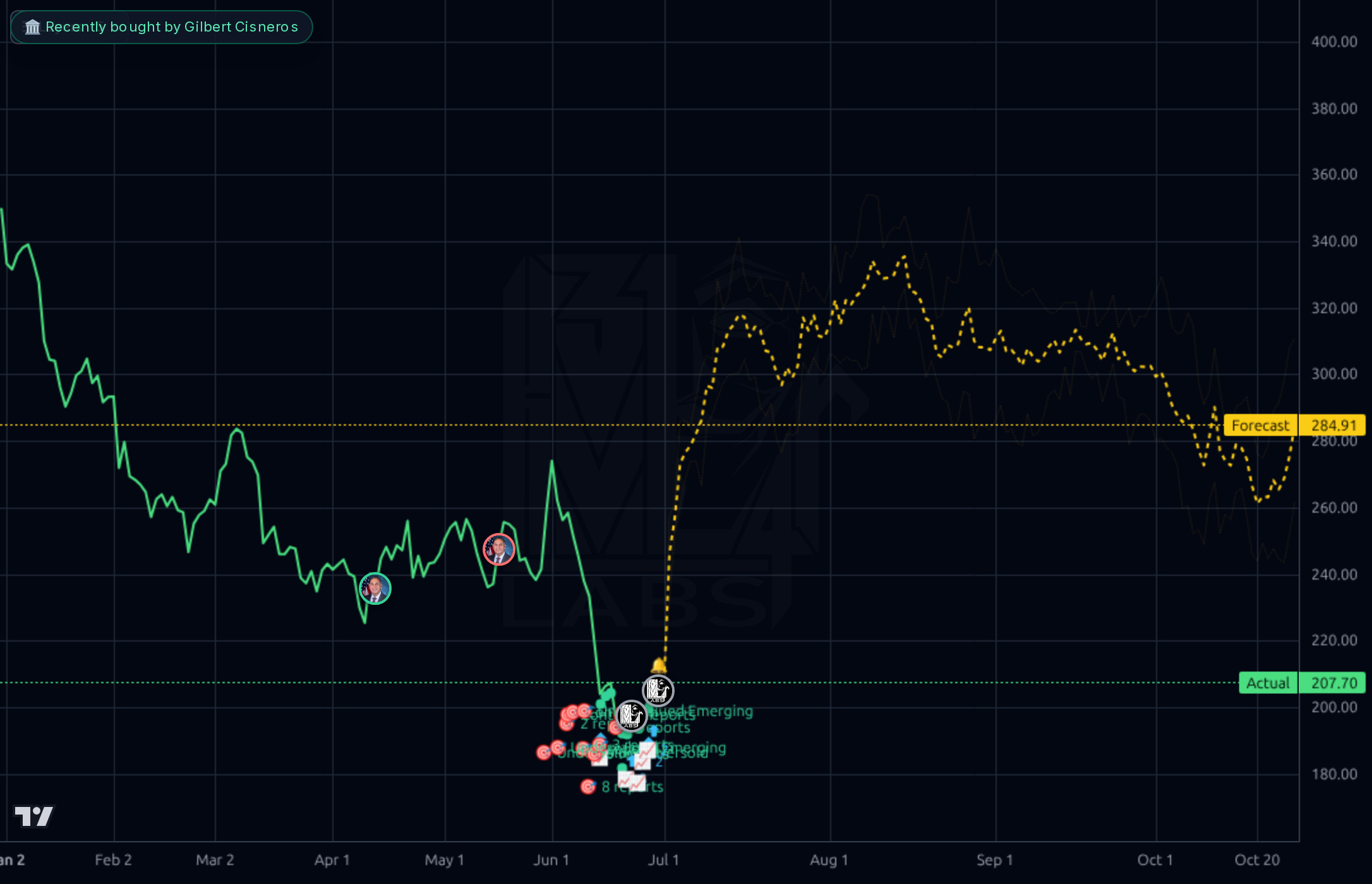

1-3 years: if Adobe successfully repositions Creative Cloud + Experience Cloud as the enterprise AI-content workflow layer, EPS can compound to $35–$40 by FY28 and even a modest re-rating to 12–14x forward earnings gets you to $420–$500. The FCF machine ($9B+ annually) plus the buyback shrinks share count meaningfully at these prices. The biggest structural risk is that generative AI commoditizes creative software faster than Adobe can migrate its economic model — if consumers/SMBs churn to native model providers (OpenAI, Google, Midjourney) and enterprise Foundry adoption disappoints, revenue growth falls into the mid-single digits and the multiple stays at 7–9x forever.

The financials remain excellent in absolute terms and disconnected from the tape. Q2 FY26 (May-26) printed $6.62B revenue (+10.5% YoY implied from the trailing quarters running $5.99B → $6.19B → $6.40B → $6.62B), 33.8% operating margin, 89.2% gross margin and $2.11B FCF on just $58M capex — an ~$8.4B annualized FCF run-rate that squares with the $9.22B TTM FCF. TTM revenue is $25.2B (+11.5% YoY), net margin 28.7%, ROE 63%, ROIC 43% — these are elite software economics. The balance sheet is fine but not pristine: $4.9B cash vs $7.07B debt (net debt ~$2.1B), current ratio 0.75, working capital -$3.0B, debt/equity 0.61 — the softness is largely a function of aggressive buybacks compressing equity and consuming cash. At 11.7x trailing, 7.4x forward EPS, 7.9x P/FCF, 8.3x EV/EBITDA, 0.51 PEG, ADBE trades like a melting ice cube, but there is no evidence of that in the segment numbers yet — AI ARR reportedly +200% YoY and the recent Firefly Foundry launch signals monetization progress. The gap between quality (63% ROE, 89% GM) and multiple (7.4x fwd) is the entire investment thesis.

Every timeframe is in a clear downtrend. On the weekly, price has cascaded from ~$680 through prior support at ~$340 down to $207.70, with the model's own weekly forecast band ($320–$480) sitting well above spot — an aspirational mean-reversion picture, not a current signal. Daily shows the June breakdown from ~$275 to sub-$210 on heavy panic bars, with price -29.3% below SMA200, -13.2% below SMA50, -6.2% below SMA20, RSI 39.3, Perf Month -20.9%, Perf Quarter -15.0%. The 1h/4h charts show a rounded base $185–$210 with early stabilization and a small bullish gap around Jul 1, but $210–$215 is the immediate ceiling and there is a wall of supply into $230–$245. The Kronos forecasts (1h $242, 4h $365, 1d $285, 1wk $423) are strongly bullish but the model's daily directional accuracy (43%) is below the 54% naive baseline with 32% MAPE — so treat the yellow line as a bias indicator, not a target. Key levels: support $190 (52w low) then $180; resistance $215 → $230 → $245; a weekly close back above the SMA50 equivalent (~$245) would confirm regime change.

The signal in the news is that Adobe is actively reframing itself as an AI infrastructure vendor for enterprises, not just a creative-suite incumbent being disrupted. The Firefly Foundry launch (Jun 25) — letting enterprises train custom generative models on their own brand assets — is a real differentiator versus generic foundation models and monetizes the enterprise moat. The SeekingAlpha 'Value Equation Deep Dive' and Zacks trending-stock coverage both reflect that value-oriented investors are starting to circle. The Adobe vs ServiceNow comparison highlighting 30% net margin is a fair pushback against the 'ADBE is broken' narrative. The noise is the sentiment overhang: retail social feed is nominally bullish but includes 'Burry kiss of death' and activist-letter chatter, and the stock is being lumped in with the 'SaaSpocalypse' narrative that Guggenheim just upgraded CRM against. Congressional flow is mixed and small ($1k-$15k range, Cisneros bought April, sold May). None of this changes fundamentals; it does explain why the multiple is 7x.

- Firefly Foundry (announced Jun 25, 2026) — enterprise custom generative model platform trained on client brand assets, direct monetization of the enterprise data moat

- AI ARR reportedly +200% YoY per prior disclosures — the fastest-growing line item in the P&L needs to be re-cut and shown separately at the Sept 10 print

- $25B share repurchase authorization providing structural EPS tailwind at 7.4x forward multiple — each $5B repurchased at $205 retires ~24M shares (~6% of float)

- HUMAIN strategic alliance for generative AI model development referenced in the company profile — international/enterprise AI distribution channel

- Digital Experience segment cross-sell into the same enterprise buyers now piloting Foundry — analytics + content generation in one workflow

- AI disruption is real: OpenAI, Google, Midjourney and open-source models could commoditize core Creative Cloud use cases faster than Firefly scales

- Tape damage is severe — price 29% below SMA200, 42% below 6-month peak — value stocks in downtrends can stay cheap for years (see Perf 3Y -58%, Perf 5Y -65%)

- The AI forecast model's daily directional accuracy (43%) is below the naive baseline (54%) with 32% MAPE — the bullish yellow line is not a reliable signal in this regime

- Working capital is -$3.0B and current ratio 0.75 — not a liquidity concern with $9B FCF but leaves no cushion if growth stalls and buybacks are already committed

- Short interest 5.27% with 3.36 days-to-cover and Perf Month -20.9% — momentum shorts are pressing and can extend the drawdown

- September 10 earnings is the next binary event — a weak AI ARR number or FY27 guidance cut could take the stock to $170–$180

- Prior in-house base targets in the $242–$275 range have not printed over 8 sequential calls — anchor to a more conservative base

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord