CTSH— AI Stock Forecast & Price Targets

Published 7/1/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live CTSH price forecast →

CTSH trades at deep-value multiples (P/E 8.4x) with strong cash flow generation ($1.9B FCF), but faces secular risk from AI-driven revenue compression in legacy IT services. Recent news highlights strategic AI partnerships, yet sell-side skepticism and a 55% drawdown from $87 to $38.74 suggest significant undervaluation.

Wait for earnings (July 29) as the binary event; if price holds above $38.50, consider small accumulation. Invalidation: break below $37.50 triggers short-term sell-off.

Focus on AI monetization progress post-earnings. Target $45-$50 range by Q4 2026 based on valuation (PEG 0.67) and cash flow stability. Catalysts include ServiceNow integration results and bookings growth confirmation.

Terminal thesis: CTSH could trade at 12x forward P/E if AI orchestration monetization accelerates, but secular risk from legacy revenue compression remains a structural headwind. Long-term value hinges on successful transition to high-margin AI services.

Revenue growth remains modest (6.55% Y/Y TTM) but cash flow is robust ($1.9B FCF, 15.77% operating margins). The balance sheet is fortress-like with $1.5B cash vs $1.09B debt and low leverage (debt/equity 0.07). However, the Q3 2025 net income anomaly (-$274M) raises concerns about recurring margin pressure. Dividend yield of 3.31% is attractive but pricing already discounts AI monetization risks.

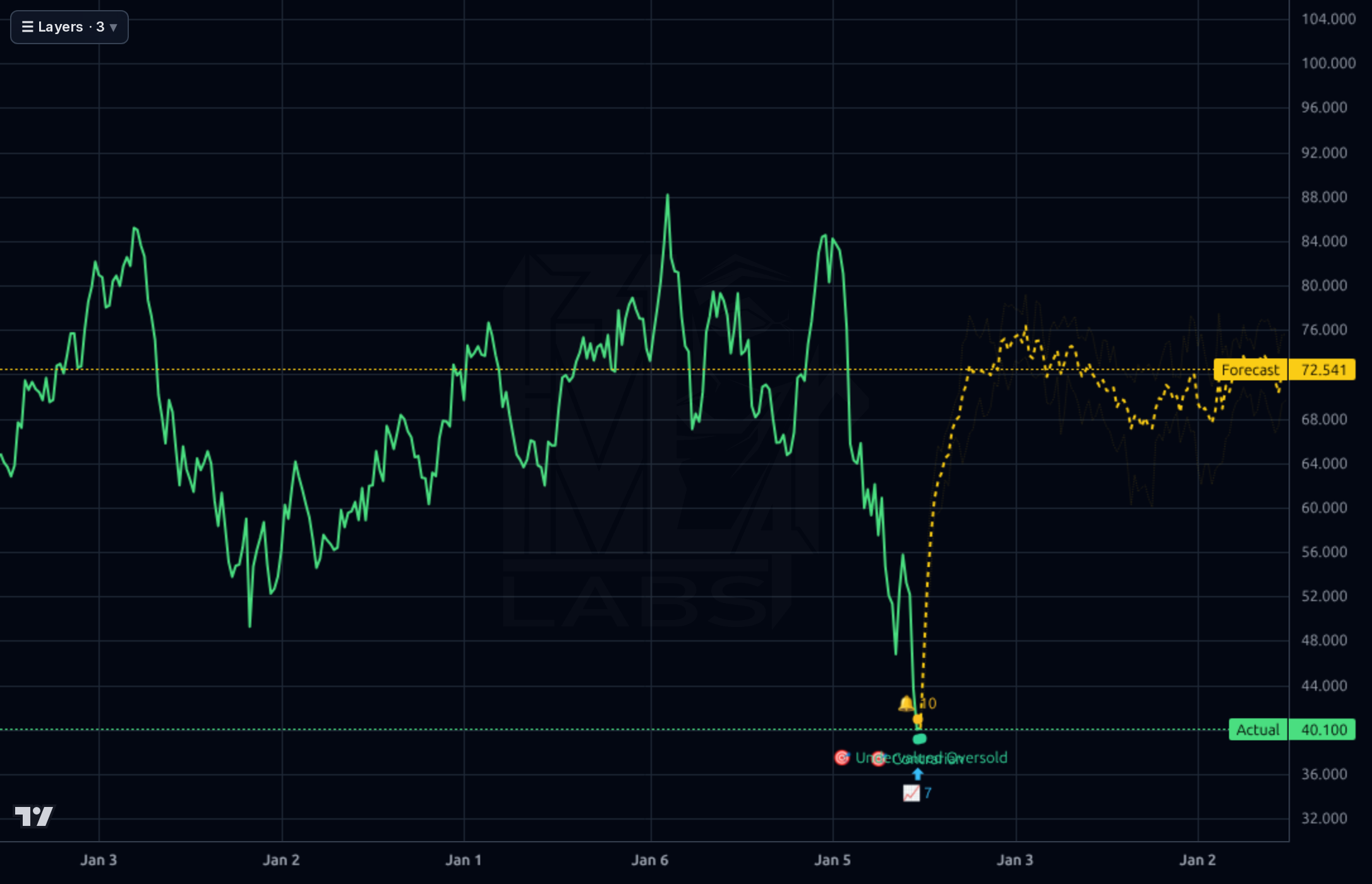

The chart shows a bearish trend with price below both SMA20 (-18.6%) and SMA50 (-23.65%), indicating weak momentum. Support levels near $38-$40 are critical; the forecast band (72.54/64.61) is significantly above current price, suggesting a massive gap between model expectations and reality. RSI at 23.23 confirms oversold conditions but technicals remain bearish due to extended downtrend.

Key news includes Cognizant's AI partnerships (ServiceNow integration, Pearson collaboration) signaling strategic positioning in enterprise AI orchestration. However, Morgan Stanley cutting PT to $47 and TD Cowen lowering PT to $47 reflects sell-side skepticism. The stock hasn't benefited from broader AI momentum despite strong fundamentals, creating a potential value trap.

- ServiceNow AI Agents integration with Neuro AI Multi-Agent Accelerator (Q3 2025) driving enterprise AI adoption

- Pearson partnership for workforce development programs expanding AI skills pipeline

- Secular risk: Generative AI compressing legacy BPO/maintenance revenue faster than new AI services can compensate

- Sell-side skepticism: Persistent analyst downgrades pricing in near-term headwinds

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord