PLNT— AI Stock Forecast & Price Targets

Published 6/26/2026 · A free sample of K3vl4r’s AI-powered analysis.

Kronos price forecasts, scored fundamentals & technicals, and a multi-horizon plan.

View the live PLNT price forecast →

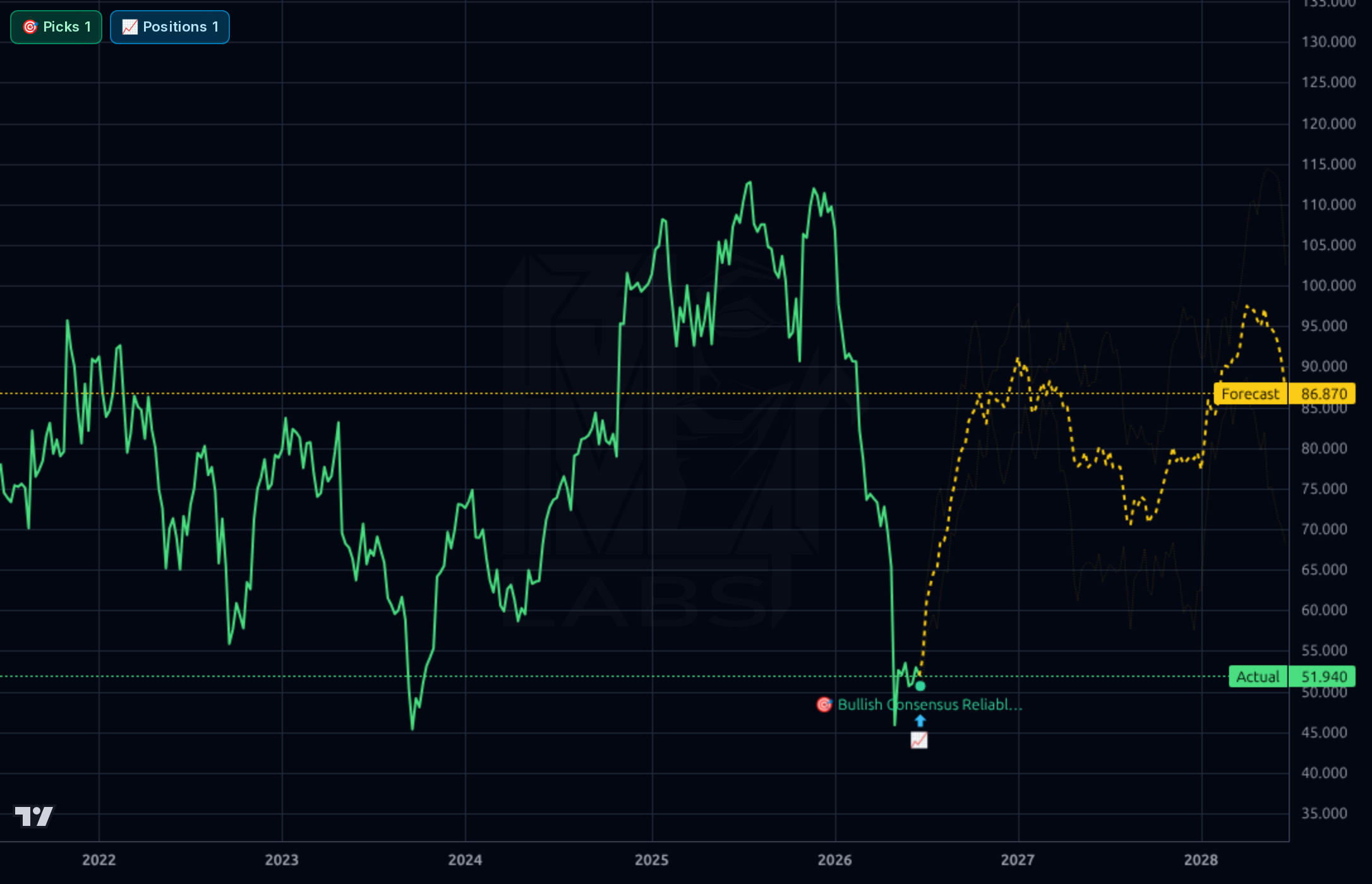

Planet Fitness trades at $51.94 after a brutal ~52% YTD drawdown from $114, with the Kronos model and analyst targets ($67.59) both suggesting meaningful upside while fundamentals remain solid (Q1 revenue +21.9% Y/Y, 29.6% operating margins, $122M FCF). However, the recent Zacks 'Bear of the Day' designation, cut 2026 guidance from slowing member growth, and a CFO transition argue for patience — this looks like a contrarian accumulation setup, not a clean breakout.

1-4 week view: Cautious long / starter position. Price is basing at $50-54 with RSI neutral and short float 9.35% (squeeze fuel). Initiate at ~$51-52 with hard invalidation on a daily close below $48 (loses the post-capitulation base). First target $58-60 (gap fill / 50D reclaim attempt). Size at 1/3 of intended position — the model's vertical forecast is unreliable in magnitude (MAPE ~49%), so don't chase. If $54 breaks with volume, add.

1-6 month view: Constructive but data-dependent. Thesis: guidance has been reset lower, expectations are crushed, new CFO arrives, and any in-line or modestly better quarter could drive a 30-40% re-rating toward the $67.59 analyst consensus. Expected return range +15% to +35% to $60-70. Catalysts: next earnings print, any membership trend stabilization commentary, CFO's first capital allocation signal. What changes my mind: another guidance cut, member churn accelerating, or macro consumer rollover hitting the value-fitness segment.

1-3 year view: PLNT remains a high-return franchise model (ROIC 9.6%, operating margin ~30%) with secular tailwinds in low-cost fitness. Terminal thesis: re-rating to 18-22x forward EPS on $4-5 EPS by 2028 implies $80-100. Multi-year drivers: unit growth, dues pricing, Black Card mix, international optionality. Biggest structural risk: the negative equity / $2.9B debt stack makes the equity acutely sensitive to any sustained membership decline or refinancing at higher rates — this is a leveraged equity story masquerading as a steady compounder.

Operationally PLNT is performing well: Q1 2026 revenue of $337.2M (+21.9% Y/Y per snapshot), gross margin 50.8%, operating margin 29.3%, net margin 15.3%, and EBITDA of $145.2M. TTM EPS of $2.77 yields an 18.8x trailing and 14.4x forward P/E with PEG 1.37 — reasonable for a franchise-heavy model. Cash flow quality is strong: Q1 OCF $147.5M and FCF $122M (a notable jump vs. Q4's $59M), and ROIC of 9.6% is acceptable. The blemish is the balance sheet: $2.89B total debt against $375M cash and negative stockholders' equity of -$482M (a function of buybacks/franchise structure, not distress, but it eliminates the P/B metric and amplifies sensitivity to rates). EV/EBITDA of 11.5x and EV/Sales 4.7x are not cheap in absolute terms but compressed vs. history. The core issue flagged by the Zacks bear note — new membership growth slowed in Q1 and 2026 guidance was cut — is the swing factor; reported numbers look fine, but the forward unit-economics narrative cracked.

The price action is ugly on the longer timeframes and constructive only at the very short end. On the weekly, PLNT collapsed from a 52-week high of $114.47 to $51.94 (-54.6%), wiping out roughly two years of gains and sitting -39% below the 200-day SMA. The daily shows a capitulation low near $44, a bounce, and now a tight base around $50-54 with RSI at 46.8 (neutral, no oversold bounce left to harvest mechanically). The 1h chart shows price hugging $51-54 with the Kronos forecast projecting an aggressive ramp toward $72.75 over the forecast horizon; the 4h echoes a move to ~$99, and the daily forecast targets $87.57 — all bullish, with directional accuracy at 78% over 30d in backtests (though MAPE is a wide ~49%, so magnitude is unreliable). Near-term bullish probability prints 1.0. Key levels: support $50/$44 (recent low), resistance $54 (20D), then a gap to fill toward $64-67 (analyst target zone and prior breakdown shelf). The divergence to watch: model says vertical rally; tape says base-building — trust the base first.

The newsflow is net-negative but stale and largely priced in. Zacks tagged PLNT 'Bear of the Day' on June 22 explicitly citing slowing new-member growth and a 2026 guidance cut, and Seeking Alpha downgraded to Hold on June 19 for the same reason. The CFO transition (Sudhanshu Priyadarshi from Keurig Dr. Pepper, granted a $3M new-hire award) is a leadership reset that could be a positive medium-term catalyst — bringing in a large-cap CPG CFO suggests a sharpened focus on capital allocation and member monetization. ChartMill's GARP piece (June 26) noting 22% earnings growth at 16x P/E is the constructive counterpoint. Signal: guidance cut is real and the stock has already absorbed a 50%+ drawdown reflecting it. Noise: the broader 'risky consumer discretionary' bucket call is generic. The setup is classic post-cut washout with a new CFO — fundamentally interesting but lacking a near-term catalyst until the next earnings print on May 07 (per snapshot; likely Q2 reporting in August given current date).

- New CFO Sudhanshu Priyadarshi (ex-Keurig Dr. Pepper) onboarding with $3M new-hire award — large-cap CPG capital allocation discipline incoming

- Q1 2026 revenue growth of +21.9% Y/Y and EPS Q/Q +30.3% despite the membership slowdown — pricing and Black Card mix carrying the model

- FCF inflection: Q1 FCF $122M vs. Q4 $59M and Q2'25 $9.7M — capex moderating and cash generation accelerating

- Forward P/E 14.4x with PEG 1.37 — re-rating optionality if guidance stabilizes

- Analyst consensus Recom 1.80 (Buy) with $67.59 target = +30% from spot

- 2026 guidance was cut on slowing new-member additions (Zacks Bear of the Day, June 22) — risk of a second cut at next print

- Negative stockholders' equity of -$482M and $2.89B total debt — leveraged equity with refinancing/rate sensitivity

- Short float 9.35% with 3.16 days to cover — crowded short but also reflects negative sentiment

- Stock is -52% YTD and -54.6% from 52W high; -39% below 200D SMA — broken long-term trend, no technical confirmation yet

- Consumer discretionary cycle risk flagged in news; value-fitness historically defensive but not immune

- Kronos forecast magnitude unreliable (MAPE 49% on 30d) — directional 78% is useful, the +40% target moves are not

- CFO transition introduces execution uncertainty in the next 1-2 quarters

Get AI analysis on any stock

This is one of hundreds of Kronos AI reports — scored fundamentals & technicals, bull/base/bear price targets, a multi-horizon plan, and continuously-updated forecasts across the market. Create a free account to explore them all.

Create your free account →Already a member? Sign in · Join our Discord