AVAV— AI Stock Forecast & Price Targets

Published 6/30/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live AVAV price forecast →

AeroVironment presents a dichotomy: strong recent top-line revenue growth driven by defense demand contrasts sharply with negative profitability metrics and high valuation multiples. While the backlog and sector tailwinds are positive, the current stock price appears elevated relative to historical performance and near-term earnings quality, suggesting caution despite bullish news flow.

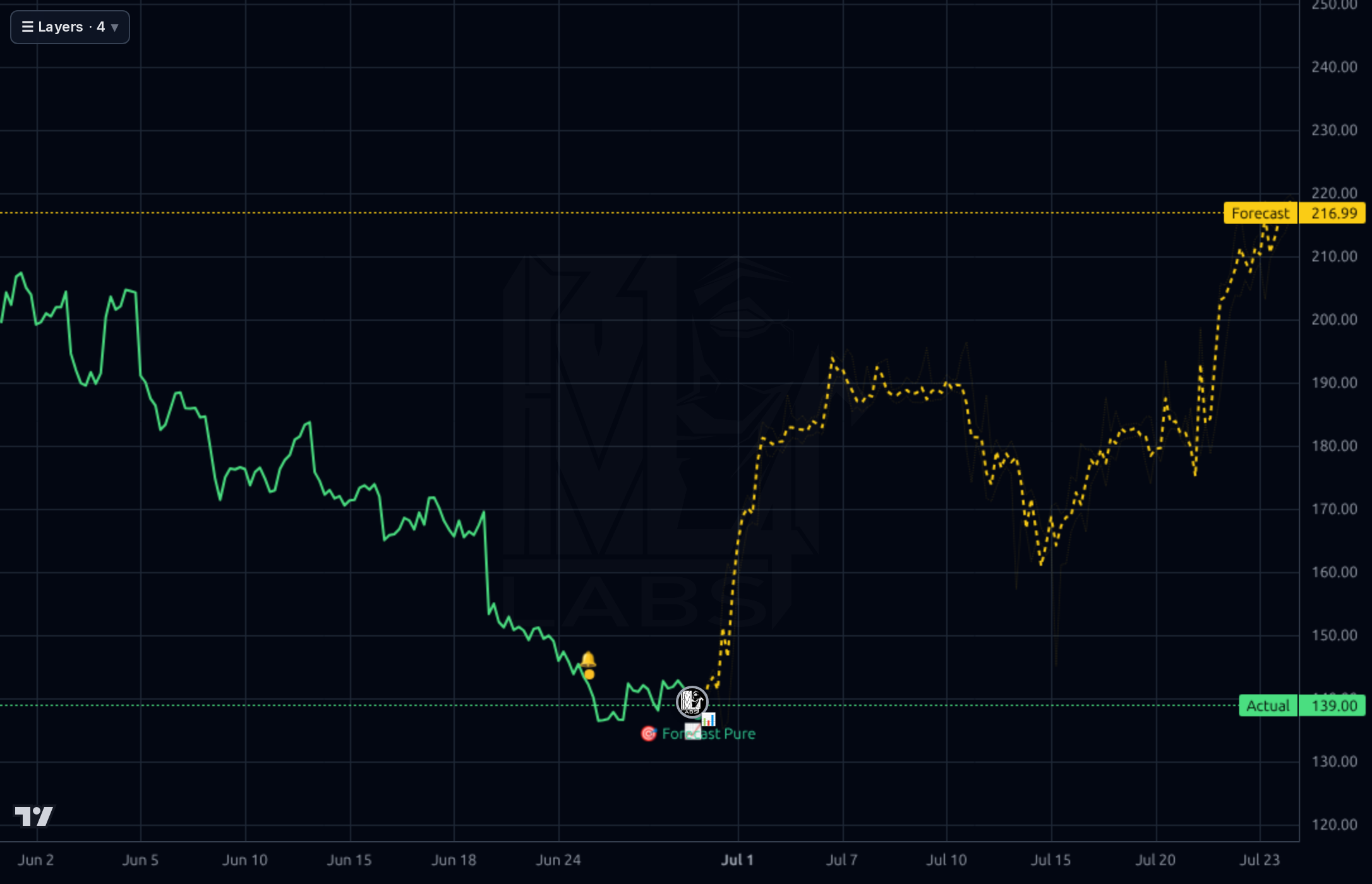

Given the immediate post-earnings volatility and low model reliability metrics, wait for a consolidation period near established support levels (e.g., testing the $130-$140 range) before initiating any significant long positions. A break above key resistance areas seen in the recent chart peaks would be required to confirm momentum.

The mid-term thesis hinges on the company's ability to convert high revenue growth into positive, sustainable net income and free cash flow. If management can demonstrate margin expansion through operational improvements (beyond just top-line bookings), the stock has a clear path toward realizing its higher analyst targets ($180 base).

The long-term thesis is supported by the structural shift towards defense spending, positioning AVAV well within the growing autonomous systems and robotics sector. The key driver remains securing large, multi-year government contracts that stabilize revenue streams regardless of short-term profitability fluctuations.

The company reports strong top-line performance with record Q4 revenue of $641.62 million and full-year revenue guidance pointing to continued growth (FY2027 projected revenue between US$2.13B and US$2.23B). However, profitability is severely challenged; the full-year net loss was US$265.12 million, resulting in negative profit margins (-13.9%). The balance sheet shows significant total debt ($826M) relative to equity, and free cash flow remains negative across reported periods. While revenue growth signals strong demand, the inability to translate this into positive net income or consistent FCF raises concerns about operational efficiency and cost management.

The price action visible in both charts shows a significant downtrend followed by sharp volatility spikes around earnings announcements. The recent forecast band suggests support near $139 (actual) with a base target of $187.00, implying upward momentum is expected to continue above current levels. However, the model's own directional accuracy metrics for short-term horizons are low (e.g., 1d: 16% vs 94% naive baseline), suggesting that recent price action has been erratic and difficult to predict reliably by the model in this regime. The stock is trading near its 52-week low ($135.2) on the fundamentals sheet, which could act as a technical floor.

The primary signal is overwhelmingly positive regarding demand: AeroVironment reported record Q4 revenue driven by strong global defense demand and major acquisitions. Management highlighted an 'unprecedented' defense demand over the next two years, supported by a $1.2 billion backlog. The negative aspect is the profit outlook; despite record revenue, the company posted a full-year net loss of US$265.12 million, which tempers the enthusiasm generated by the top-line beat.

- Expansion in ground robotics portfolio, as noted by analysts, suggests diversification beyond core UAS offerings.

- The development of advanced technologies like digital beamforming technology and AI-powered OSINT platforms points to future high-margin revenue streams.

- High valuation multiples (Forward P/E of 34.7) combined with negative TTM earnings create significant downside risk if defense spending slows or execution falters.

- The company's reliance on large government contracts exposes it to potential budget delays, funding shifts, or changes in defense policy.

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord